PM Photos

Introduction

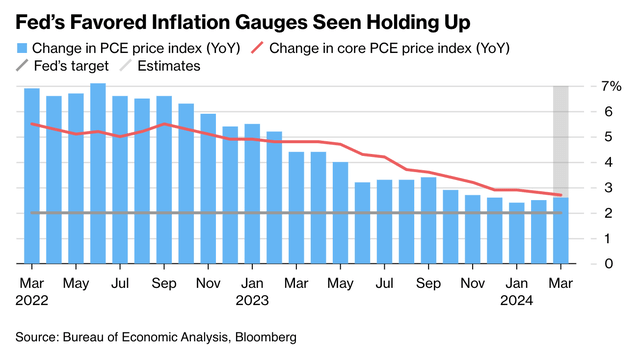

Inflation has turn out to be a problem once more. In the US, all-item inflation has are available larger than anticipated for 4 consecutive months, with new upside momentum reported in March.

Expectations are the Fed’s favourite indicator – the PCE value index – will present its third-consecutive enhance in March as properly.

Bloomberg

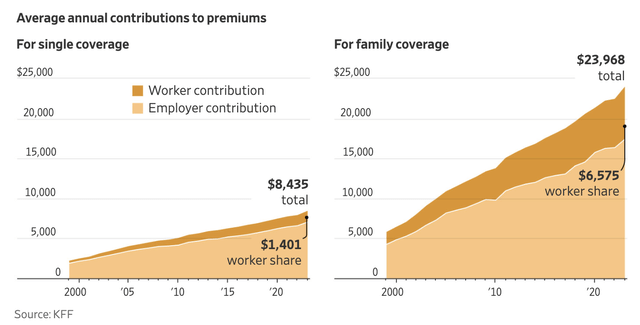

Zooming a bit out, one of many greatest points for buyers and customers is healthcare inflation. My very own healthcare insurance coverage premiums, for instance, went up by double-digits this yr.

The most important difficulty for insurers and the complete healthcare business is rising prices. As reported by The Wall Road Journal final yr, “A household’s medical insurance prices practically $24,000 this yr after the most important enhance in additional than a decade.”

Wall Road Journal

The explanation I am bringing this up is as a result of I am an enormous fan of healthcare corporations with pricing energy.

Not solely can these corporations assist us to guard our wealth towards what might be a chronic interval of elevated healthcare inflation as a result of normal inflation points and secular drivers like an ageing inhabitants, but in addition to achieve our retirement objectives.

That is the place Abbott Laboratories (NYSE:ABT) is available in.

On April 20, I wrote an article titled “20 Years to $300K? Constructing A $10,000 Dividend Portfolio From Scratch.”

Abbott was one of many holdings I offered in that article, because it has a robust healthcare enterprise portfolio, a 2.1% dividend yield, a 12.1% 5-year dividend CAGR, a sub-50% payout ratio, and greater than 50 consecutive annual dividend hikes, making it one of many few Dividend Kings in the marketplace.

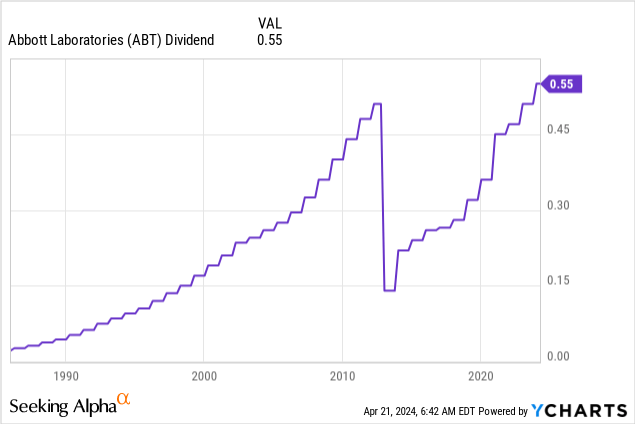

Be aware that the massive decline within the dividend chart beneath is brought on by the AbbVie (ABBV) spin-off. ABT didn’t reduce its dividend. For the reason that spin-off, ABBV has hiked its dividend each single yr as properly.

My most up-to-date article on this inventory was written on January 29, after I went with the title “The King Is Again: Abbott Laboratories’ Path To >11% Annual Returns.”

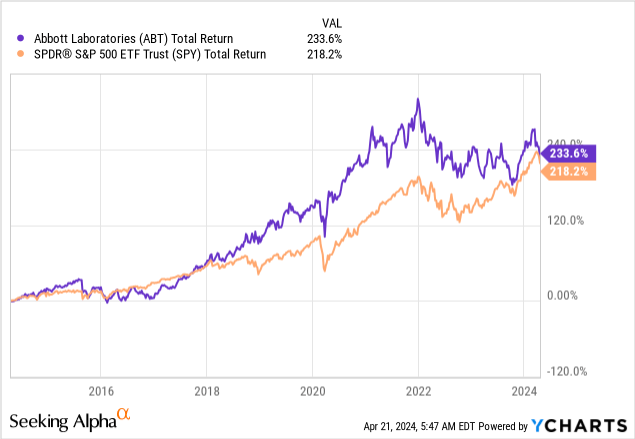

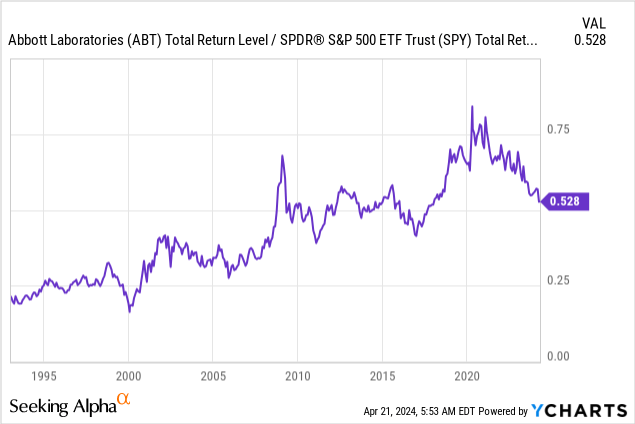

Since then, ABT is down 5%, together with dividends, lagging the S&P 500 by roughly 580 foundation factors.

The excellent news is that over the previous ten years, ABT was nonetheless the higher funding in comparison with the S&P 500.

On this article, I am going to re-assess the danger/reward and clarify why ABT stays certainly one of my all-time favourite dividend development shares that gives each security and earnings development.

Even higher, as the corporate simply launched its 1Q24 earnings, we have now a whole lot of new knowledge to work with.

So, let’s get to it!

Put up-COVID, Abbott Stays Rock-Stable

Abbott is among the healthcare corporations that benefitted tremendously from the pandemic. In spite of everything, testing (amongst different merchandise) demand exploded when the world was making an attempt to determine learn how to take care of the brand new virus.

After the pandemic, demand for these merchandise quickly declined, which resulted in a considerably difficult scenario the place a whole lot of sturdy healthcare corporations abruptly reported horrible development charges, and buyers had been coping with difficult valuation assessments.

The chart beneath compares the ratio between ABT’s complete return and the full return of the S&P 500. Whereas ABT has constantly outperformed the market, it has been an underperformer because the second the world observed that COVID-19 was, in truth, not the tip of the world.

Whereas this can be unhealthy information for buyers who hoped to make a fast buck with Abbott, I imagine this brings new alternatives, because the Abbott core enterprise stays in improbable form.

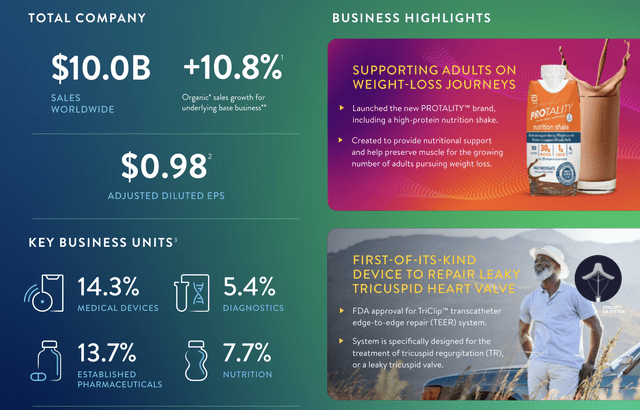

Within the just-released 1Q24 quarter, the corporate reported adjusted earnings per share of $0.98, which exceeded analyst consensus estimates by two pennies. Natural gross sales of its non-COVID enterprise rose by 10.8%.

Abbott Laboratories

Even higher, as we’ll talk about later on this article, the sturdy efficiency resulted in an upward revision of the midpoint for each earnings per share and gross sales development steering ranges.

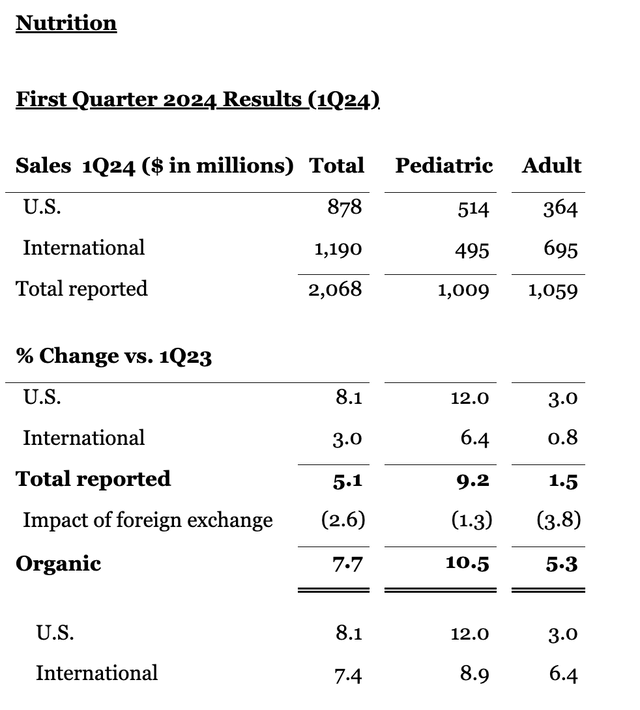

Digging a bit deeper, we discover that within the Diet phase, gross sales elevated by 8% on an natural foundation.

Abbott Laboratories

This development was primarily pushed by sturdy efficiency in Pediatric Diet, which was fueled by ongoing market share positive aspects within the U.S. toddler formulation enterprise in addition to the corporate’s enlargement of the worldwide portfolio of toddler formulation, toddler, and grownup diet manufacturers.

Abbott Laboratories

Furthermore, the launch of Protality, which is a brand new diet shake designed to assist adults in weight reduction whereas preserving lean muscle mass, added considerably to development.

Apparently sufficient, this product comes at a good time when weight-loss drugs like GLP-1 have became development engines.

Even higher than the 8% development in Diet is the 14% natural development price within the Established Prescribed drugs Division (“EPD”).

In keeping with Abbott, this division not solely achieved spectacular positive aspects in top-line development but in addition confirmed vital enchancment in working margin, with over 350 foundation factors of enchancment in comparison with 2019.

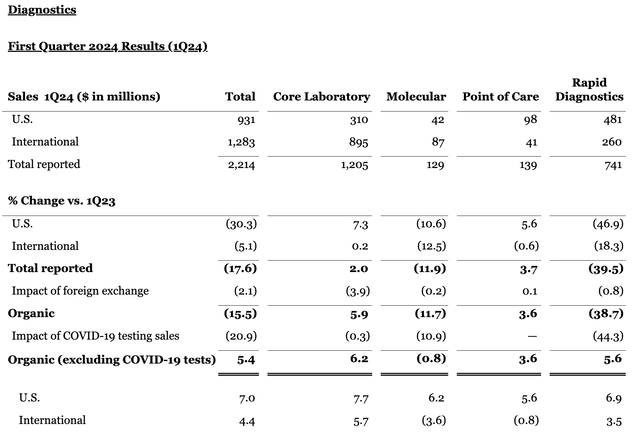

The Diagnostics phase noticed 5% gross sales development, which excluded COVID-19 testing. Together with the 20.9% decline in COVID-related gross sales, natural development would have been down 15.5%.

Abbott Laboratories

COVID-adjusted natural development was supported by the adoption of the corporate’s “market-leading” methods and elevated demand for testing from a variety of shoppers, together with hospitals, laboratories, pressing care facilities, doctor workplaces, retail pharmacies, and blood screening services.

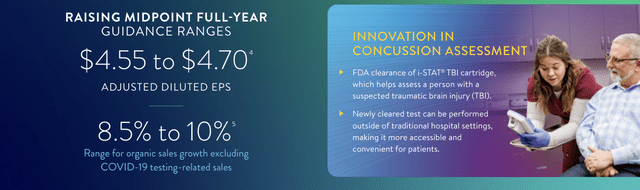

Moreover, in line with the corporate, a point-of-care diagnostic check for delicate traumatic mind damage or concussion acquired FDA approval throughout the quarter.

This might doubtlessly rework concussion testing requirements.

The entire blood check on a conveyable instrument helps clinicians consider sufferers 18 years of age and older who current with suspected delicate traumatic mind damage or mTBI, generally generally known as concussion. Take a look at outcomes will help rule out the necessity for a CT scan of the top and help in figuring out one of the best subsequent steps for affected person care. – Through PR Newswire

Final however not least, the Medical Gadgets phase noticed an enormous 14% enhance in natural gross sales throughout the first quarter.

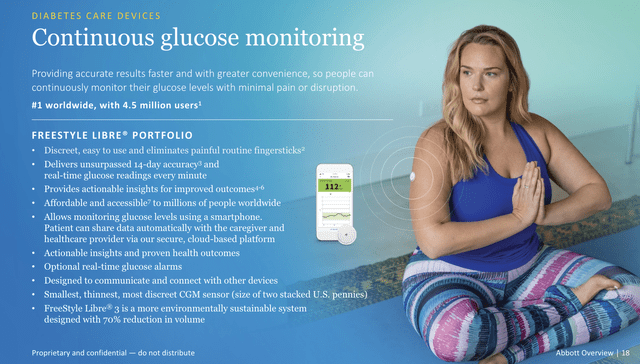

Inside Diabetes Care, FreeStyle Libre gross sales rose to $1.5 billion. That is a 23% development price in certainly one of my favourite healthcare niches. In actual fact, the corporate’s glucose monitor has turn out to be the best-selling product in its market.

Abbott Laboratories

Basically, apart from concussion testing and glucose breakthroughs, the corporate additionally launched merchandise like TriClip for coronary heart valve restore and the Aveir leadless pacemaker.

In Rhythm Administration, development of seven.5% was led by Aveir, our just lately launched leadless pacemaker. Aveir has quickly captured market share within the single-chamber pacing phase of the market and is now getting used for dual-chamber pacing, which is the most important phase of the pacing market. This revolutionary expertise helps to ship development charges in our Rhythm Administration enterprise that considerably exceed the general development on this market. – ABT 1Q24 Earnings Name

A Rosy Outlook & Good Information For Shareholders

As I already briefly talked about, sturdy core gross sales and earnings led to a steering hike.

It now expects adjusted earnings per share to be within the vary of $4.55 to $4.70.

Moreover, natural gross sales development, excluding COVID-19 testing-related gross sales, is projected to be between 8.5% to 10%.

Abbott Laboratories

The “drawback” with this EPS steering was that analysts had been disenchanted that the corporate didn’t elevate the ceiling of the steering vary.

The ceiling positively stays the identical, and that is the entire level. The inventory goes to go up when you beat expectations,” mentioned RBC Capital Markets analyst Shagun Singh.

In the event you’re sustaining expectations, it is already priced into the inventory… So that is what’s taking part in proper now,” she mentioned, including that she stays optimistic on Abbott. – Through Reuters

So, what does all of this imply for buyers?

I get that Abbott is in a considerably powerful spot, because it’s exhausting to place a price on a inventory with extreme COVID-19 headwinds.

Nonetheless, I actually like the corporate’s long-term development potential and its concentrate on shareholders by constant dividend development.

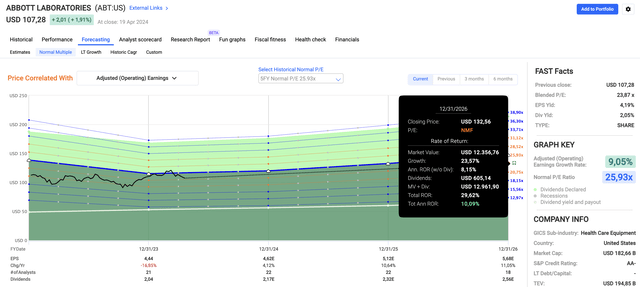

Presently, ABT trades at a blended P/E ratio of 23.9x, which is above its 20-year common of 19.8x.

That mentioned, as I wrote in my final article, I imagine the five-year normalized P/E ratio of 25.9x is a fairer metric, as the corporate is in a scenario the place non permanent post-pandemic headwinds cloud the image.

FAST Graphs

The excellent news is that regardless of these headwinds, analysts count on 4% EPS development this yr, doubtlessly adopted by 11% development in each 2024 and 2025.

If we apply a 23.3x a number of (beneath the five-year common), we get a possible complete return of 10%, together with the corporate’s 2.1% dividend. A quantity larger than that isn’t unlikely, in my view.

Whereas ABT could also be in tough waters, I imagine it’s a improbable dividend development inventory with a excessive probability of long-term outperformance.

Therefore, I am at present determining learn how to match ABT into my portfolio, as I am trying so as to add a couple of corporations to my 20-stock portfolio.

Takeaway

Investing in Abbott Laboratories presents a chance for long-term development and stability in mild of inflation considerations.

Regardless of latest challenges, ABT’s core enterprise stays strong, with spectacular efficiency throughout its segments, together with Diet and Medical Gadgets.

In the meantime, the corporate’s concentrate on innovation, supported by merchandise like Protality and FreeStyle Libre, positions it for continued success.

Whereas short-term headwinds might have an effect on its valuation, ABT’s constant dividend development and potential for future earnings development make it a gorgeous funding.

With analysts forecasting optimistic EPS development and a possible complete return of 10%, ABT stays a compelling alternative for buyers looking for each earnings and development in unsure instances.

Execs & Cons

Execs:

Stability Amidst Inflation: ABT provides stability throughout inflationary durations, with a various portfolio that features important healthcare merchandise and pricing energy. Robust Core Enterprise: Regardless of latest challenges, ABT’s core enterprise stays sturdy, confirmed by its spectacular efficiency in segments like Diet and Medical Gadgets. Innovation: The corporate’s dedication to innovation, with merchandise like Protality and FreeStyle Libre, positions it for long-term development and market management. Constant Dividend Development: ABT’s monitor report of constant dividend development makes it a gorgeous choice for income-focused buyers.

Cons:

Valuation Challenges: Quick-term valuation could also be affected by post-pandemic headwinds, doubtlessly impacting short-term returns. Uncertainty: Associated to the purpose above, the continued impression of COVID-19 on healthcare demand creates some uncertainty relating to future earnings and development prospects. Competitors: Whereas ABT has confirmed to stay sturdy in mild of competitors, it operates in engaging markets with keen friends.

{kind=link}