Natali_Mis

We beforehand lined Affirm (NASDAQ:NASDAQ:AFRM) in January 2024, downgrading the inventory to a Maintain, as a result of overly optimistic rally by +175.9% because the October 2023 backside.

Whereas the fintech continued to exhibit worthwhile progress, we didn’t imagine that the inventory’s eye-watering premium was sustainable then. Mixed with the elevated quick curiosity, we believed that there could be a deep pullback within the near-term.

For now, with AFRM already pulling again by -19.7% because the earlier article, we imagine that there’s an improved margin of security right here, primarily based on the fintech’s enhancing margins and the administration’s promising FY2024 steerage.

Mixed with the inventory’s constantly moderating FWD valuations, we imagine that the fintech is slowly rising into its progress premium, with FY2025/ FY2025 prone to exhibit its proof of idea as a prudent and profitable BNPL fintech platform.

The AFRM Funding Thesis Is Extra Engaging After The Latest Pullback

AFRM has executed extraordinarily nicely regardless of the unsure macroeconomic outlook, attributed to the constant progress in its annualized Gross Merchandise Quantity to $30B (+33.9% QoQ/ +31.5% YoY) and its energetic customers to 17.1M (+0.2M QoQ/ +2.4M YoY) by FQ2’24.

Most significantly, due to the administration’s constant price optimizations, the fintech continues to develop its adj working profitability to $93M (+55% QoQ/ +250% YoY) with adj margins of 16% (+4 factors QoQ/ +32 YoY).

On the one hand, the Client Monetary Safety Bureau stories that BNPL customers usually report a median credit score rating within the sub-prime class of between 580 and 669, in contrast the non-users with constantly increased credit score scores of close to prime at between 670 and 739.

That is additionally partly why AFRM has been established, “as a result of bank cards aren’t working,” with the fintech additionally choosing its personal proprietary ITACs credit score high quality rating to “analyze the traits of a shopper’s attributes predictive of each willingness and talent to repay loans.”

Alternatively, whereas we’ve been skeptical ourselves, it’s obvious that the AFRM administration has been comparatively profitable in managing its shopper and portfolio dangers.

That is attributed to the fintech’s comparatively cheap 30+ days delinquency price of two.4% (inline QoQ/ YoY), 60+ days of 1.4% (inline QoQ/ -0.1 factors YoY), and 90+ days of 0.7% (inline QoQ/ YoY) by FQ2’24, whereas under FY2019 averages.

That is in comparison with its different fintech friends:

SoFi (SOFI), with 30+ days delinquency price of 0.9% and total delinquency price at 2.5% as of FY2023. PayPal (PYPL) with 30+ days delinquency price of 1.4%, 60+ days of 1%, and 90+ days of two.2%, and different main bank card lenders at a median of three.2% as of February 2024.

As well as, whereas AFRM’s internet charge-off has been rising to $151.31M (+131.7% QoQ/ +9.4% YoY), we’re not overly involved, because the identical has been reported by a number of fintech and standard banks because the macroeconomic outlook normalizes from the hyper-pandemic interval.

These developments are proof that the administration’s prudence in moderating the mortgage origination quantity has labored as meant in reducing its mortgage portfolio credit score dangers.

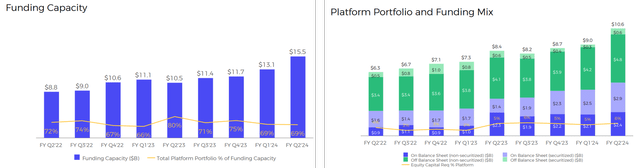

AFRM’s Funding Capability & Loans Held On Stability Sheet

In search of Alpha

The identical has been noticed in AFRM’s means to increase its exterior funding to $15.5B (+18.3% QoQ/ +47.6% YoY) by the newest quarter, demonstrating the fintech’s means to sustainably develop its mortgage portfolio with out having to overly depend on its stability sheet.

Lastly, the administration has additionally provided a promising FY2024 outlook, with GMV of over $25.25B (+25% YoY) and adj working margins of over 11% (+15.6 factors YoY), implying its improved monetization and working scale transferring ahead.

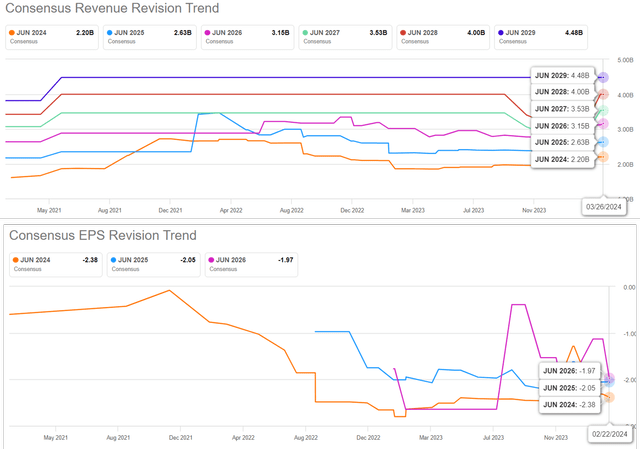

The Consensus Ahead Estimates

In search of Alpha

Maybe for this reason the market stays largely optimistic about AFRM’s prospects, attributed to the comparatively secure prime line progress estimate at a CAGR of +25.7% via FY2026, with constructive Free Money Stream technology from FY2024 onwards.

So, Is AFRM Inventory A Purchase, Promote, or Maintain?

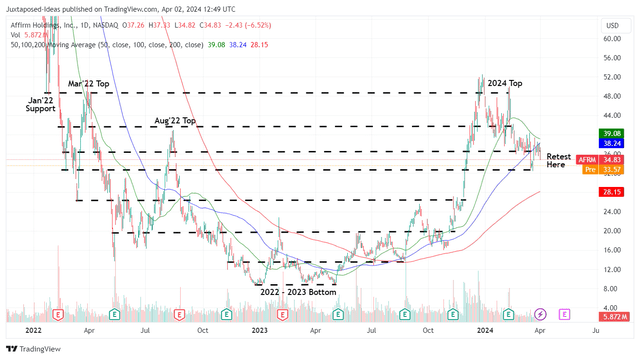

AFRM 2Y Inventory Value

Buying and selling View

For now, AFRM has dramatically retraced by -31.9% because the 2024 peak, with the inventory now showing to retest the earlier assist ranges of $30s.

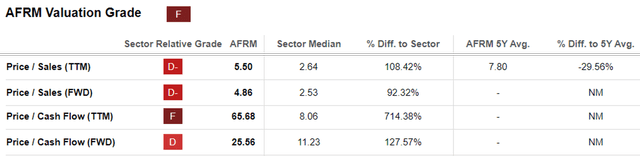

AFRM Valuations

In search of Alpha

Primarily based on the inventory’s lack of ability to maintain the upward momentum and the moderation noticed in AFRM’s valuations to FWD Value/ Gross sales of 4.86x and FWD Value/ Money Stream of 25.56x, in comparison with the earlier article of seven.32x/ 49.14x and the 3Y Value/ Gross sales imply of 10.98x, it’s obvious that the market is ready for the fintech to develop into its premium valuations

The identical has been noticed in its fintech friends, together with SOFI at FWD Value/ Gross sales of three.16x and UPST at 3.93x, in comparison with their 3Y imply of 5.38x and eight.05x, respectively.

A lot of AFRM’s headwind might be attributed to the unsure macroeconomic outlook and the unlikely GAAP profitability within the near-term.

On the identical time, with the Fed already pricing in three price cuts in 2024, we might even see additional strain within the fintech’s revenue unfold, albeit probably well-balanced by the rising mortgage origination as borrowing prices average, additional aided by the sturdy labor market.

Because of the AFRM’s nascent BNPL platform and the unsure gentle touchdown, we will perceive why the inventory has pulled again because it has because the hyper-pandemic peak and the 2024 prime.

Nonetheless, right here is the place we imagine there’s immense alternatives for buyers with increased danger tolerance, because the inventory seems to be nicely supported at present ranges, providing buyers with an improved margin of security.

On the identical time, we imagine that the headwinds could elevate over the following few quarters, as AFRM ship the primary yr of adj working revenue, additional cementing its reversal over the following few years because the macro outlook normalizes.

Consequently, we’re upgrading AFRM as a Purchase for buyers with a long-term investing trajectory, particularly made enticing by the latest pullback.