chaofann

Co-produced by Austin Rogers

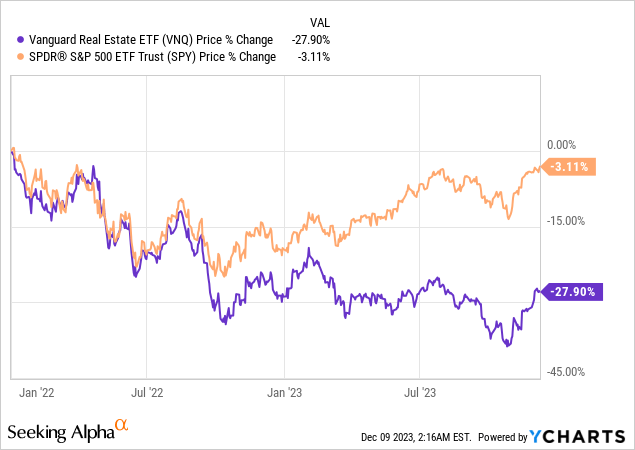

Investor sentiment about actual property funding trusts (“REITs”) is decrease than it has been because the Nice Monetary Disaster of 2008-2009.

That has translated into a large divergence in efficiency between the general public actual property sector (VNQ) and the S&P 500 (SPY):

Over the previous 2 years, REITs have underperformed the market by practically 25 share factors, even after the current rebound!

As we’ve got completed many occasions previously, we remind buyers that this enormous divergence in worth efficiency doesn’t signify basic weak point however relatively merely investor pessimism.

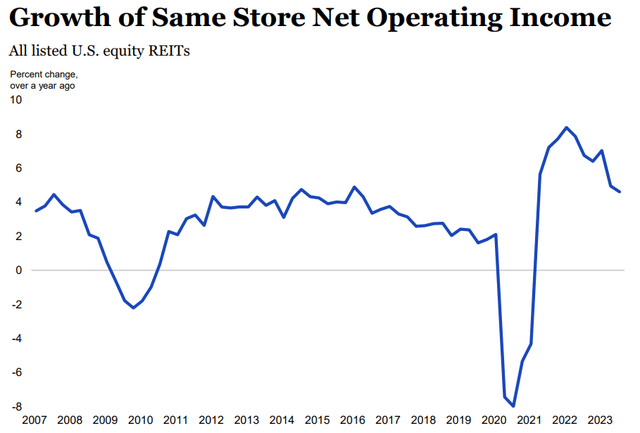

Take into account just a few information about REITs, courtesy of NAREIT:

REITs’ common loan-to-value ratio sits at about 36%. REITs’ weighted common debt time period to maturity is 6.5 years. 91% of REITs’ debt is fixed-rate. Due to the above elements, REITs’ weighted common rate of interest on debt is just 4.0%. Identical-store / comparable-property web working earnings (“NOI”) continues to rise.

Rising rates of interest are a headwind for REITs, however they’re a extra modest headwind than many buyers suppose. And they’re felt with a lag. Increased rates of interest create incrementally growing curiosity bills, whereas lease progress is felt a lot quicker.

Therefore we discover that REITs’ same-store NOI progress continues at a robust tempo of about 5% YoY in Q3 2023. That’s greater than at virtually any level within the final 15 years!

NAREIT Q3 2023 T-Tracker

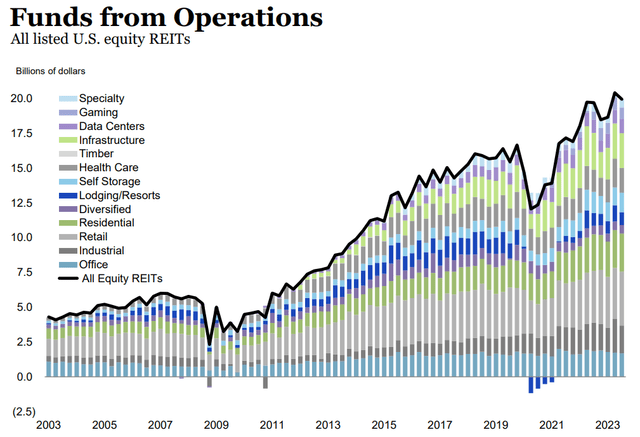

However, in fact, NOI doesn’t account for curiosity bills. One would possibly object that SSNOI seems to be solely on the optimistic facet of the equation for REITs whereas ignoring the rising bills from curiosity funds.

Funds from operations (“FFO”) does incorporate curiosity prices. In terms of FFO, once more, whole REIT earnings are close to an all-time excessive and proceed to develop:

NAREIT Q3 2023 T-Tracker

You’ll suppose that this backdrop would result in at the least a considerably optimistic investor sentiment towards REITs. However the reverse is true.

Valuations have compressed considerably and are actually at close to their lowest ranges because the nice monetary disaster.

This valuation would possibly make sense in a “greater for longer” situation during which rates of interest go even greater and keep there for longer. However the probability of that situation taking part in out seems to be falling every single day as inflation slides downward and the financial system weakens.

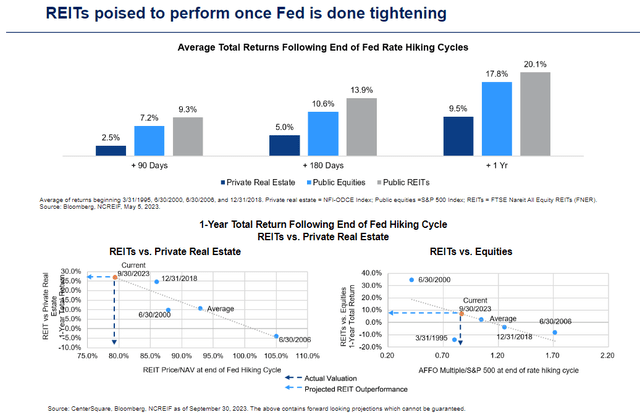

A consensus is forming that the Federal Reserve is totally completed with fee hikes and that the subsequent Fed transfer can be a fee minimize.

Traditionally, REITs have strongly outperformed within the 3-12 months following the definitive finish of fee hikes.

CenterSquare

We don’t see any cause to consider this time can be totally different.

In truth, given the extent of underperformance REITs have suffered over the previous few years, we consider REITs ought to outperform the broader inventory market by a big diploma within the subsequent yr.

However not all REITs will carry out equally nicely, in fact. Some may have a tepid restoration, whereas others will soar, producing enormous features for individuals who opportunistically purchased in the course of the downturn.

Listed below are two of these REITs that we expect will rebound magnificently within the quarters and years forward. We really consider the present costs signify once-in-a-decade shopping for alternatives.

1. Alexandria Actual Property Equities (ARE)

ARE is a REIT each dividend progress investor ought to at the least be conversant in. With over 30 years of sectoral focus, the corporate has established itself because the main landlord-developer of Class A, state-of-the-art, unbeatably positioned life science actual property in america. These are buildings used for biotech analysis and improvement.

ARE would not simply personal standalone life science buildings. They personal multi-building campuses that profit from the innovation-enhancing results of clustering collectively, sometimes adjoining to world class analysis universities.

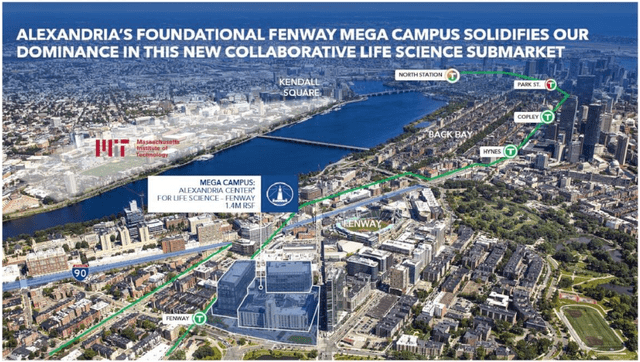

Take, for instance, ARE’s mega-campus positioned proper throughout the bay from MIT and only a brief stroll from Fenway Park in Boston, Massachusetts, maybe essentially the most preeminent life science market on the earth.

ARE Presentation

Or take ARE’s near-monopoly on life science properties straight adjoining to UC San Francisco.

ARE Presentation

ARE’s inventory worth has dropped ~45% because the starting of 2022, largely as a result of the market is anxious in regards to the quantity of latest life science actual property properties beneath improvement. COVID-19 spurred a giant wave of latest improvement on this house. Plus, the market fears {that a} steady provide of conventional workplace buildings can be transformed into life science amenities within the coming years, including additional to the provision glut.

What we consider the market misunderstands is that location, constructing high quality, and landlord reliability are collectively a strong aggressive benefit.

The areas seen above are very near world class analysis universities, from which biotech firms can faucet a steady output of scientists. Furthermore, these are all supply-constrained markets with restricted out there land or redevelopment alternatives close to the locus of innovation.

Furthermore, constructing high quality is immensely necessary in attracting biotech tenants. ARE designs its buildings to be extremely safe and power environment friendly? That latter component is necessary as a result of life science analysis requires lots of power utilization.

Lastly, ARE has established itself as a number one life science landlord over the past three many years. Put merely, “Alexandria” means high quality on this house. ARE has model energy.

Many of the new provide of life science house getting into the market will not be straight aggressive with ARE due to its subpar location, constructing high quality, or landlord belief.

Add to this ARE’s top-notch steadiness sheet power as outlined by these metrics…

ARE Presentation

…and you have a REIT that exudes power on each side of the steadiness sheet.

By way of valuation, ARE has not been practically this low-cost because the Nice Monetary Disaster.

ARE at the moment trades at a strikingly low 11.6x AFFO. That is virtually half of its common (not peak!) P/AFFO ratio of about 21.5x from the final 5 years. Simply reverting to its 5-year imply would generate an 85% upside, however even when ARE solely returned to a 18x valuation a number of, the upside remains to be excessive at 55%.

And that is on prime of an virtually 5% dividend yield and mid-single-digit AFFO per share progress!

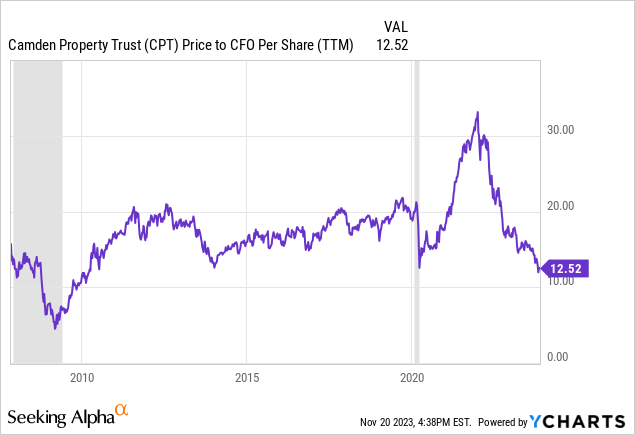

2. Camden Property Belief (CPT)

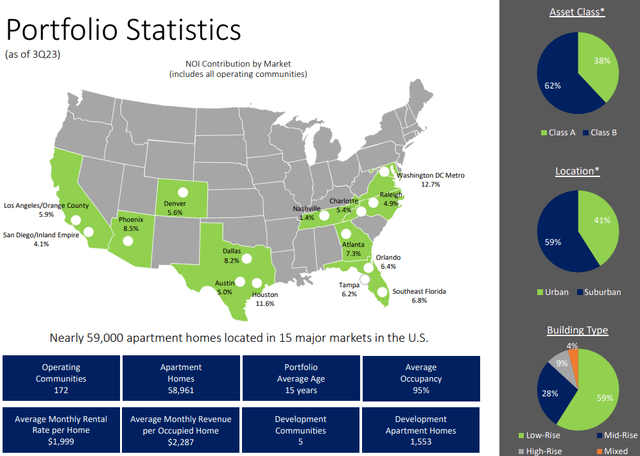

CPT is a blue-chip multifamily landlord-developer within the Sunbelt. Except for publicity to Washington DC and Denver, CPT is fully centered on the fast-growing Sunbelt area with a closely diversified portfolio.

CPT Presentation

As a result of decrease prices of dwelling, decrease taxes, and higher job progress, the Sunbelt area has loved a robust inhabitants inflow lately and certain will proceed to take action for the foreseeable future.

CPT stands to realize from this, whether or not persons are transferring into city areas (41% of the portfolio) or suburban areas (59%), whether or not they go for greater lease Class A flats (38%) or reasonably priced Class B models (59%).

CPT even has just a few irons within the single-family build-to-rent hearth by means of two SFR developments in Texas.

Simply as for ARE, the market’s main concern with CPT is the wave of latest provide coming to market over the subsequent yr or so. However once more, location inside every particular person market is a aggressive benefit for CPT, as a result of the perfect areas in most cities have already been constructed out, leaving primarily the much less nicely positioned land for improvement.

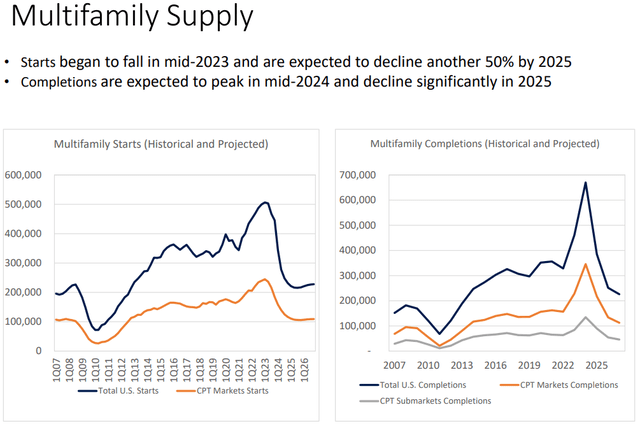

Furthermore, due to the sharp enhance in rates of interest over the past yr, new multifamily begins have fallen off a cliff, which signifies that in 2025 and after, completions needs to be even decrease than in the course of the post-GFC interval from 2014 by means of 2022.

CPT Presentation

Which means that there’s mild on the finish of the tunnel. Provide headwinds are short-term, whereas inhabitants progress and housing unaffordability are longer-term tailwinds.

The market additionally appears to fret about the truth that 23% of CPT’s debt is floating fee, however administration is unperturbed, viewing the present interval during which short-term charges are greater than long-term charges as an anomaly that will not final without end.

CPT’s A- credit standing speaks to its steadiness sheet power.

That is one other REIT buying and selling at a once-in-a-decade low valuation.

The REIT’s present worth/core FFO of 13.0x sits nicely beneath its 5-year common of 20.5x, implying an upside of 58% if CPT simply returns to its current common valuation. However even simply getting again to an 18x a number of would generate roughly a 40% inventory worth upside on prime of CPT’s 4.5% yield and mid-single-digit progress fee.

Backside Line

The rising rate of interest cycle has dealt a heavy blow to investor sentiment towards REITs. However fundamentals have held up simply superb, and because the narrative modifications from “rising charges” to “falling charges,” REITs ought to take pleasure in a pleasant interval of outperformance.

Do not take our phrase for it. Take a look at the historic file.

Proper now, REITs are neglected in favor of bonds and mega-cap tech shares, however that will not all the time be the case. We’re assured that REITs will take pleasure in their time within the solar once more.

Within the meantime, we are going to preserve loading up on these once-in-a-decade alternatives.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}