designer491

By Jeffrey Schulze, CFA, Head of Technique

Trajectory of Labor Market, Inflation Key Areas to Watch

The U.S. economic system has persevered via the strongest financial tightening cycle for the reason that early Eighties, with 100 foundation factors (bps) of further charge hikes in 2023, following 425 bps in 2022. Nevertheless, we predict the following three quarters (inclusive of the present one) would be the crux of this cycle, the toughest a part of a climb the place all probably the most tough strikes are concentrated. We count on the lagged results of Fed tightening to weigh on the economic system within the first half of subsequent yr, and we proceed to take care of our base case of a recession till we get via this era.

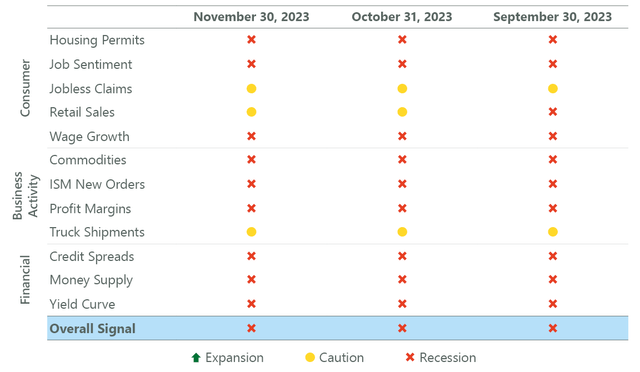

We had been nicely inside the consensus view final yr in calling for what turned “probably the most anticipated recession ever.” But 12 months later, we’re nonetheless awaiting a significant downturn in financial exercise. Our North Star, the ClearBridge Recession Danger Dashboard, has now been flashing a pink or recessionary sign for 16 months. At current, there are 9 pink and three yellow indicators, which offer the inspiration for our base case views whilst consensus has shifted into the tender touchdown camp (Exhibit 1). Importantly, an extended length between the preliminary pink sign and a recession taking maintain just isn’t remarkable, because the economic system doesn’t all the time take a straight line down.

There are a lot of potential the explanation why the economic system held up higher than anticipated this yr, together with a strong labor market that has supported consumption and impressive fiscal spending packages nonetheless making their manner via the economic system’s bloodstream. We count on these optimistic impulses to dampen in 2024, setting the economic system on a extra fragile footing because the calendar turns over. One other threat the economic system will probably be going through within the new yr is the delayed impact of financial tightening, which famously acts with lengthy and variable lags. Given excessive inflation and ultra-low charges, financial coverage probably didn’t attain restrictive territory till the tip of 2022, that means the complete results of upper charges ought to proceed to weigh on the economic system within the first half of 2024, given frequent knowledge of lags to financial coverage ranging as much as 18 months.

Exhibit 1: ClearBridge Recession Danger Dashboard

ClearBridge Investments

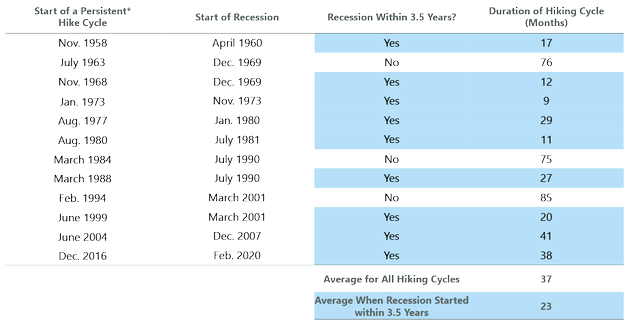

Whereas a recession was the consensus view final yr, with the advantage of hindsight, it was probably untimely to count on one. Historical past reveals that, for the reason that late Nineteen Fifties, it takes a median of 23 months from the preliminary charge hike of a persistent mountaineering cycle to the start of an financial downturn. Whereas it could really feel just like the Fed has been mountaineering for an eternity, the primary hike of this cycle got here solely round 20 months in the past, that means we’re nonetheless wanting the historic common.

Exhibit 2: Lengthy and Variable Lags

*A Persistent Hike Cycle is the interval when nearly all of Fed charge hikes happen in a tightening cycle. The date of the preliminary charge hike within the tightening cycle could not align with the beginning of the Persistent Hike Cycle. (FactSet, Federal Reserve)

Some impacts of financial tightening are already weighing on the economic system. In actual fact, the labor market is exhibiting cracks, with our job sentiment indicator – which measures whether or not jobs are laborious to seek out – rolling over, a pattern that has traditionally been adopted by a recession. Whereas the buyer has been rock strong for the reason that pandemic, we’re seeing indicators of stability sheet fatigue by way of rising delinquencies throughout bank cards, auto loans, and even mortgages, together with extra selective spending patterns. And it is vital to notice that consumption has traditionally remained robust proper as much as – and even previous – the beginning of a recession.

We prompt final yr that the Fed’s success in bringing down inflation would decide the probabilities of a tender touchdown. The Fed has made substantial progress, and the annualized six-month charge of core PCE now stands at 2.6%, approaching the Fed’s 2% goal. Nevertheless, it is uncommon in developed markets for inflation to be successfully tamed on the primary attempt with no second wave of worth will increase. The U.S. has endured three main inflation episodes during the last roughly 100 years and all three included a number of waves of inflation; globally the prevalence of a number of waves stands at 87%, in accordance with a current examine from Strategas Analysis Companions. We consider that is entrance of thoughts for the Fed, which can probably err on the aspect of warning, with the higher-for-longer coverage we’re at the moment experiencing one instance of this.

On the optimistic aspect, whereas it’s nonetheless too early to declare victory, inflation is on tempo to return a lot nearer to focus on subsequent yr, taking additional hikes off the desk and elevating the query of cuts to convey the stance of financial coverage nearer to impartial. If the Fed can get extra assured on inflation, in the end that ought to open the door for modest charge cuts in 2024 that might assist spur an improved outlook later within the yr or into 2025.

Jeffrey Schulze, CFA, is Head of Financial and Market Technique at ClearBridge Investments.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}