Stockernumber2/iStock through Getty Photographs

Earlier than we dive in, I simply wish to remind readers that I have been carefully following and have invested in Kirkland’s Inc. (NASDAQ:KIRK) at numerous factors previously, beginning again in Could 2020.

Enclosed beneath are the 5 public website articles I’ve written on Kirkland’s.

Searching for Alpha

The primary write up was in late Could 2020, and revealed at $1.14 per share. As I continued work on the title, I wrote an replace piece two weeks later, in early June 2020. Then, later within the month, again mid June 2020, I had the prospect to interview the then new CEO Steve ‘Woody’ Woodward. As I had a giant Actual Property Renaissance thesis, arguably many months earlier than a number of the greatest minds on Wall Avenue, KIRK was one in all names in my high names, in my lengthy basket. Furthermore, as a part of a strategy to play that actual property renaissance thesis, I beloved Kirkland’s valuation and was impressed by Woody, so I loaded up on the inventory between $1.75 and $2.25. Over the subsequent six to 9 months, KIRK’s EBITDA energy exploded upwards, as they did the truth is meaningfully profit from the COVID induced actual property renaissance together with quite a lot of favorable enterprise modifications made by administration.

Lo and behold, from the preliminary $1.14 inventory value, trough to peak, and once more pushed by then report earnings energy (this wasn’t a Meme inventory), KIRK shares went on soar to over $30, throughout the first half of 2021. Candidly, I began promoting some shares at $7 and bought the vast majority of shares, between $11 and $12. A pleasant 4 to six bagger (on my common value foundation) and one in all my greatest realized share wins of my younger profession (as of at the moment, I am solely 43 and hope to have one other 40 nice years forward). That stated, promoting out between $11 and $12 meant lacking a 15 or 16 bagger.

In September 2022, after being on the sidelines for just a few years, round $3 per share, I acquired again on the horse. I feel I used to be within the inventory for just a few months, however the turnaround was slower to develop than I anticipated and I ended up taking a 15% loss, round $2.50.

Constancy

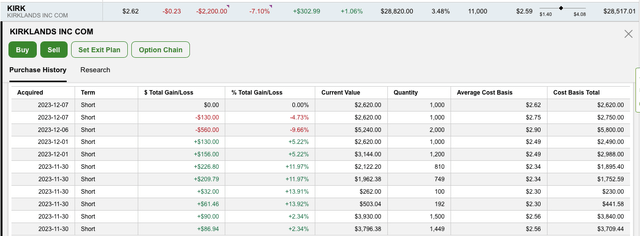

Having been on the sidelines since, on November 30, 2023, after listening to KIRK’s Q3 FY 2023 convention name, I purchased again into Kirkland’s, at round $2.50 per share. By December 4, 2023, or solely three buying and selling days later, KIRK shares leapt as excessive as $3.54, leading to a 40% unrealized achieve. I did promote 30% of my place, at $3.35, however beginning shopping for it again, between $2.62 and $2.90. Due to this fact, and you’ll see beneath, through my Constancy account snapshot, I feel KIRK shares are value $4, and presumably $5 plus, in any other case I might have merely printed the 35% to 40% winner, in three buying and selling days, and moved on.

See right here:

My Constancy Present Lengthy Place in Kirkland’s

Sorry prematurely for the slightly lengthy introduction. Nonetheless, I consider it’s extremely related, because it establishes that I have been carefully following Kirkland’s since Could 2020. Secondly, has I’ve kind of spherical tripped, albeit briefly, a 40% unrealized winner (by holding 70% of the place), I determine it’s value sharing my December 1, 2023 write up, initially written to my Investing Group’s members, now with the broader SA viewers. To that finish, enclosed beneath is that write up, from December 1, 2023. (I’ve solely up to date just a few minor items to replicate a barely completely different inventory value and upwardly revised analyst estimates).

This Certain Seems And Feels Like An Inflection Level

Merely put, I am about 85% to 90% assured that Kirkland’s, Inc.’s administration has put in a movement all the components required for a profitable turnaround. Regardless of the troublesome macro backdrop, we’re seeing clear and compelling proof of ‘inexperienced shoots’.

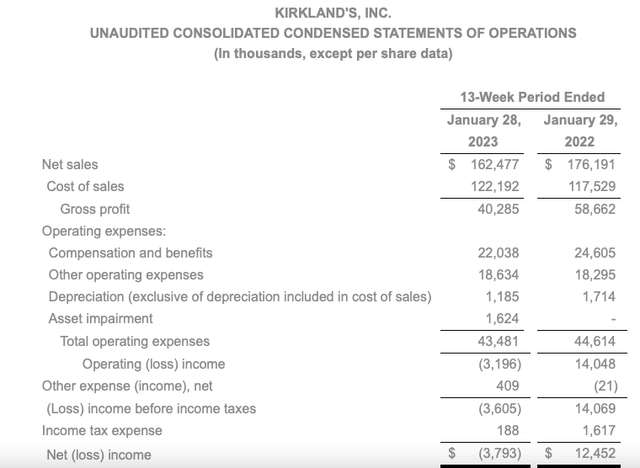

Let’s begin with valuation. As of November 25, 2023, KIRK has 12.92 million shares excellent.

KIRK’s Q3 FY 2023 10-Q

So $2.62 per share x 13 million shares equals a market capitalization of solely $34 million.

As the top of Q3 FY 2023 (October 28, 2023), KIRK had $5.8 million of money, $105 million of stock, $55.7 million of accounts payables, and $62 million drawn on its revolver.

So pro-forma, on the finish of October 2023, we’re speaking about an enterprise worth of $67.5 million.

Nonetheless, and KIRK’s November 30, 2023 press launch, KIRK had a improbable November 2023. Particularly, they had been capable of pay down $27 million on the revolver!

See right here:

As of October 28, 2023, the Firm had a money stability of $5.8 million, with $62.0 million of excellent debt below its $90.0 million senior secured revolving credit score facility. As of November 30, 2023, the Firm had $35.0 million of excellent debt below its senior secured revolving credit score facility.

(Supply: Kirkland’s Q3 FY 2023 earnings launch)

The Trajectory Of Q3 Comps And Site visitors

On Kirkland’s Q3 FY 2023 convention name, we discovered that the trajectory of comps improved properly by the quarter.

Site visitors:

Aug.: -14% Sept.: -6% Oct.: -4%

Comps:

Aug.: -13% Sept.: -9% Oct.: -6%

In consequence, our omnichannel visitors declines improved from down 14% in August to down 6% in September, and down 4% in October. Our Q3 comparable gross sales improved from down 13% in August to down 9% in September to down 6% in October.

(Supply: Kirkland’s Q3 FY 2023 convention name)

Now get this……

In November, comps had been up low single digits and visitors was constructive for the primary month all 12 months!

We had been capable of reduce our ecommerce visitors decline from detrimental 17% within the first half of the fiscal 12 months to solely detrimental 3% in October. On the brick-and-mortar entrance, we improved visitors from a decline of 11% throughout the first half of the fiscal 12 months to down 4% in October. In November, visitors to our shops stayed constructive for the primary time in 2023.

(Supply: Kirkland’s Q3 FY 2023 convention name)

See right here:

In consequence, we’re inspired by a low single-digit improve in comparable gross sales at a a lot improved merchandise margin in November, which incorporates Black Friday.

(Supply: Kirkland’s Q3 FY 2023 convention name)

Wait…..it will get higher:

In This fall FY 2024, November was the hardest comp month to lap. Their upcoming December 2023 and January 2024 comps are a lot simpler, at down 11% and down 8%, respectively!

As a reminder, November was the hardest month-to-month gross sales comparability to final 12 months when comps had been flat. Final 12 months, December comps had been down 11% and January comps had been down 8%. Site visitors additionally turned constructive in November, however we stay cautious about assuming the identical pattern for the remainder of the quarter, given continued macro uncertainty.

(Supply: Kirkland’s Q3 FY 2023 convention name)

Right here Is One other Huge Constructive: They Have Taken $10 million (YTD) of prices out of the enterprise!

For the year-to-date, working bills are down roughly $10 million versus the identical 9 months for 2022. We count on working bills to be down once more in This fall versus the prior 12 months when adjusted for the extra week on this 12 months’s retail calendar.

(Supply: Kirkland’s Q3 FY 2023 convention name)

When you’ve spent any time modeling KIRK then you definitely shortly notice that this enterprise is tremendous torqued to rising its comps. That’s simply how its financials transfer, at the very least traditionally.

See right here:

In consequence, we count on a strong year-over-year enchancment in adjusted EBITDA for the fourth quarter. Within the fourth quarter of 2022, adjusted EBITDA was $2.6 million.

(Supply: Kirkland’s Q3 FY 2023 convention name)

Qualitative ‘Inexperienced Shoots’

(All quoted supplies is from Kirkland’s Q3 FY 2023 convention name.)

Exhibit A – Merch Margins Are Up

The 5 elements of this year-over-year change had been as follows; first, merchandise margin elevated 110 foundation factors to 54% versus 52.9% within the prior 12 months quarter. Decrease freight charges and stock ranges, together with improved product circulation, drove the rise in merchandise margin.

Exhibit B – Successful Again Lapsed Prospects

Throughout the quarter, we proceed to see different promising indicators from the pivot in our advertising technique. It’s mission-critical for us to reengage our loyal buyer and we’re very inspired to see a 20% improve in lapsed buyer reactivation throughout Q3. We’re seeing sequential enchancment in visitors and conversion with much less discounting and improved profitability. We consider these developments are a results of the strategic shift in product combine and advertising.

Exhibit C – Leaner And Cleaner Stock Coming Into This fall

See right here:

Shifting the main focus to operations. Now we have continued to enhance our self-discipline and accuracy in our stock circulation. We ended Q3 with 17% much less stock than final 12 months, together with being in inventory and on time with merchandise for the vacation season, placing us in good place to fulfill the calls for of our peak season.

Our provide chain efficiencies are persevering with to extend by efficient use of expertise, contract negotiations, and course of enhancements. For instance, we closed our two ecommerce hubs and have consolidated our ecommerce operations in our Jackson, Tennessee distribution heart.

And right here:

With extra normalized ranges of stock this 12 months, our provide chain has stabilized, permitting us, with the assistance of course of enhancements in labor administration, to realize roughly $500,000 in financial savings in Q3.

Exhibit D – Well Taking Out Prices

Our provide chain efficiencies are persevering with to extend by efficient use of expertise, contract negotiations, and course of enhancements. For instance, we closed our two ecommerce hubs and have consolidated our ecommerce operations in our Jackson, Tennessee distribution heart.

Exhibit E – Clear Line Of Sight To 30% Gross Margins in This fall

On the opposite elements, we proceed to enhance our provide chain effectivity. I feel that is going to be in our favor within the fourth quarter. And if we are able to get some topline momentum to proceed by the remainder of the quarter, I feel we’d get again to not these historic ranges, however definitely into that 30% vary within the fourth quarter on gross revenue, and it’ll rely upon the leverage and the gross sales outcomes as to how effectively we do, plus or minus. However I simply assume the general positioning is best coming into this 12 months as you take a look at that to final 12 months.

Exhibit F – Getting Again To The Fundamentals

And I feel the pricing, together with furnishings acquired too excessive for our clients. So, we actually turned that one fully the other way up, acquired again into kind of fundamentals and high-value, high-unit velocity gadgets and noticed a ton of success there.

You’ve got heard me point out a few instances the impression and the significance of the seasonal enterprise for us right here. And I might say one form of is a story of two tales. If you consider Q3, Halloween had only a runaway success, most likely the quickest and earliest season demand that we’ve got seen for that enterprise in my time right here.

Exhibit G – Getting Again To The Fundamentals (Half 2)

After which the opposite factor I might say is I discussed the reward and kind of impulse class. And you have been with us lengthy sufficient to know that was once a extremely necessary a part of our enterprise, and we reintroduced that this This fall and it is doing superb.

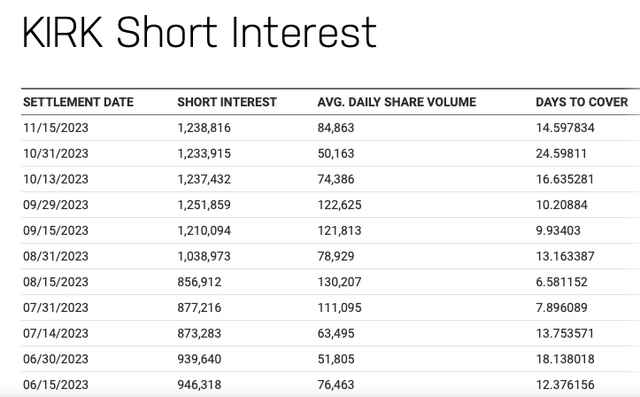

Quick Curiosity

Though the quick curiosity is not GameStop (GME) like, it’s a bit elevated, at simply shy of 10% of all the share rely.

As a fast throwback, as I’ve written as regards to quick squeezes, on occasion, enclosed is a snapshot from my April 2020 quick squeeze article on GameStop.

Searching for Alpha archives

Nasdaq.com

Primary And Again Of The Envelop Modeling

Final 12 months, in This fall, KIRK posted $162.5 million of gross sales, or a down 6.1% comp and gross margins had been a disgusting low 24.8%.

When you mannequin a 4% improve in comps given the strong November, enterprise momentum, and the better December and January comparisons, you arrive at one thing like $168 million of This fall gross sales (pro-forma FY 2024).

30% x $168 million equals $50.4 million of gross margin {dollars}. With $10 million of run charge working expense taken out of the enterprise, $40 million of SG&A is feasible in comparison with final 12 months’s $43.5 million.

There was $62 million on the revolver, as October 28, 2023, however $27 million has been paid down, in November 2023. So SOFR +250 Bps is about 8%. Based mostly on this, This fall FY 2023 curiosity expense needs to be not more than $1.2 million, for the quarter.

So working earnings of $10 million much less $1 million of curiosity expense plus loss carried ahead and now we’re cooking with fuel. Relying in your tax charges assumptions, it believable they may put up a $0.50 to $0.60 This fall FY 2024 EPS determine.

Kirkland’s IR

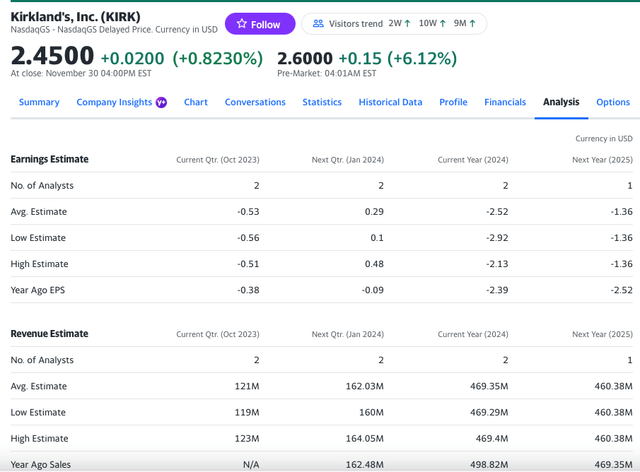

Lo and behold, as of November 30, 2023, the road was solely modeling a $0.29 of This fall EPS and no progress in gross sales.

Yahoo Finance, as of November 30, 2023

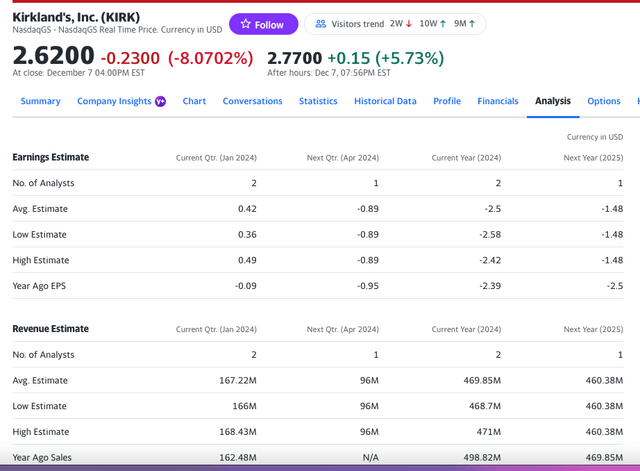

By the way, and subsequently to KIRK’s November 30, 2023 convention name, analyst estimates have been elevated, to $0.42 in EPS (from $0.29) and income estimates have been lifted to $168 million (from $162 million).

See beneath:

Yahoo Finance (as of December 7, 2023)

Dangers

Though I am actually excited and inspired by Kirkland’s Q3 FY 2023 convention name, notably its improbable November 2023, which confirmed a serious debt pay down and plain enterprise momentum, Kirkland’s must show it to the road, and Mr. Market, that they will ship in each calendar December 2023 and January 2024. Secondly, though its debt stability is manageable, that is nonetheless a leveraged enterprise is that dropping a bit of bit of cash. With a really small market capitalization of solely $34 million, there may be restricted margin of security right here. Kirkland’s should proceed apace on its turnaround in an effort to re-established its mid-single digit EBITDA energy, in FY 2024, which is required to shore up its stability sheet. Lastly, as this goes with out say, as it is a small retailer, with simply shy of $500 million of annual gross sales, the corporate is at all times topic to macro headwinds, in addition to merchandising and executional dangers.

Placing It All Collectively

About three weeks in the past, KIRK shares had been circling the drain and altering palms round $1.50 per share. Sure, the inventory is up a few $1 per share, in a brief time period. Nonetheless, that’s solely a $13 million transfer in market capitalization, given the very tiny share rely right here. Secondly, the pay down within the revolver, of $27 million, in a single month’s time, is way quicker than the road anticipated.

Lastly, for the primary time in ages, KIRK’s enterprise has some actual turnaround momentum and the brand new CEO has appropriately course corrected and reengaged with its lapsed clients base within the face of a a lot more durable macro backdrop. Woody was the suitable CEO, for that second in time, throughout the Actual Property Renaissance, again when client discretionary spending on furnishings and residential decor was strong. Submit the growth to bust of the enterprise cycles, Kirkland’s new administration group has well course corrected and set off on a wiser and higher enterprise path, a plan that matches up significantly better with a more durable macro again drops and the place they’re carry on a regular basis worth and contemporary selection to interact and win again its buyer base.

To make an extended story quick, I feel it’s logical to recommend a robust case could be made that KIRK shares are value $4, with a shot at $5. Once more, there are solely 13 million shares excellent, the quick curiosity is considerably elevated, and Mr. Market (outdoors of a small variety of sizzling cash day merchants) is sluggish on the uptake right here. Kirkland’s turnaround seems and feels actual, at the very least to me. We will see once they report This fall numbers, in mid March 2024.

Editor’s Notice: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

{kind=link}