jetcityimage/iStock Editorial through Getty Pictures

Introduction

A few months in the past, I wrote a sequence of articles protecting a few of the largest medical health insurance firms in america: Humana (HUM), UnitedHealth (UNH), Cigna Group (CI) and Elevance Well being (ELV). As I grew to become aware of insurance coverage operations whereas learning these firms, I wish to diversify my protection of insurance coverage firms with this text on American Monetary Group (NYSE:AFG). I solely stumbled throughout AFG this June when fellow SA contributor Alexander Steinberg wrote about it in this text. After studying a pair extra articles and looking out on the investor relations web site, AFG has been on my watchlist for the previous few months. I wish to use this text (and the analysis it takes to jot down it) to turn into extra aware of the corporate and share my ideas with you.

Enterprise Overview

For an preliminary overview, let me cite from AFG’s most up-to-date 10-Ok submitting:

Subsequent to the sale of its annuity operations, AFG studies its operations as two segments: (i) Property and casualty insurance coverage (“P&C”) and (ii) Different, which incorporates holding firm prices and revenue and bills associated to the managed funding entities (“MIEs”).

Supply: AFG FY2022 10-Ok – Web page 50 (Section Assertion of Earnings)

AFG introduced the sale of its annuity enterprise for whole after-tax money proceeds of $3.5 billion on Could 28, 2021 (AFG’s market capitalization stands at $10 billion as we speak so this was fairly a giant divesture). The proceeds have been used to pay beneficiant particular dividends in FY21 ($28.06 per share) and FY22 ($14.31 per share).

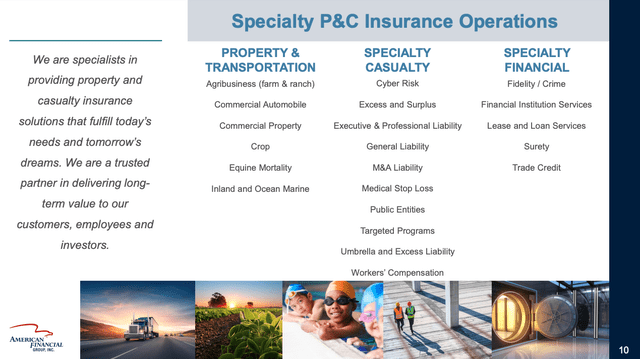

So because the “Different” section solely consists of holding firm prices and bills to MIEs, this leaves us with just one actual section which is Property and casualty insurance coverage (P&C). Here’s a slide from a latest Investor Presentation giving a fast overview of AFG’s choices within the P&C section:

Specialty P&C Operations (BMO Capital Markets Digital Summit Presentation – Slide 10)

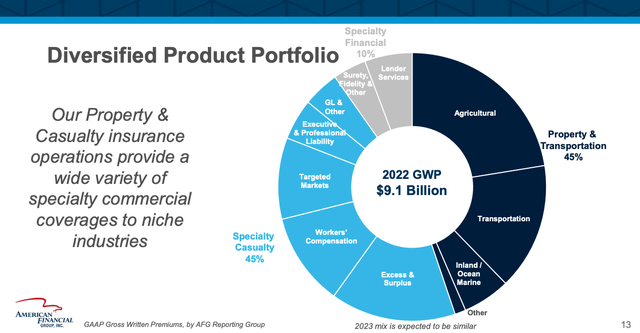

So AFG divides the P&C operations into three sub-segments: (1) Property & Transportation, (2) Specialty Casualty and (3) Particular Monetary. Right here is one other chart from the identical presentation to present you a greater understanding of the size and relevance of those sub-segments:

Gross Written Premiums by sub-segments (BMO Capital Markets Digital Summit Presentation – Slide 13)

Right here we will see that Specialty Monetary is the smallest section whereas the opposite two are of the identical measurement. I’ll solely clarify a few of the largest classes since going over each providing could be a bit an excessive amount of.

The agricultural enterprise provides multi-peril crop insurance coverage protecting most perils in addition to crop-hail, equine mortality and different coverages for full-time working farms/ranches. Transportation provides protection for automobiles comparable to buses and vehicles, different danger switch packages (tailor-made options for purchasers that do not wish to insure 100% of dangers) and different specialty transportation niches.

Extra & Surplus provides protection for distinctive, unstable and hard-to-place dangers like development or roofing. Employees’ Compensation provides protection for advantages payable to workers who get injured on the job (in Germany we name this “Berufsgenossenschaft”, simply in case I’ll have any German readers).

So in conclusion, AFG operates in what you would possibly name area of interest markets. Moreover, AFG’s insurance coverage operations are very effectively diversified on the smaller, sub-segment scale.

How does AFG generate income?

I’ll spend most of my effort on this part as a result of I believe it’s an important one. I’ll begin by giving a superficial overview earlier than diving deeper into this query within the subsequent two sub-sections. AFG generates income from two sources: (1) Underwriting and (2) Web Funding Earnings. They’re intertwined in a number of methods.

(1) Underwriting: When AFG indicators an insurance coverage contract with a buyer, the client pays AFG a premium. This fee is made upfront. Premiums are accounted for as income (additionally known as web earned premiums, extra on that later) within the revenue assertion or unearned premiums on the legal responsibility facet of the steadiness sheet. Concurrently, AFG accounts for anticipated claims (Loss & LAE) out of those contracts on the legal responsibility facet of the steadiness sheet. If we have been to match this to an industrial firm, web earned premiums minus Loss & LAE could be one thing like gross revenue. If we deduct working expenditures (OPEX) from this equation, it could look one thing like this:

Income (or web earned premiums) – Loss & LAE – OPEX (or underwriting bills) = Underwriting revenue/loss

In conclusion, we at all times need web earned premiums to be greater than the mixture of Loss & LAE and underwriting bills. So Key Efficiency Indicators (KPIs) for Underwriting are (1) Gross written premiums, (2) web earned premiums and (3) the mixed ratio (= (Loss & LAE + Underwriting Bills) divided by web earned premiums).

(2) Web Funding Earnings: Any time AFG generates a revenue in underwriting, because of this they’re successfully borrowing cash from their prospects at a adverse fee. The amount of money that the insurer has obtainable for the time between the fee of the premium and the outflow for the settlement of the claims can also be known as “float”. AFG invests this cash within the meantime and generates extra funding revenue. All of this funding revenue is 100% attributable to AFG. KPIs for this a part of earnings are (1) Funding Portfolio Dimension and (2) Funding Portfolio Yield.

Underwriting

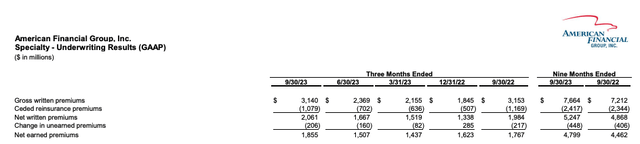

Allow us to begin with accounting and the distinction between the forms of premiums AFG studies of their monetary statements. There are three reported premium numbers: Gross written premiums (GWP), Web written premiums (NWP) and Web earned premiums (NEP), as might be seen within the following screenshot from a slide of AFG’s most up-to-date Q3 2023 Investor Complement:

Varieties of Premiums (AFG Q3 2023 Investor Complement – Web page 7 )

GWP describes absolutely the variety of premiums AFG signed with prospects within the given interval. AFG reinsures a part of these premiums, giving a few of these premiums away in trade for the promise of the reinsurer to take over a few of the future claims/losses. Then, the ensuing NWP are adjusted for “change in unearned premiums”. This comes again to the accounting I discussed earlier. If AFG indicators an insurance coverage contract in March and this contract has a period of 1 yr, solely 10 months (March-December) will probably be accounted for as income whereas 2 months (January and February of the next yr) will probably be accounted for as unearned premiums (a legal responsibility). In January and February of the next yr, these unearned premiums will probably be accounted for as income whereas the legal responsibility disappears. I’ll discard NWP and solely give attention to GWP and NEP.

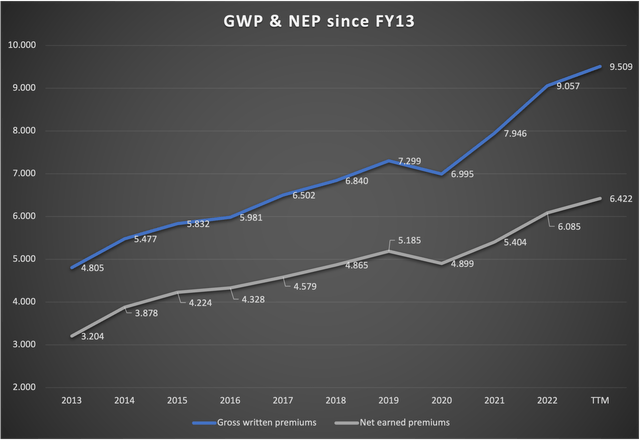

Let’s begin by looking on the improvement of GWP and NEP during the last decade (numbers in $million):

GWP & NEP since FY13 (Firm Experiences – compiled by Creator)

We will see that premiums have grown in each single yr besides FY20 because of the pandemic. We will additionally see that the expansion of premiums accelerated over the previous 2-3 years as a catch-up impact from the pandemic and because of greater inflation (= greater value will increase). The longer-term progress charges are very steady. GWP grew with a CAGR of seven.3% since FY13 and 6.85% since FY17 whereas NEP grew with a CAGR of seven.39% since FY13 and 5.85% since FY17.

Premium progress will at all times be a mixture of three components: (1) Worth will increase, (2) the addition of latest prospects and (3) the retention fee of present prospects. I will not go into any additional element right here as a result of I lack the info and I do not assume that it’s that essential.

So two of the KPIs appear to be in fine condition with a gentle mid-to-high single-digit progress fee. Now let’s check out the third KPI that I discussed which is the mixed ratio. The mixed ratio is one thing just like the EBIT margin for the underwriting. I’ll repeat it right here for readability:

“Industrial Firm” American Monetary Group Income Web earned premiums – prices of gross sales – Loss & LAE = Gross Revenue = Gross Revenue equal – OPEX – Underwriting Bills = EBIT = Underwriting Revenue/Loss Click on to enlarge

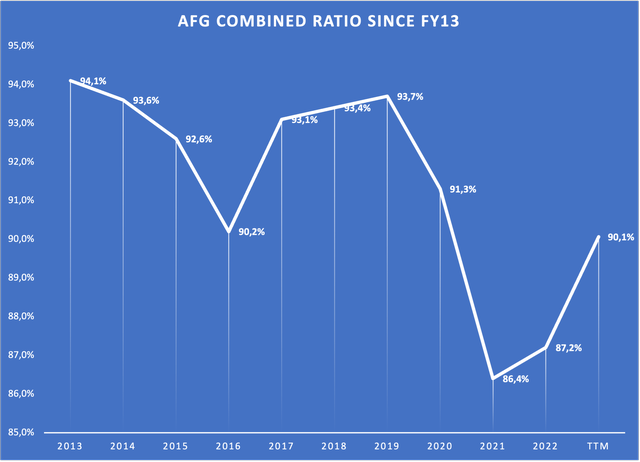

This can be a very unfastened comparability nevertheless it does the job of creating clear how the reporting of underwriting outcomes works. The mixed ratio describes the share of Loss & LAE + Underwriting Expense to the Web earned premiums, so it’s the inverse worth of the Underwriting/EBIT margin. If the underwriting margin is 10%, the mixed ratio is 90%. Right here is an outline of AFG’s mixed ratio over the previous decade:

AFG Mixed Ratio since FY13 (Firm studies – compiled by Creator)

We will see that AFG’s mixed ratio has been beneath 100% yearly, an excellent signal as a result of it exhibits us that AFG persistently generates underwriting income and by doing that, borrows cash from prospects at a adverse fee. We will additionally see that FY21 and FY22 ratios have been outliers, that means that AFG reported very excessive underwriting income in these two years. We presently see a development of normalization, with AFG guiding for a mixed ratio of 91% on the midpoint for FY23, extra according to previous outcomes.

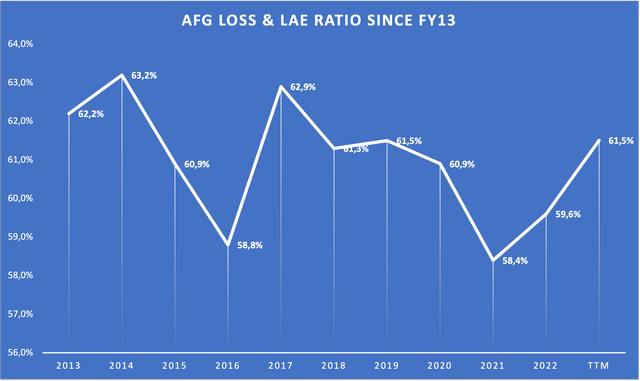

Solely wanting on the mixed ratio is not sufficient. We also needs to check out the 2 components that kind this ratio. Here’s a chart exhibiting the Loss & LAE ratio since FY13:

AFG Loss & LAE ratio since FY13 (Firm studies – compiled by Creator)

The typical is 61.0% and the median is 61.3%. Whereas the Loss & LAE ratio is unstable, it appears to be general steady in the long run. The TTM variety of 61.5% is a bit bit greater than the typical/medium for the previous decade. A steady Loss & LAE ratio is an indication of underwriting prowess, one other good signal.

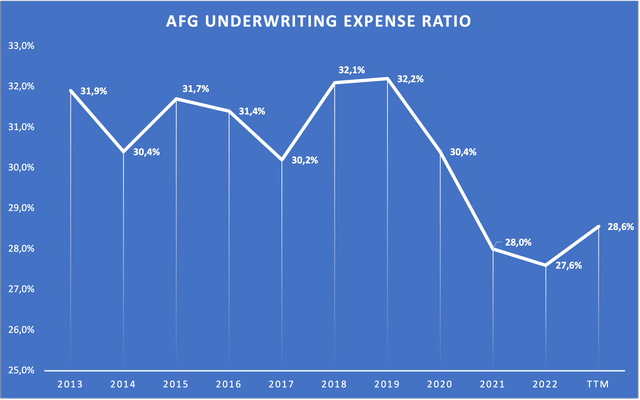

Right here is one other chart exhibiting the underwriting expense ratio:

AFG Underwriting Expense ratio since F13 (Firm studies – compiled by Creator)

That is the place it will get fascinating. We have now seen that AFG reported exceptionally good mixed ratios in FY21 and FY22. Right here we will see that the principle purpose for this was declining underwriting bills. As I stated earlier, we’re presently seeing a normalization of the mixed ratio with AFG guiding for 91% on the midpoint. Sadly I do not know if that 91% steerage assumes an increase in Loss & LAE or underwriting bills. This will probably be fascinating to see within the This autumn 23 earnings report. Nonetheless, even within the present development towards normalization of the mixed ratio, the underwriting expense ratio continues to be at a low degree in comparison with the previous. This might imply two issues: (1) AFG achieved some working leverage over the previous few years or (2) we’ll see an increase within the underwriting expense ratio within the subsequent few quarters/years. I believe the reality lies one thing in between as each statements are most likely right. One other factor that may have been an element is the sale of the annuity enterprise in 2021. Whereas I can not discover a purpose why this might have impacted underwriting expense ratios within the P&C section, I nonetheless assume it’s suspicious that the underwriting expense ratio declined in the identical yr the annuity enterprise was offered and appears to remain on this decrease degree. This would possibly simply be a coincidence although.

To conclude this sub-chapter:

AFG has grown GWP and NEP at round 6% over the previous decade Premium progress has been very regular and there aren’t any causes to count on a deterioration of premium progress going ahead AFG’s FY23 steerage for the mixed ratio is extra according to the previous however nonetheless at a low degree. This may be a future headwind if AFG cannot preserve the underwriting prices on the present degree.

Web Funding Earnings

Now we all know that AFG generates float at a adverse price because of the constant underwriting income. Let’s take a look at what AFG does with this cash. I’ll once more begin with some common issues.

Assuming AFG’s insurance coverage contracts have a period of 1 yr, the funding portfolio ought to roughly have the scale of (1) one yr of web earned premiums + (2) Shareholders’ fairness (assuming AFG invests its fairness capital as effectively). Once more, it is a quite simple approach of it so please do not name me out on this within the feedback.

I’ll simply use FY22 numbers to examine this:

$6,085 million (Web earned premiums)

+ $4,052 million Shareholders’ fairness

= $10,137 million Funding Portfolio Estimate

In the meantime, the Funding Portfolio stood at $14,512 million based on the FY22 steadiness sheet. The distinction is round $4.4 billion So this did not appear to work. What’s the drawback right here?

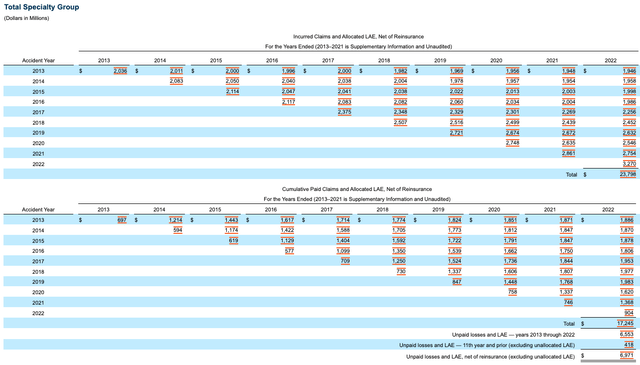

The reply might be present in Word O of the FY22 10-Ok. Let me present you:

Incurred Claims vs. Cumulative Paid Claims (AFG FY22 10-Ok / Word O – Insurance coverage)

This chart appears to be like type of intimidating nevertheless it is not as dangerous because it appears. The highest half exhibits incurred claims for the years 2013-2022 whereas exhibiting the claims for each single yr and the adjusted values to these claims within the following years. The underside half exhibits the quantity of paid claims on a cumulative foundation (once more for each single yr). So for instance we will see that on the finish of FY22, there have been $1,946 million incurred claims for calendar yr 2013, whereas $1,886 million have been paid for these claims all through these years.

Now we have now to have a look at this desk whereas excluding the 2022 numbers:

$23,798 million Incurred claims (2013-2022)

– $3,270 million Incurred claims 2022

= $20,528 million Incurred claims (2013-2021)

$17,245 million Paid claims (2013-2022)

– $904 million Paid claims 2022

= $16,341 million Paid claims (2013-2021)

And now the end result: $20,528 million – $16,341 million = $4,187 million

Which means $4.2 billion of the funding portfolio are a results of unpaid claims for “previous instances”. That is almost the distinction of $4.4 billion I ended up with my simplified calculation above. In conclusion, the Funding Portfolio will at all times be higher than NEP for one yr + shareholders’ fairness which is an effective factor as a result of once more, that is cash borrowed without charge that generates funding revenue for AFG.

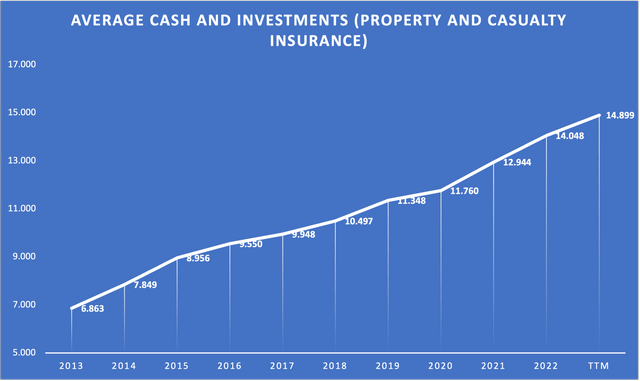

Now let’s check out the essential KPIs I laid out earlier: (1) Portfolio Dimension and (Portfolio Yield). Here’s a chart exhibiting the Portfolio Dimension all through the years:

Funding Portfolio Dimension since FY13 (Firm studies – compiled by Creator)

AFG studies this utilizing averages for every quarter and yr. We will see the scale of the Funding Portfolio has been rising steadily each single yr. The expansion CAGR got here in at 8.28% since FY13 and seven.15% since FY17. So unsurprisingly, the portfolio grew according to the premiums (even a bit sooner). We will count on the portfolio to develop according to premiums at round 6% going ahead.

Right here is the final chart for this chapter:

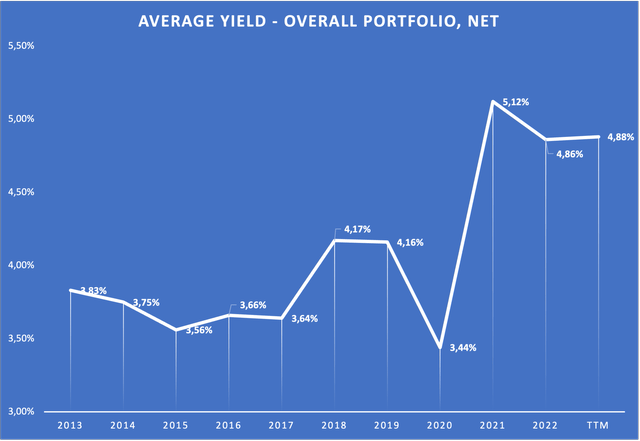

Funding Portfolio Yield ( Firm studies – compiled by Creator)

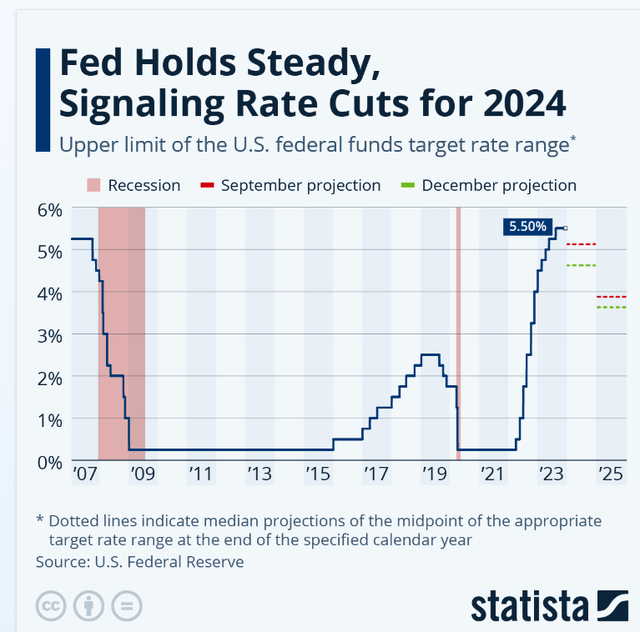

Right here we will see the general web yield of the funding portfolio. We will see that the yield has risen sharply over the previous three years and a bit in FY18 and FY19. If we take a look at the event of the U.S. federal funds fee, we will see that AFG’s portfolio yield strikes according to it:

U.S. federal funds fee (Statista)

Now this might imply two issues: AFG (1) would possibly take a look at greater web funding revenue for years to return (if charges keep elevated) or (2) would possibly take a look at headwinds for the web funding revenue when charges begin declining. I once more assume that it will likely be a mixture of each. I assume that AFG will lock in greater charges in addition to they will with out compromising liquidity to have the ability to pay for incurred claims. So we’d see elevated portfolio yields for a minimum of two years. If charges have been to return down, portfolio yield would finally come down as effectively. There may be nothing AFG can do about it.

In the long run, portfolio yield is nothing else than volatility. So long as the portfolio measurement retains rising according to premiums, a decline within the portfolio yield is a minor concern.

Financials

Let’s begin this chapter as I normally do, by looking at the latest steadiness sheet:

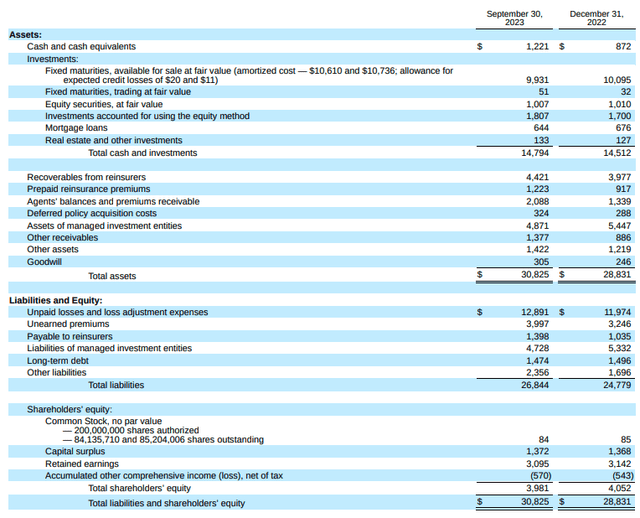

AFG Q3 23 Steadiness Sheet (Q3 23 10-Q Submitting)

We already lined a number of objects by now so I’ll give attention to web debt and goodwill.

We will see that Goodwill solely makes up beneath 1% of whole Belongings, one thing that I wish to see as a result of it exhibits that AFG has been in a position to carry out because it does with out the necessity to carry out overpriced acquisitions. Money and money equivalents presently quantity to $1,221 million whereas long-term debt stands at $1,474 million. This may end in a web debt place of solely $253 million. In line with S&P Capital IQ, web debt stands at $485 million, a bit greater than my quantity. It would not matter although as a result of the web debt quantity is negligible in comparison with AFG’s earnings energy. For the trailing twelve months (TTM), AFG’s major reporting metric which is “Core Web Working Earnings” (extra on that quickly) got here in at $912 million. So AFG’s web debt solely stands at round 0.5x earnings, a really wholesome quantity. In conclusion, AFG’s steadiness sheet appears to be like very wholesome.

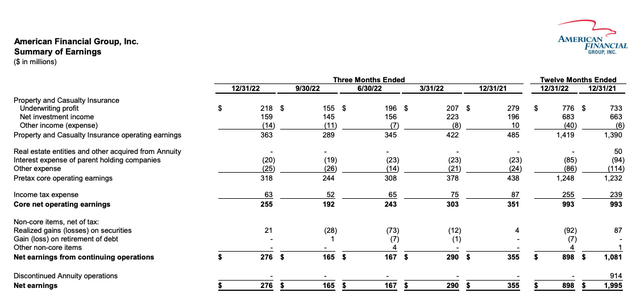

Now let’s flip to earnings metrics and I wish to begin by looking on the aforementioned “Core Web Working Earnings”. Here’s a screenshot from the FY22 Investor Complement doc:

FY22 Abstract of Earnings (This autumn 22 Investor Complement – Web page 4)

Right here we will see what sort of changes AFG makes to web earnings to reach at Core web working earnings. The principle factor, with the others being negligible, is the adjustment for realized good points/losses on securities. This positively is sensible so I’ve nothing to complain about right here. We will use core web working earnings (I’ll name it core earnings any more) as our major earnings metric.

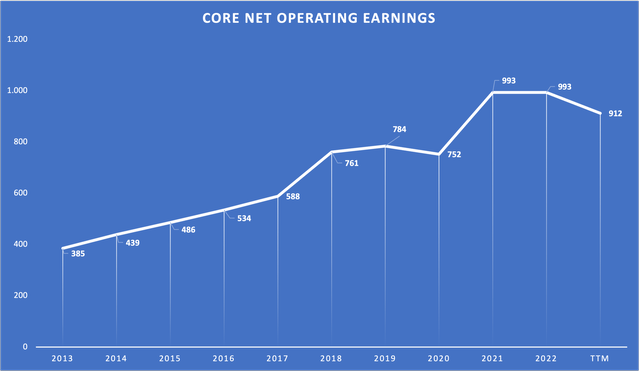

Here’s a chart exhibiting the event of core earnings during the last decade:

AFG Core Earnings since FY13 (Firm studies – compiled by Creator)

Creator’s Word: The Annuity enterprise which was offered in 2021 is included in core earnings till 2020.

We will see that core earnings are in a long-term upward development. This isn’t stunning since we already know that P&C premiums and the funding portfolio have been steadily rising. What we will see right here although is the impact that the event of the mixed ratio has on core earnings. Core earnings declined in FY20 according to the decline in premiums. This was to be anticipated. Core earnings have been flat YoY in FY22 and declined for the TTM regardless of premiums rising on this timeframe. That is because of the weak spot within the mixed ratio that I highlighted earlier.

Over the long term, core earnings grew with a CAGR of 11.10% since FY13 and 11.05% since FY17. Each progress charges are greater than the expansion charges we have now seen for insurance coverage premiums. That is attributable to enhancements within the mixed ratio. The mixed ratio improved from 94.1% in FY13 to 87.2% in FY22 and presently stands at 90.1% for the TTM. In conclusion, we will not count on that core earnings will develop sooner than premiums going ahead. My greatest guess is that core earnings will develop according to premiums at round 6%, perhaps a bit sooner if AFG manages to deliver the underwriting expense ratio down by reaching some working leverage (which I believe is fairly doubtless).

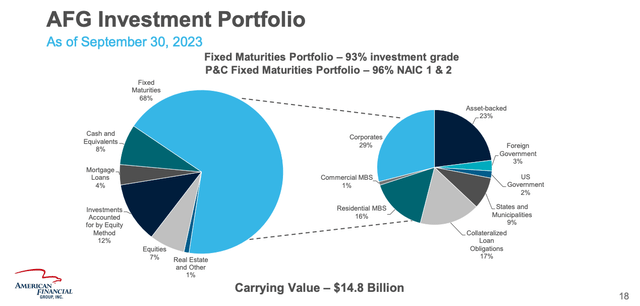

Subsequent, I would like to check out AFG’s funding portfolio:

AFG Funding Portfolio (BMO Capital Markets Digital Summit Presentation – Slide 18)

AFG’s portfolio is focused on Fastened maturities. $2,378 million are invested in Various Investments (primarily Investments Accounted for by the Fairness Technique and Equities). These are imagined to generate greater funding revenue whereas the Fastened maturities fulfill the necessity for liquidity.

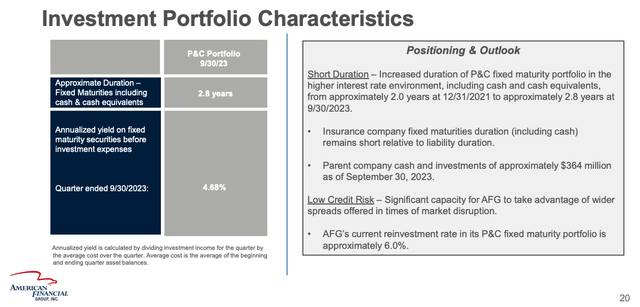

Right here is one other slide from the presentation exhibiting some extra Portfolio Traits:

Extra Portfolio Info (BMO Capital Markets Digital Summit Presentation – Slide 20)

Right here we will see one thing that I already guessed earlier. To catch the advantages of a rising yield atmosphere, AFG has prolonged the period of the mounted maturity portfolio from 2.0 years to 2.8 years because the finish of 2021. Moreover, with the annualized yield of the mounted maturities standing at 4.68% proper now and the reinvestment charges at 6%, we’d see some extra tailwinds from the yield facet over the close to time period. Because the older mounted maturities run out, they are often reinvested at greater charges, finally resulting in greater web funding revenue over the close to time period. As I stated earlier although, that is only a short-term impact of volatility and we should not pay an excessive amount of consideration to this.

General although, I like AFG’s strategy of investing a component (round 15%) of the portfolio into higher-yielding different investments, particularly as I’ve proven earlier that AFG’s float might be very long-term. With the portfolio’s carrying worth at $14.8 billion and near $10 billion in short-term mounted maturities, the liquidity facet of the portfolio covers 1.5x instances NEP, a wholesome ratio in my view.

Valuation

There are presently 84.7 million shares excellent whereas the worth per share stands at $118.96. So AFG’s market capitalization stands at near $10.1 billion proper now. With core earnings for the TTM coming in at $912 million, AFG presently trades at 11x core earnings which appears to be like low-cost.

Valuing an organization like AFG is not really easy although. There are 3 ways of valuing AFG in my view and I’ll undergo all of them.

(1) Return on Fairness (RoE) and Worth-to-E-book ratio (P/B)

This one is fairly easy and it is usually essentially the most inaccurate in my view. One might argue that Insurance coverage firms might be valued like banks. We’d like two values for this: E-book Worth (BV) and Return on Fairness (RoE). Within the case of AFG, we will simply take the adjusted BV that they report in each Investor Complement doc. On the finish of Q3 23, AFG’s adjusted BV stands at $4,536 million. If we divide the market capitalization by the BV, AFG trades at 2.2x BV. In the meantime, AFG generated $912 million in core earnings for the TTM, so the RoE for the TTM is available in at 20.1%.

Now we will put it collectively. If AFG generates 20% RoE and we count on a ten% return from our funding, we must be keen to pay 2x BV or round $107 per share. So this means that AFG is overvalued proper now.

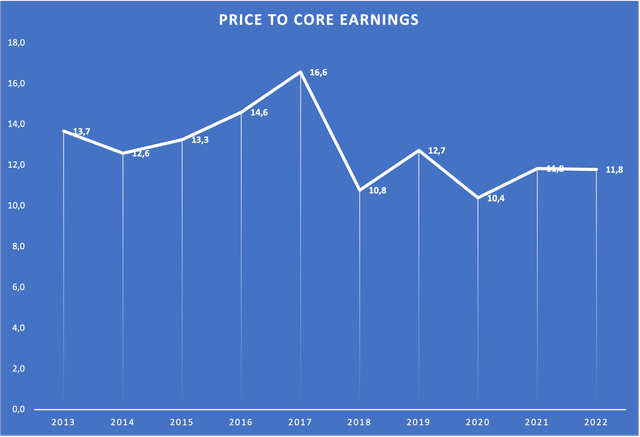

(2) Historic Worth to Core Earnings ratio

We will additionally take a look at how the market priced AFG prior to now. Here’s a chart exhibiting the Worth/Core Earnings ratio over the previous decade (the numbers are for the final day of December of yearly):

Worth/Core Earnings since FY13 (Compiled by Creator utilizing firm earnings and per share costs)

The typical is 12.8x Core Earnings and the median is 12.7x Core Earnings. If we apply 12.75x Core Earnings, AFG ought to commerce at $137 per share. Utilizing this valuation strategy, AFG appears to be like undervalued. I’ve to level out although that the above numbers additionally embrace the annuity enterprise till it was offered in 2021. Due to this, I believe that this additionally is not the very best strategy to worth AFG. This leads me to the final possibility.

(3) Discounted Money Stream Valuation

This might sound odd as a result of it is not frequent to worth an insurer utilizing a DCF strategy. Let me inform you why I believe that is the very best strategy.

Initially, we have to gauge long-term return potential. I at all times say that I believe long-term return potential is the sum of (1) the FCF Yield and (2) the longer term FCF progress fee. The issue is that within the case of AFG, we do not have an actual quantity for FCF as we do for “regular firms” due to the character of the insurance coverage enterprise. We will make it work although. So what does the FCF Yield usually inform us? It tells us how a lot money the corporate will pay out to us whereas nonetheless fulfilling reinvestment wants (CAPEX). Let’s apply this to AFG. I acknowledged a number of instances all through this text that I believe AFG ought to have the ability to develop premiums within the vary of 6% according to the previous since I see no purpose for the expansion fee to decelerate. The Funding Portfolio ought to develop according to premiums at 6%. This may imply that the legal responsibility facet of the steadiness sheet will develop at 6% as effectively. If AFG pays out all the pieces it earns, liabilities will outgrow the fairness half on the steadiness sheet, finally resulting in a weak steadiness sheet and AFG not with the ability to tackle new insurance coverage contracts. So if AFG needs to maintain this ratio up, it must develop fairness/ebook worth at 6% according to liabilities. If AFG manages to maintain producing RoE of 20%, it might want to reinvest 30% of core earnings again into the steadiness sheet. We will view this as some form of CAPEX for AFG as a result of it’s wanted to develop premiums.

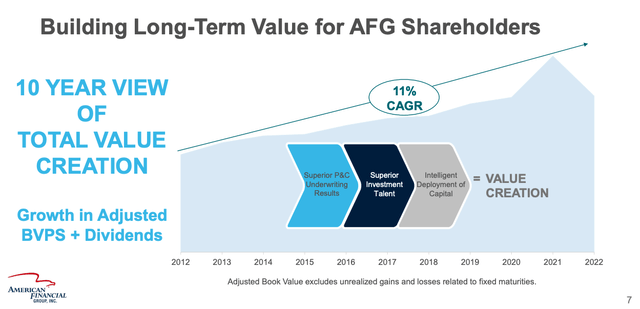

I’ve proven earlier that AFG presently trades at 11x core earnings which is equal to a 9% earnings yield. Now we deduct my “CAPEX” estimate of 30%. The result’s an “FCF Yield” of 6.3%. Now we’re again within the traditional valuation territory. If we add 6% premium progress on high of the 6.3%, AFG ought to have the ability to generate round 12% long-term returns going ahead. In case you assume this calculation was utterly delusional, let me present you a slide from the latest investor presentation:

10-12 months Worth Creation (BMO Capital Markets Digital Summit Presentation – Slide 7)

Right here we will see that AFG delivered progress in adjusted BV + Dividends of 11% since 2012, a bit beneath my expectations. If AFG could be valued at 12.75x core earnings because it did prior to now, my calculations would end in an 11% return potential sooner or later, according to the previous. In case you are a dividend investor, be told that the 6.3% “FCF Yield” I discussed will most likely be near 100% dividends. So AFG is a high-yield inventory with mid-single-digit progress, making it an fascinating selection for dividend buyers who wish to diversify their portfolio with out compromising on whole return prospects.

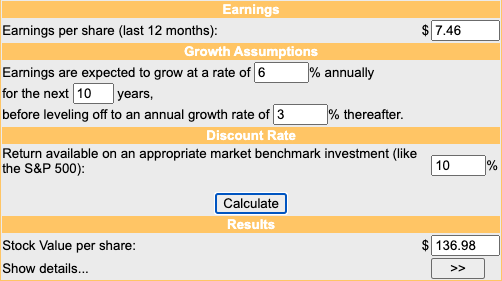

Now to complete this part up, let’s carry out a DCF calculation. I’ll assume $10.65 core earnings per share (as AFG guides for FY23). After deducting the 30% “CAPEX” talked about above, the beginning FCF must be $7.46 per share. I’ll use a ten% low cost fee (as I at all times do), 6% progress over the following decade and three% progress into perpetuity (a bit above world GDP progress). Right here is the end result:

DCF Calculation (Moneychimp.com)

Surprisingly, my estimates depart me to imagine that AFG must be price $137 per share. That is precisely the identical worth that I derived utilizing the Worth/Core Earnings ratio, indicating that the market priced AFG pretty fairly over the previous decade.

In conclusion, I believe that AFG is undervalued for the time being with an upside potential of round 15%.

Dangers

After fascinated by it for fairly a while, dangers appear to be low. The one two dangers I see are (a) a everlasting decline within the mixed ratio and (b) a everlasting decline within the portfolio yield.

Threat (a) would imply that AFG instantly begins to lose its underwriting prowess or experiences deterioration of underwriting prices. This may result in decrease underwriting revenue or within the worst case even to underwriting losses. Since underwriting accounts for an enormous a part of AFG’s income, this could be very dangerous for the corporate and subsequently additionally for the share value.

Threat (b) is much extra doubtless and would come into play if the federal funds fee goes again to zero. This may result in a pointy decline in AFG’s web funding revenue which may’t be made up for by the expansion of the portfolio measurement. If you wish to guess on declining charges, AFG just isn’t the fitting funding to take action.

Conclusion

AFG has been in a position to develop web earned premiums (NEP) at above 6% per yr over the previous decade and there’s no purpose to count on this progress fee to materially decline. The funding portfolio generated web funding revenue and grew according to NEP (even a bit sooner) whereas the portfolio yield adopted the federal funds fee. AFG’s steadiness sheet and funding portfolio look wholesome. Web debt stands at 0.5x core earnings, an excellent ratio.

The insurance coverage enterprise is defensive by nature and AFG operates in a number of area of interest markets whereas being effectively diversified all through the sub-sectors of its three major reporting segments.

I estimate that AFG could possibly pay out on the “FCF Yield” of 6.3% whereas rising earnings according to premiums at round 6% going ahead. Utilizing a number of valuation approaches, I concluded that AFG is undervalued and must be price round $137 per share.

Dangers appear low and the one two dangers I see are completely declining margins (expressed by a deteriorating mixed ratio) and a everlasting decline within the portfolio yield within the case of a return to the zero-rate coverage.

Taking all the pieces into consideration, I provoke protection on AFG with a purchase score and a good worth estimate of $137 per share.

{kind=link}