csfotoimages/iStock Editorial through Getty Pictures

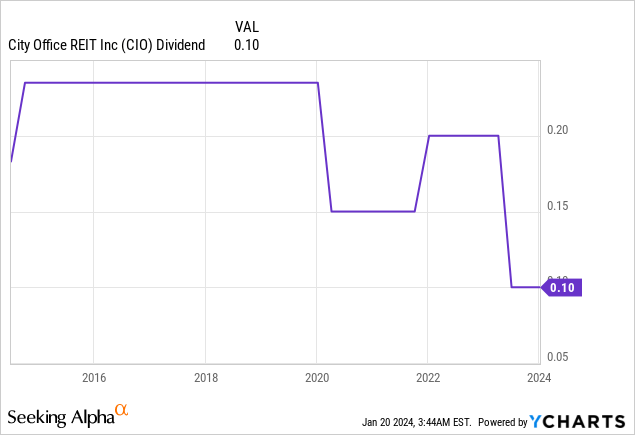

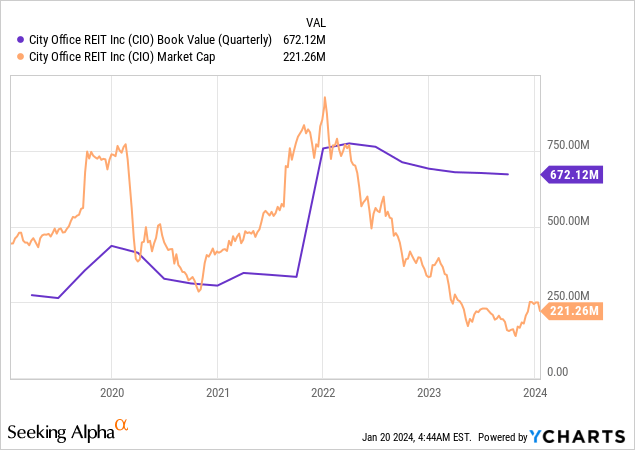

The sustained collapse of fairness workplace REITs since 2022 has doubtless opened up some alternatives to accumulate extremely distressed belongings with first rate underlying fundamentals regardless of the grim backdrop posed by the tripartite of excessive rates of interest, work-from-home developments, and the specter of a recession. Metropolis Workplace REIT (NYSE:CIO) is down roughly 70% over this time-frame, now buying and selling arms at a 67% low cost to a ebook worth of $16.83 per share on the finish of its final reported fiscal 2023 third quarter. The internally managed REIT final declared a quarterly money dividend of $0.10 per share, left unchanged sequentially and $0.40 per share annualized, for a 7.3% ahead dividend yield.

Nonetheless, ebook worth is a considerably contentious metric for workplace REITs because it doesn’t seize the deterioration in underlying property fundamentals throughout the US. The nationwide workplace emptiness charge reached 18.1% in November 2023, up 190 foundation factors over its year-ago comp, with the most important will increase seen in West Coast markets, with San Francisco significantly hit exhausting.

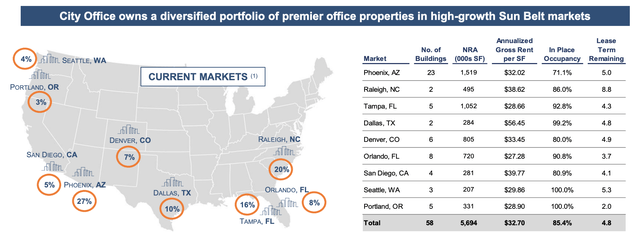

Metropolis Workplace REIT November 2023 Presentation

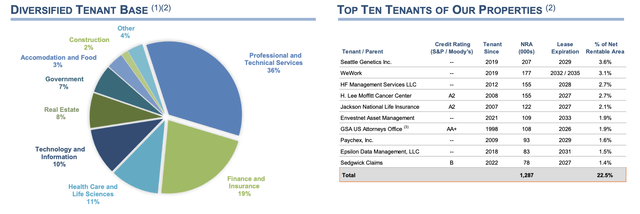

CIO is very diversified throughout the US, specializing in the Solar Belt markets, with Florida and Arizona forming its largest markets. The REIT owns or has a controlling curiosity in 58 properties unfold throughout 5.7 million sq. toes of workplace properties in 10 cities on the finish of its third quarter. These had an mixture 85.4% occupancy charge with 4.8 years remaining on common on their leases. The query now could be simply how a lot of a worth play CIO is with ebook worth doubtless not a full reflection of the particular market worth of its properties.

Income, FFO, And Dividend Protection

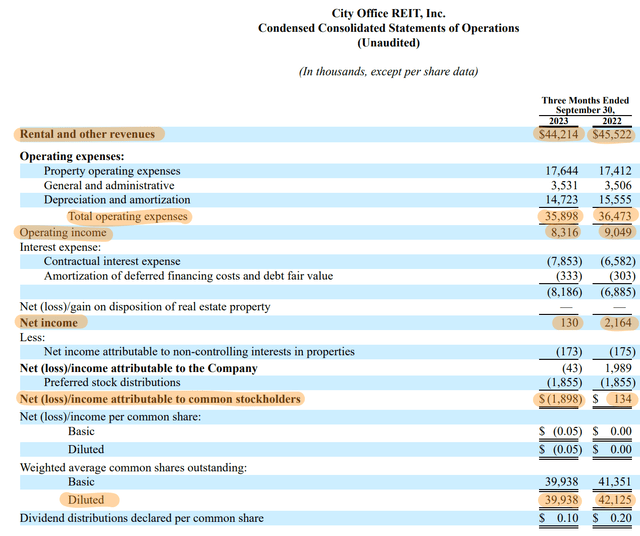

CIO generated income of $44.2 million throughout its third quarter, a 2.9% decline over its year-ago comp however a beat of $230,000 on consensus estimates. The dip in income was led by occupancy, which fell by 40 foundation factors regardless of same-store money internet working earnings rising by 2.2% versus its year-ago quarter. Nonetheless, working earnings at $8.3 million dipped from $9 million within the year-ago interval, with internet earnings attributable to widespread shareholders a lack of $1.9 million.

Metropolis Workplace REIT Fiscal 2023 Third Quarter Kind 10-Q

Core FFO for the third quarter got here in at $13.7 million, round $0.34 per share, and down 5 cents from core FFO of $0.39 within the year-ago interval. The extra related determine for the dividend is adjusted FFO, which got here in at $6.3 million throughout the quarter. This was $0.15 per share, dipping by 3 cents from the year-ago interval. This meant 150% protection for the dividend or a 67% payout ratio.

Metropolis Workplace REIT November 2023 Presentation

The REIT’s 3.1% publicity to bankrupt co-working house supplier WeWork (OTC:WEWKQ) is a legal responsibility, with ongoing restructuring efforts doubtless set to ship decrease rents or a interval of elevated emptiness as CIO makes an attempt to lease the house to a brand new supplier. CIO’s weighted common widespread shares excellent was additionally down 5.2% year-over-year attributable to an ongoing $50 million share buyback program licensed in Could 2023.

Leverage, Maturities, And The Fed

Metropolis Workplace REIT November 2023 Presentation

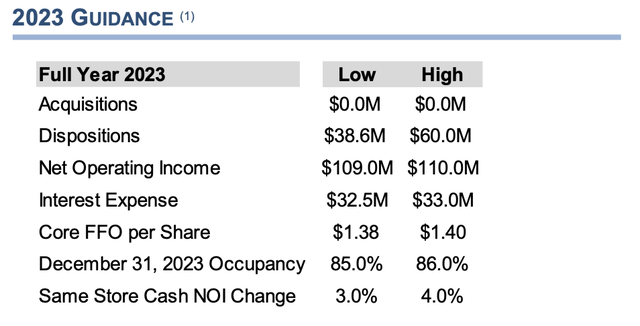

CIO is guiding for core FFO to be $1.38 per share at minimal for its full 12 months 2023, which implies it’s at present swapping arms for 4x instances core FFO. I might anticipate AFFO to be decrease at round $0.60 per share, which implies the next however nonetheless very constrained 9.2x a number of.

Metropolis Workplace REIT November 2023 Presentation

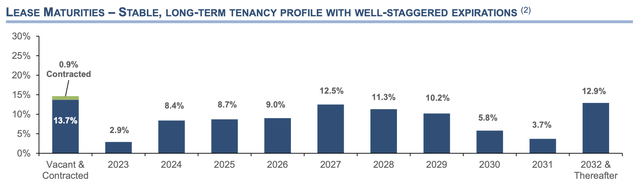

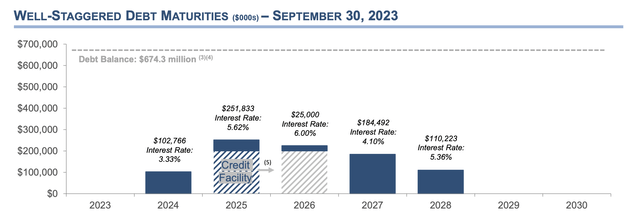

I just like the REIT’s well-laddered lease expirations, with simply 16.8% of leases expiring by 2025. This offers CIO extra time to have the ability to execute new leases towards workplace property markets that may nonetheless in restoration. CIO executed 119,000 sq. toes of latest and renewable leases throughout the third quarter, with renewal money rents that have been 3.1% greater versus expiring rents. Nonetheless, debt maturities are fairly front-loaded, with $102.8 million coming due in 2024 and one other $251.8 million coming due in 2025. That is towards money and equivalents of $36.7 million on the finish of the third quarter.

Metropolis Workplace REIT November 2023 Presentation

Therefore, additional asset disposals will doubtless be essential regardless of the $330 million of utterly unencumbered properties that CIO can connect mortgage debt to. I’ve not been shopping for any widespread shares of purely office-focused fairness REITs because the trade continues to be going by means of a reset to a brand new regular. Nonetheless, I have been shopping for related distressed preferreds or bonds. CIO’s 6.625% Sequence A Preferreds (NYSE:CIO.PR.A) at present supply a 9% yield on price and are buying and selling round $6.68 beneath their $25 per share liquidation worth. The Fed will probably be instrumental to worth creation for each securities this 12 months, as practically 150 foundation factors value of cuts by means of 2024 stays the bottom case based on the CME FedWatch Instrument. Each of those securities are rated as a maintain.

{kind=link}