ProjectB

Funding Thesis: I take the view that Danone S.A. (OTCQX:DANOY) might see upside if the corporate meets its like-for-like gross sales goal of 6-7% going ahead and ship additional quantity progress. Till such time, I proceed to charge the corporate as a maintain.

In a earlier article again in October, I made the argument that Danone S.A. is unlikely to see upside till such time that we see a big revival in volume-based progress.

Nonetheless, the inventory has since ascended to a value of $12.95 on the time of writing:

TradingView.com

The aim of this text is to evaluate the important thing drivers of progress in Danone S.A., and whether or not the inventory has the capability to see continued progress from right here taking current efficiency into consideration.

Efficiency

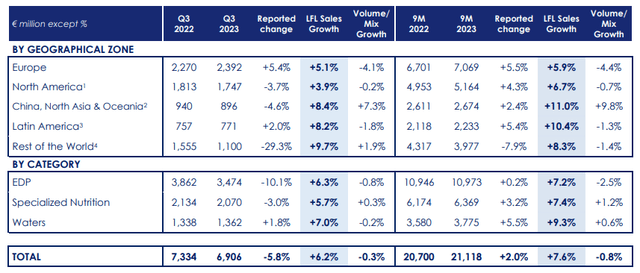

When third quarter 2023 outcomes for Danone S.A. (as launched on October 26, 2023), we can see that Europe continued to see respectable progress in like-for-like gross sales of 5.1% as in comparison with the prior yr quarter, however quantity was down by 4.1% over the identical interval.

Danone: 2023 Third-Quarter Gross sales

The China, North Asia, and Oceania area noticed the very best proportion progress in gross sales of 8.4%, and quantity was up by 7.3% over the identical interval.

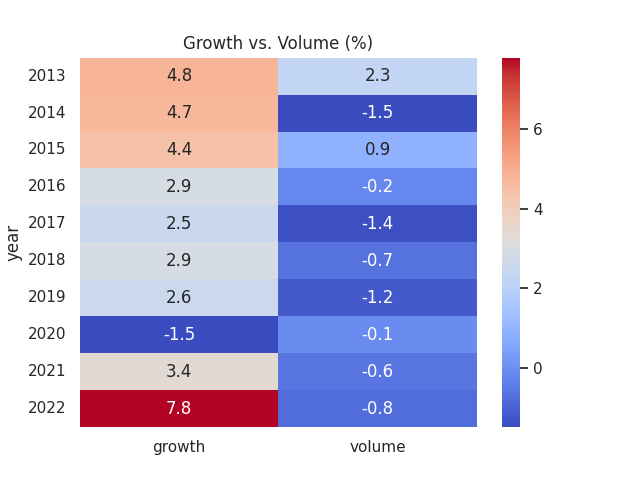

When full-year outcomes, we are able to see that whereas progress in the latest yr got here in at a 10-year excessive – quantity had nonetheless seen a decline indicating that progress was price-driven versus volume-driven.

Figures sourced from historic Danone full-year reviews. Heatmap generated by creator utilizing Python’s seaborn visualisation library.

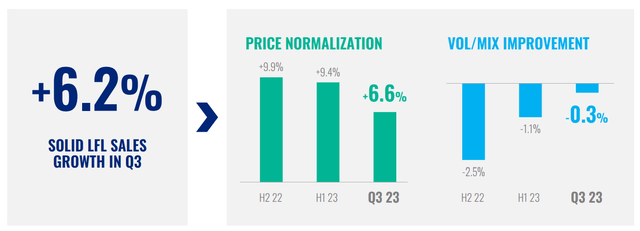

With this being mentioned, now we have seen value progress begin to normalise and quantity progress begin to rebound – although the latter has remained barely detrimental for this quarter:

Danone Q3 2023 Gross sales Presentation

On this regard, I take the view that if Danone can proceed to point out proof of a rebound in quantity heading into This fall, then this might permit for additional upside within the inventory.

My Perspective and Trying Ahead

As regards my tackle the above outcomes and the implications for the expansion trajectory of the inventory going ahead, I take the view that indicators of value normalisation and a sluggish however regular restoration in quantity are encouraging.

Whereas quantity progress throughout China, North Asia & Oceania was vibrant at 7.3%, this market accounted for simply over 12% of total gross sales whereas that of Europe accounted for practically 35% in Q3 2023.

On this regard, a rebound in quantity progress throughout the European market can be significantly necessary to maintain a rebound in quantity demand total. I had beforehand said that with pressures on value progress and authorities initiatives throughout the French market to implement value reductions for main grocery store retailers – there was the danger that quantity might not rebound and total gross sales progress would see a substantial drop.

Nonetheless, quantity has seen an enchancment along with value normalization, and a continuation of this development could be encouraging. Taking efficiency throughout the French market into consideration – which is a extremely necessary market within the context of Europe – efficiency was extra spectacular than anticipated and the corporate is now anticipating like-for-like gross sales progress of 6-7% as in comparison with a previous expectation of 4-6%. Progress throughout Europe was significantly led by initiatives such because the transformation of each the Important Dairy and Plant-based merchandise companies.

From this standpoint, I can be retaining an in depth eye on full-year outcomes to find out whether or not 1) quantity progress can rebound into constructive territory given the anticipated additional normalization of value, and a couple of) like-for-like gross sales progress can meet the 6-7% goal as set out by Danone.

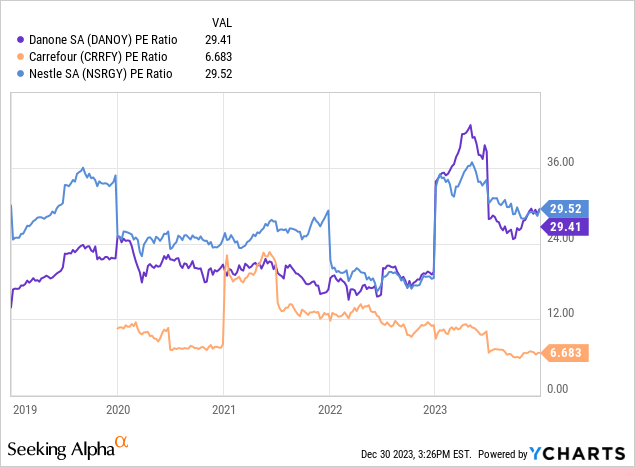

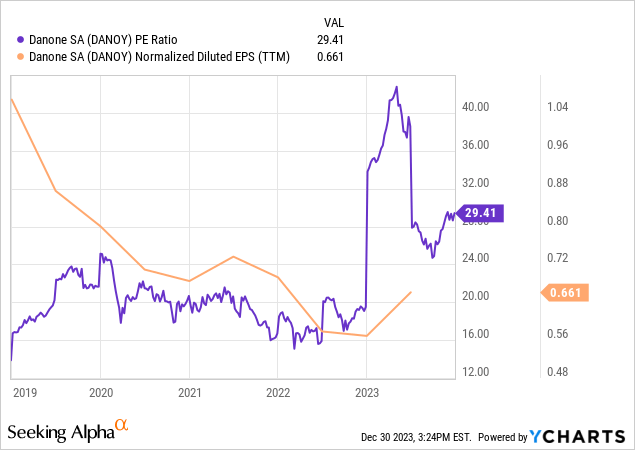

When wanting on the 5-year P/E ratio trajectory for Danone, we are able to see that each Danone and competitor Nestle (OTCPK:NSRGY) are buying and selling above 29x, whereas that of Carrefour (OTCPK:CRRFY) is considerably decrease at 6.683x.

YCharts

Moreover, we are able to see that whereas earnings have began to rebound – the P/E ratio remains to be buying and selling considerably increased than in earlier years.

YCharts

From this standpoint, I take the view that Danone S.A. is pretty valued at this cut-off date – with additional progress being potential if we see indicators of a rebound in quantity demand throughout the following quarter in addition to proof that Danone can meet its like-for-like gross sales goal of 6-7% for the yr.

Dangers

By way of the potential dangers to Danone S.A. at the moment, whereas it’s encouraging that the corporate has seen progress in quantity and like-for-like gross sales – it’s nonetheless potential that Danone might come below better stress to decrease costs as in comparison with its friends going ahead.

As an example, a considerably better portion of Danone’s merchandise akin to yogurt are commodities with a number of personal label alternate options out there, whereas Nestle affords a considerably wider array of branded merchandise throughout a number of classes that customers could also be extra reluctant to change from – thus permitting for a sure diploma of energy for the corporate with regards to price-setting.

On this regard, value normalisation stays a menace – and the danger stays that like-for-like gross sales might nonetheless are available in decrease than anticipated if we see value drops outweigh the consequences of quantity progress.

Conclusion

To conclude, Danone S.A. has seen encouraging progress in like-for-like gross sales with a sluggish but regular rebound in quantity.

On this regard, I take the view that the upcoming quarter will show a big telling level as as to if Danone has the capability to see upside from right here. Specifically, I can be in search of proof that the corporate can meet its like-for-like gross sales goal of 6-7% in addition to proof that quantity progress can outweigh any additional downward stress on value.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}