William_Potter

Funding Thesis

Constructing a strong basis for a well-balanced and extensively diversified dividend portfolio might be of immense worth for the creation of wealth over the long run.

On this article, I’ll present you how one can construct a broadly diversified dividend portfolio that mixes each dividend revenue and dividend progress whereas on the similar time providing a excessive likelihood of attaining constructive funding outcomes.

For this demonstration, I’ll use the present composition of The Dividend Revenue Accelerator Portfolio for example. Although the portfolio remains to be within the development part (it at the moment consists of 1 ETF and 12 particular person firms), it already gives a sexy mixture of dividend revenue and dividend progress, given its balanced composition.

Furthermore, the portfolio gives a broad diversification over firms, sectors, and industries, along with offering geographical diversification, in addition to diversification throughout completely different fairness kinds, which I’ll display on this evaluation.

The portfolio’s lowered threat stage just isn’t solely attributed to its in depth diversification, but in addition to different components that improve the safety of buyers. I’ll illustrate the portfolio’s lowered threat stage by analyzing the 60M Beta Components of the businesses which can be a part of it, in addition to their Payout Ratios and EPS Development Charges, thus offering a complete threat evaluation of the portfolio.

This in depth threat evaluation of The Dividend Revenue Accelerator Portfolio raises my confidence that the portfolio already gives buyers with a lowered threat stage, resulting in an elevated likelihood of attaining engaging funding outcomes. This makes The Dividend Revenue Accelerator Portfolio a sexy funding method to adapt and comply with.

Final Wednesday, I made the most recent acquisition for The Dividend Revenue Accelerator Portfolio by including British American Tobacco:

British American Tobacco vs. Altria: Which is the Higher Dividend Alternative?

Presently, the portfolio gives buyers with a Weighted Common Dividend Yield [TTM] of 4.69% and a 5 12 months Weighted Common Dividend Development Fee [CAGR] of 9.03%. These metrics point out that the portfolio efficiently combines dividend revenue with dividend progress, highlighting its huge attractiveness for buyers.

The Dividend Revenue Accelerator Portfolio Presently Consists of the Following Positions:

Schwab U.S. Dividend Fairness ETF (NYSEARCA:SCHD) Realty Revenue (NYSE:O) Philip Morris (NYSE:PM) Royal Financial institution of Canada (NYSE:RY) Apple (NASDAQ:AAPL) AT&T (NYSE:T) Mastercard (NYSE:MA) Important Avenue Capital (NYSE:MAIN) Johnson & Johnson (NYSE:JNJ) Financial institution of America (NYSE:BAC) Ares Capital (NASDAQ:ARCC) BlackRock TCP Capital (NASDAQ:TCPC) British American Tobacco (NYSE:BTI)

The Dividend Revenue Accelerator Portfolio

The Dividend Revenue Accelerator Portfolio’s goal is the era of revenue by way of dividend funds, and to yearly increase this sum. Along with that, its aim is to achieve an interesting Complete Return when investing with a lowered threat stage over the long-term.

The Dividend Revenue Accelerator Portfolio’s lowered threat stage shall be reached because of the portfolio’s broad diversification over sectors and industries and the inclusion of firms with a low Beta Issue.

Beneath you’ll find the traits of The Dividend Revenue Accelerator Portfolio:

Engaging Weighted Common Dividend Yield [TTM] Engaging Weighted Common Dividend Development Fee [CAGR] 5 12 months Comparatively low Volatility Comparatively low Danger-Stage Engaging anticipated reward within the type of the anticipated compound annual price of return Diversification over asset lessons Diversification over sectors Diversification over industries Diversification over international locations Purchase-and-Maintain suitability

Overview of the Firms That Are A part of The Dividend Revenue Accelerator Portfolio

Image

Firm Title

Sector

Business

Nation

P/E [FWD]

Dividend Yield [TTM]

Dividend Development 5Y

Variety of shares

Acquisition Value per Share in $

Complete Acquisition in $

Present Value per Share in $

Market Worth in $

Present Allocation

SCHD

Schwab U.S. Dividend Fairness ETF

ETFs

ETFs

United States

3.53%

13.92%

13.3761

74.83

1000.93

71.34

954.25

43.52%

O

Realty Revenue

Actual Property

Retail REITs

United States

40.13

5.46%

4.28%

1.8185

55.54

101.00

54.05

98.29

4.48%

PM

Philip Morris

Shopper Staples

Tobacco

United States

18.52

5.38%

3.15%

1.0552

95.71

100.99

93.78

98.96

4.51%

RY

Royal Financial institution of Canada

Financials

Diversified Banks

Canada

11.65

4.49%

6.24%

1.0936

92.36

101.00

85.58

93.59

4.27%

AAPL

Apple

Data Expertise

Expertise {Hardware}, Storage and Peripherals

United States

28.92

0.56%

6.59%

0.5867

172.14

100.99

189.59

111.23

5.07%

T

AT&T

Communication Companies

Built-in Telecommunication Companies

United States

7.33

7.40%

-5.97%

6.8036

14.84

100.97

16.09

109.47

4.99%

MA

Mastercard

Financials

Transaction & Cost Processing Companies

United States

34.37

0.58%

17.92%

0.2544

396.96

100.99

408.75

103.99

4.74%

MAIN

Important Avenue Capital

Financials

Asset Administration and Custody Banks

United States

9.02

6.95%

3.58%

2.4876

40.6

101

41.38

102.94

4.69%

JNJ

Johnson & Johnson

Well being Care

Prescription drugs

United States

22.61

3.09%

5.83%

0.6557

154.01

100.99

151.04

99.04

4.52%

BAC

Financial institution of America

Financials

Diversified Banks

United States

8.89

3.73%

12.03%

3.9191

25.77

101

29.42

115.30

5.26%

ARCC

Ares Capital

Financials

Asset Administration and Custody Banks

United States

7.72

9.66%

4.65%

5.0812

19.88

101

19.81

100.66

4.59%

TCPC

BlackRock TCP Capital

Financials

Asset Administration and Custody Banks

United States

8.69

11.87%

-1.73%

8.8111

11.46

101

11.88

104.68

4.77%

BTI

British American Tobacco

Shopper Staples

Tobacco

United Kingdom

7.94

8.84%

2.45%

3.094

32.11

101

32.37

100.15

4.57%

Click on to enlarge

Supply: The Creator, knowledge from Looking for Alpha

Danger Evaluation of The Present Composition of The Dividend Revenue Accelerator Portfolio

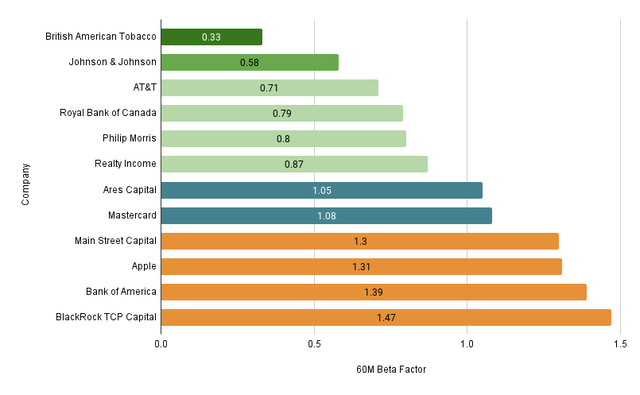

Danger Evaluation: Analyzing the Firms’ 60M Beta Components

The graphic beneath illustrates the 60M Beta Components of the businesses which can be a part of The Dividend Revenue Accelerator Portfolio. The chart reveals that half of the portfolio’s 12 particular person positions have a 60M Beta Issue beneath 1.

These low 60M Beta Components display that the businesses can contribute to lowering portfolio volatility, thus indicating a low threat stage for buyers.

The businesses which contribute most to lowering portfolio volatility are British American Tobacco (60M Beta Issue of 0.33), Johnson & Johnson (60M Beta Issue of 0.58), AT&T (0.71), Royal Financial institution of Canada (0.79), Philip Morris (0.8), and Realty Revenue (0.87).

Supply: The Creator, knowledge from Looking for Alpha

It’s price highlighting that the most recent incorporation of British American Tobacco into The Dividend Revenue Accelerator Portfolio contributes considerably to the portfolio’s lowered volatility and threat stage.

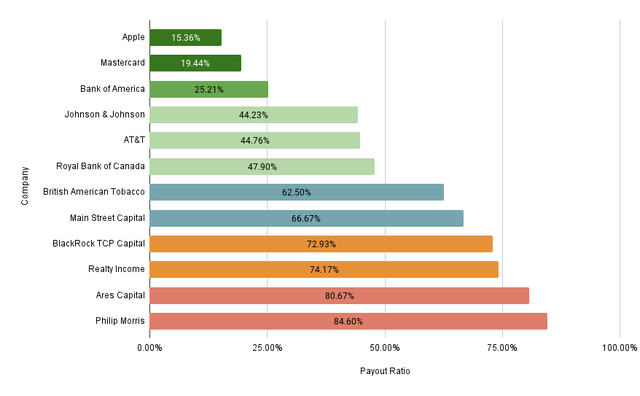

Danger Evaluation: Analyzing the businesses’ Payout Ratios

The graphic beneath reveals the Payout Ratios of the businesses which can be a part of The Dividend Revenue Accelerator Portfolio. The chart reveals that 10 of the 12 firms keep a Payout Ratio beneath 80%, highlighting the lowered threat stage of The Dividend Revenue Accelerator Portfolio.

A low Payout Ratio signifies that there’s loads of room for dividend enhancements. A excessive Payout Ratio, nonetheless, might be seen as a warning sign that the likelihood of a dividend minimize is greater, which might have a robust unfavourable impression on the corporate’s inventory worth, representing a threat issue for buyers.

Contemplating the person firms which can be a part of The Dividend Revenue Accelerator Portfolio, Apple has the bottom Payout Ratio (15.36%), adopted by Mastercard (19.44%), Financial institution of America (25.21%), Johnson & Johnson (44.23%), AT&T (44.76%), and Royal Financial institution of Canada (47.90%).

Supply: The Creator, knowledge from Looking for Alpha

Solely Ares Capital (Payout Ratio of 80.67%), and Philip Morris (84.60%) have a Payout Ratio above 80%. The upper payout ratios of Ares Capital and Philip Morris in comparison with the opposite firms of the portfolio, reinforce my determination to not over-represent the 2 shares in The Dividend Revenue Accelerator Portfolio. Doing so reduces the chance stage for buyers whereas boosting the potential of a profitable funding efficiency.

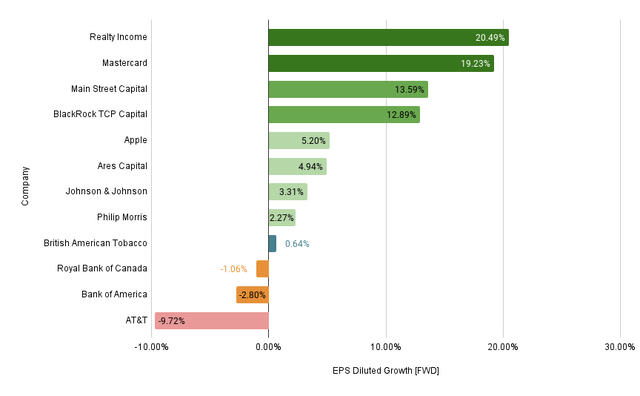

Danger Evaluation: Analyzing the businesses’ EPS Development Charges

The graphic beneath illustrates the EPS Development Charges of the person firms which can be a part of The Dividend Revenue Accelerator Portfolio.

The chart reveals that 9 out of the 12 particular person firms have proven constructive EPS Development Charges.

4 out of the 12 firms have even proven double digit EPS Development Charges [FWD]: Realty Revenue (EPS Development Fee [FWD] of 20.49%), Mastercard (19.23%), Important Avenue Capital (13.59%), and BlackRock TCP Capital (12.89%).

Solely three from the 12 chosen firms have proven a unfavourable EPS Development Fee: AT&T (EPS Development Fee [FWD] of -9.72%), Financial institution of America (-2.80%), and Royal Financial institution of Canada (-1.06%).

Supply: The Creator, knowledge from Looking for Alpha

These metrics are a transparent indicator of the businesses’ dedication to offering shareholder worth. It additionally serves as a further indicator that The Dividend Revenue Accelerator Portfolio has a lowered threat stage and due to this fact, an elevated likelihood of manufacturing favorable funding outcomes.

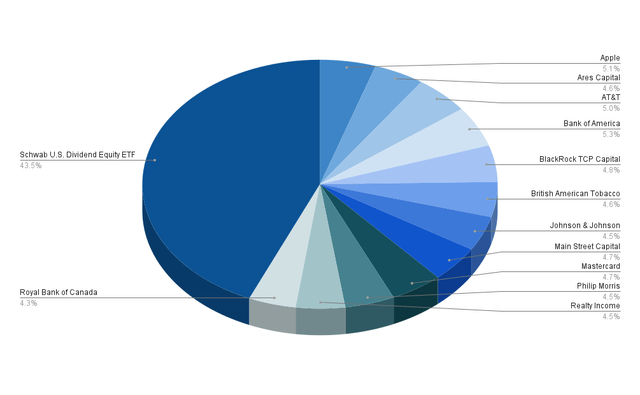

Danger Evaluation: The Dividend Revenue Accelerator Portfolio’s Diversification Throughout Firms/ETF

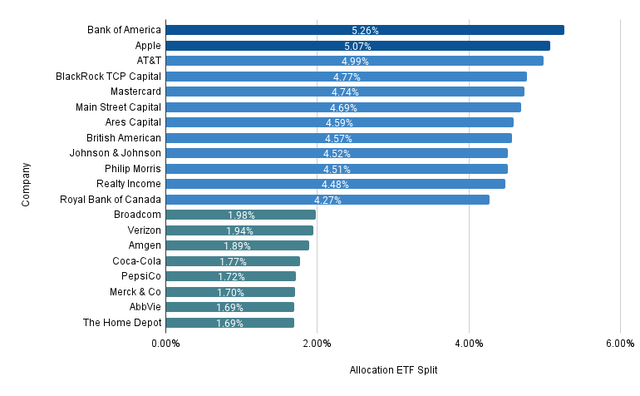

Presently, Schwab U.S. Dividend Fairness ETF represents the most important place of The Dividend Revenue Accelerator Portfolio, accounting for 43.5%.

With a proportion of 5.26%, Financial institution of America signify the most important particular person firm in comparison with the general portfolio, adopted by Apple (with a proportion of 5.07%), and AT&T (4.99%).

The truth that the Payout Ratios of the three largest positions are considerably beneath 50%, additional confirms my idea that this portfolio gives buyers a lowered threat stage: as proven within the earlier chapter, Financial institution of America’s Payout Ratio stands at 25.21%, Apple’s at 15.36%, and AT&T’s at 44.76%, indicating a low likelihood of a dividend minimize for the three largest positions of The Dividend Revenue Accelerator Portfolio.

The graphic beneath illustrates the portfolio allocation per Firm/ETF:

Supply: The Creator, knowledge from Looking for Alpha

Danger Evaluation: The Dividend Revenue Accelerator Portfolio’s Diversification Throughout Firms When Allocating SCHD to the Firms It Is Invested In

The graphic beneath demonstrates the present portfolio allocation of The Dividend Revenue Accelerator Portfolio when allocating Schwab U.S. Dividend Fairness ETF throughout the businesses it’s invested in.

I’ve rigorously chosen the businesses beneath to make sure that not one of the particular person firms I’ve added are already a part of Schwab U.S. Dividend Fairness ETF. This ensures that the portfolio has a low company-specific focus threat.

It’s price highlighting that even when allocating Schwab U.S. Dividend Fairness ETF throughout the businesses it’s invested in, solely Financial institution of America (with a proportion of 5.26%) and Apple (5.07%) account for greater than 5% of the general funding portfolio.

All different firms account for lower than 5%, indicating a lowered company-specific focus threat for buyers of The Dividend Revenue Accelerator Portfolio.

It is usually price mentioning that every one firms that at the moment account for lower than 2% of the general portfolio are oblique investments by the funding in Schwab U.S. Dividend Fairness ETF. Please observe that within the graphic beneath, solely the present largest 20 positions of The Dividend Revenue Accelerator Portfolio are included (together with 12 direct investments in particular person firms and the 8 largest positions of Schwab U.S. Dividend Fairness ETF).

Supply: The Creator, knowledge from Looking for Alpha and Morningstar

Danger Evaluation: The Dividend Revenue Accelerator Portfolio’s Diversification Throughout Sectors

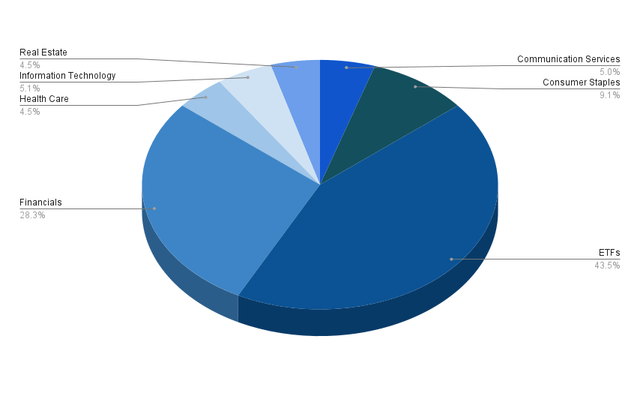

The ETF Sector represents the most important sector of The Dividend Revenue Accelerator Portfolio at this second in time, accounting for 43.5% of the general portfolio.

The second largest sector is the Financials Sector, representing a proportion of 28.3%. This sector is represented by Financial institution of America (5.26%), BlackRock TCP Capital (4.77%), Mastercard (4.74%), Important Avenue Capital (4.69%), Ares Capital (4.59%), and Royal Financial institution of Canada (4.27%).

The third largest sector is the Shopper Staples Sector with 9.1%. The Shopper Staples Sector is represented by British American Tobacco (4.57%) and Philip Morris (4.51%).

The fourth largest sector is the Data Expertise Sector, represented by Apple (5.07%), adopted by the Communication Companies Sector (represented by AT&T with 4.99%),

The Heath Care Sector (represented by Johnson & Johnson) accounts for 4.52% of the general funding portfolio.

The Actual Property Sector (represented by Realty Revenue) accounts for 4.48%.

Supply: The Creator, knowledge from Looking for Alpha

Beside the ETF Business, solely the Financials Sector accounts for a bigger proportion of the general portfolio (with 28.3%). All different sectors account for lower than 10%, indicating a lowered threat stage for buyers.

Nonetheless, the Financials Sector accounting for such a big proportion of the general funding portfolio does indicate some sector-specific focus threat.

ETFs (43.5%)

Schwab U.S. Dividend Fairness ETF (43.5%)

Financials Sector (28.32%)

Financial institution of America (5.26%) BlackRock TCP Capital (4.77%) Mastercard (4.74%) Important Avenue Capital (4.69%) Ares Capital (4.59%) Royal Financial institution of Canada (4.27%)

Shopper Staples (9.08%)

British American Tobacco (4.57%) Philip Morris (4.51%)

Data Expertise (5.07%)

Communication Companies (4.99%)

Well being Care (4.52%)

Johnson & Johnson (4.52%)

Actual Property (4.48%)

Danger Evaluation: The Dividend Revenue Accelerator Portfolio’s Diversification Throughout Sectors When Allocating SCHD to the Sectors It Is Invested In

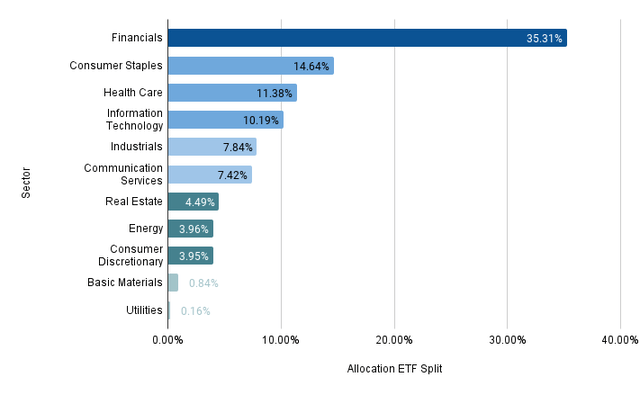

The graphic beneath illustrates the portfolio allocation per sector when allocating Schwab U.S. Dividend Fairness ETF throughout the sectors it’s invested in.

It may be famous that the Financials Sector is by far the most important sector, with a proportion of 35.31% of the general portfolio, once more indicating some sector-specific focus threat of The Dividend Revenue Accelerator Portfolio.

The Shopper Staples Sector presently represents 14.64% of the general funding portfolio, adopted by the Well being Care Sector (with 11.38%), and the Data Expertise Sector (with 10.19%).

The Industrials Sector (with 7.84%), and the Communication Companies Sector (with 7.42%) account for considerably lower than 10% of the general portfolio.

The Actual Property Sector (with 4.49%), the Vitality Sector (3.96%), the Shopper Discretionary Sector (3.95%), the Fundamental Supplies Sector (0.84%), and the Utilities Sector (0.16%) account for considerably lower than 5% of the general funding portfolio, indicating a lowered threat stage for buyers.

Supply: The Creator, knowledge from Looking for Alpha

By means of the inclusion of further firms into The Dividend Revenue Accelerator Portfolio inside the subsequent weeks, I’ll increase the portfolio’s diversification, lowering the sector-specific focus threat that it at the moment has as a consequence of its concentrated allocation to the Financials Sector.

Danger Evaluation: The Dividend Revenue Accelerator Portfolio’s Diversification Throughout Industries

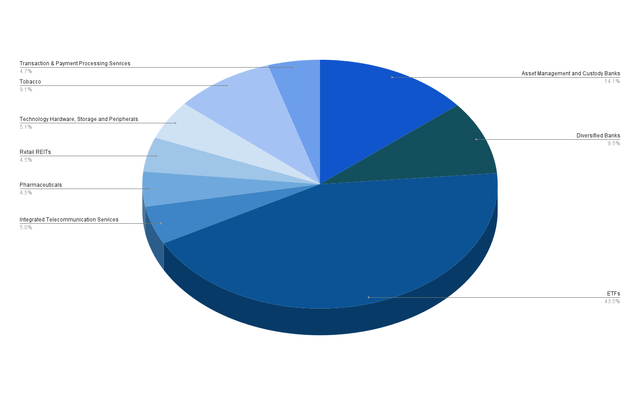

The graphic beneath reveals the portfolio allocation per {industry}. It may be highlighted that the ETF Business accounts for the most important proportion of the general funding portfolio (43.5%).

The second largest {industry} is the Asset Administration and Custody Banks Business with 14.1%. This {industry} is represented by BlackRock TCP Capital (4.77%), Important Avenue Capital (accounting for 4.69%), and Ares Capital (4.59%).

The third largest {industry} is the Diversified Banks Business, accounting for nearly 10% of the general funding portfolio. This {industry} is represented by Financial institution of America (5.26%) and Royal Financial institution of Canada (4.27%).

The Tobacco Business, which is represented by British American Tobacco (4.57%) and Philip Morris (4.51%), accounts for 9.1% of the general funding portfolio.

The fifth largest {industry} is the Expertise {Hardware}, Storage and Peripherals Business, represented by Apple with 5.07%.

All different industries account for lower than 5% of the general portfolio, highlighting, as soon as once more the lowered threat stage of The Dividend Revenue Accelerator Portfolio.

Supply: The Creator, knowledge from Looking for Alpha

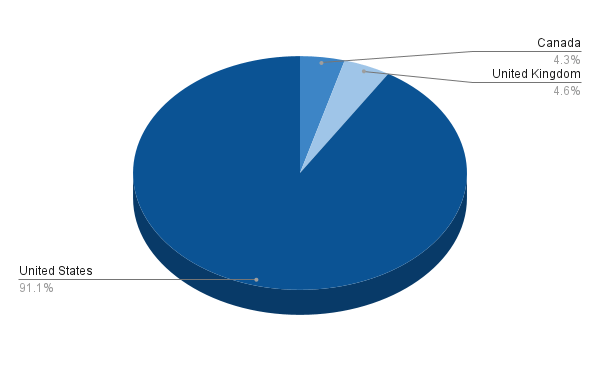

Danger Evaluation: The Dividend Revenue Accelerator Portfolio’s Geographical Diversification

The graphic beneath illustrates the nation allocation of the portfolio. It highlights a pre-dominant share of firms based mostly in The US, representing 91.1% of the general funding portfolio.

8.9% of the portfolio’s firms are located exterior america: British American Tobacco (from the UK) represents a share of 4.6% of the general portfolio, and Royal Financial institution of Canada (from Canada), a share of 4.3%.

Supply: The Creator, knowledge from Looking for Alpha

The illustration reveals that The Dividend Revenue Accelerator Portfolio achieves a level of geographical diversification, successfully lowering its geographic-specific focus threat.

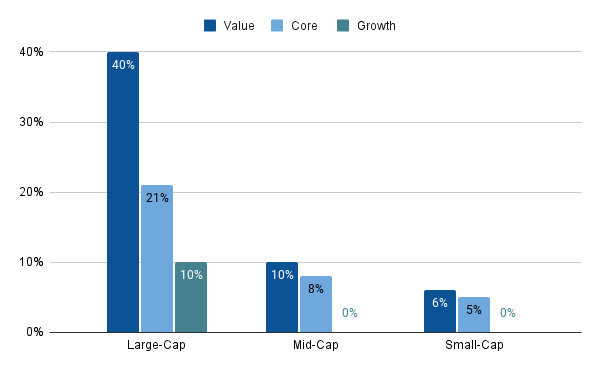

Danger Evaluation: The Fairness Type of The Dividend Revenue Accelerator Portfolio When Allocating SCHD Throughout the Equities It Is Invested In

By means of the allocation of Schwab U.S. Dividend Fairness ETF throughout the equities it’s invested in, it may be famous that The Dividend Revenue Accelerator Portfolio consists of 71% large-cap firms, 18% mid-cap firms and 11% small-cap firms. The Dividend Revenue Accelerator’s deal with large-cap firms is an indicator of the portfolio’s lowered risk-level.

Along with that, it’s price highlighting that 56% of the present composition of The Dividend Revenue Accelerator Portfolio consists of worth firms, 34% of core firms (which mix worth and progress), and 10% of progress firms. The portfolio’s deal with worth firms is a further indicator that highlights the decrease stage of threat for buyers.

The biggest proportion of The Dividend Revenue Accelerator Portfolio is invested in large-cap firms with a deal with worth (40%), as soon as once more underscoring its low stage of threat.

Supply: The Creator, knowledge from Looking for Alpha and Morningstar

The Power of The Present Composition of The Dividend Revenue Accelerator Portfolio

Engaging Weighted Common Dividend Yield [TTM]: The present Weighted Common Dividend Yield [TTM] of The Dividend Revenue Accelerator Portfolio stands at 4.69%, highlighting its means to generate further revenue by way of dividends for buyers. Engaging 5 12 months Weighted Common Dividend Development Fee: The present 5 12 months Weighted Common Dividend Development Fee [CAGR] of The Dividend Revenue Accelerator Portfolio stands at 9.03%, clearly demonstrating that the businesses ought to be capable to increase their dividends within the years to come back. Decreased Volatility by the inclusion of firms with a low Beta Issue: British American Tobacco (60M Beta Issue of 0.33), Johnson & Johnson (0.58), AT&T (0.71), Royal Financial institution of Canada (0.79), Philip Morris (0.8), and Realty Revenue (0.87) have a 60M Beta Issue beneath 1 and contribute to lowering the volatility of The Dividend Revenue Accelerator Portfolio, underlying its lowered threat stage. Inclusion of firms with a low Payout Ratio: Six from the 12 particular person firms which can be a part of The Dividend Revenue Accelerator Portfolio have a Payout Ratio beneath 50%, indicating a low probability of a dividend minimize. Inclusion of firms which have proven a robust EPS Development Fee [FWD]: 9 out of the 12 particular person firms have proven constructive EPS Development Charges [FWD], strengthening my thesis that the likelihood of a dividend minimize is comparatively low. Decreased firm particular focus threat: Even when allocating Schwab U.S. Dividend Fairness ETF throughout the businesses it’s invested in, no single firm accounts for greater than 5.5% of the general funding portfolio. This means a lowered company-specific focus threat. Diversification over sectors: When allocating Schwab U.S. Dividend Fairness ETF throughout the sectors it’s invested in, just one sector (the Financials Sector with 35.31%) accounts for a bigger proportion of the general portfolio. All different sectors signify lower than 15% of the general funding portfolio. Diversification over industries: No Business accounts for greater than 15% of the general portfolio (apart from the ETF Business), as soon as once more highlighting the portfolio’s lowered industry-specific focus threat. Geographical Diversification: Nearly all of firms in The Dividend Revenue Accelerator Portfolio come from america (91.1%). Nonetheless, it has nonetheless achieved some geographical diversification. Diversification over Fairness Types: The Dividend Revenue Accelerator Portfolio is diversified throughout Fairness Types. Nonetheless, the most important proportion are large-cap firms with a deal with worth, once more indicating a lowered threat stage for buyers.

Weaknesses Of the Dividend Revenue Accelerator Portfolio’s Present Composition

Sector-Particular Focus Danger because of the Financials Sector’s Massive Share of The Total Portfolio

I consider that the substantial presence of the Financials Sector in The Dividend Revenue Accelerator Portfolio’s composition is at the moment the first threat issue for its buyers. The Financials Sector at the moment accounts for 28.32% of the general portfolio (and even 35.31% when allocating Schwab U.S. Dividend Fairness ETF throughout the sectors it’s invested in).

To mitigate this threat, I’ll moreover diversify the portfolio within the coming weeks and months by incorporating firms from different sectors.

Nonetheless, you will need to observe that I don’t see the heavy allocation within the Financials Sector as a big threat for long-term buyers, since I consider components that might presumably negatively have an effect on the Financials Sector can be predominantly non permanent.

I’m assured that over the long run, the Financials Sector gives buyers with engaging funding alternatives and I plan to take care of a big allocation to it for The Dividend Revenue Accelerator Portfolio. Nonetheless, the allocation shall be barely lowered from its present stage.

The Portfolio Is Presently Completely Invested in Equities With No Allocation to Mounted Revenue

One other weak spot of the present composition of The Dividend Revenue Accelerator Portfolio is its unique allocation to equities, with no allocation to fastened revenue.

Nonetheless, you will need to observe that over the long run, fairness investments provide the potential for a better return in comparison with fastened revenue (like company bonds or authorities bonds, for instance).

It’s additional price noting that I don’t see the absence of fastened revenue belongings in The Dividend Revenue Accelerator Portfolio as a big threat issue, so long as you make investments over the long run, following the long run funding method of The Dividend Revenue Accelerator Portfolio.

Nonetheless, to additional scale back the chance stage of The Dividend Revenue Accelerator Portfolio, I’m contemplating including fastened revenue belongings sooner or later.

Conclusion

On this article, I’ve proven you an idea for the development of a broadly diversified dividend portfolio, which successfully combines dividend revenue and dividend progress whereas offering buyers with a excessive likelihood of reaching engaging funding outcomes, given its lowered threat stage.

The Dividend Revenue Accelerator’s Engaging Mixture of Dividend Revenue and Dividend Development

The Dividend Revenue Accelerator Portfolio remains to be in its development part, and I’ll incorporate further firms within the following weeks and months.

Nonetheless, I consider that the portfolio already gives buyers with a sexy mixture of dividend revenue and dividend progress, which is mirrored in its Weighted Common Dividend Yield [TTM] of 4.69% and 5 12 months Weighted Common Dividend Development Fee [CAGR] of 9.03%, making the portfolio the perfect selection for these searching for to mix dividend revenue with dividend progress.

The Dividend Revenue Accelerator’s Decreased Danger Stage Resulting from Its Broad Diversification and Its Inclusion of Firms With Low Beta Components

As well as, I’ve proven that the portfolio is extensively diversified, providing buyers a broad diversification throughout firms, sectors and industries. That is the case even when allocating Schwab U.S. Dividend Fairness ETF to the businesses and sectors it’s invested in. This means a lowered company-specific and sector-specific focus threat. The portfolio’s lowered threat stage is additional underscored as a consequence of its priorization of large-cap firms with a deal with worth, which signify 40% of the general portfolio.

The inclusion of firms with a low Beta Issue, equivalent to British American Tobacco (60M Beta Issue of 0.33), Johnosn & Johnson (0.58), AT&T (0.71), Royal Financial institution of Canada (0.79), Philip Morris (0.8), and Realty Revenue (0.87) moreover underlines the portfolio’s lowered threat stage.

I’ll proceed investing $400 every month to The Dividend Revenue Accelerator Portfolio, incorporating further firms to additional improve its diversification and scale back its threat stage.

The Dividend Revenue Accelerator’s Excessive Potential for Engaging Funding Outcomes

The lowered threat stage of The Dividend Revenue Accelerator Portfolio will assist us to succeed in favorable funding outcomes with a excessive likelihood. This makes The Dividend Revenue Accelerator Portfolio a excessive potential dividend portfolio in my view.

Creator’s Word: It could be nice to listen to your opinion on the present composition of The Dividend Revenue Accelerator Portfolio. Which firms do you assume would finest align with the funding method of The Dividend Revenue Accelerator Portfolio?

{kind=link}