We Are/DigitalVision through Getty Pictures

Funding abstract

My advice for ManpowerGroup (NYSE:MAN) is a promote score. I’m not assured of a restoration within the coming months, given the unsure macro-conditions. Companies are unlikely to restart their hiring momentum given the unsure outlook. As MAN’s income continues to say no, fastened prices are going to characterize a bigger portion of income, driving stronger destructive working leverage.

Enterprise overview

MAN offers staffing companies, together with short-term staffing, contract staffing, everlasting work placements, and many others. The focused prospects vary throughout varied industries. Geography-wise, as of 1Q24, MAN breaks it down into the Americas (24% of income), Southern Europe (45% of income), Northern Europe (20% of income), and Asia Pacific Center East [APME] (12% of income). MAN’s aggressive moat is its scale (at $18.6 billion in income over the previous 12 months, it is among the largest gamers within the trade), which permits it to extra effectively supply for the best candidates. Due to the longstanding relationship it has already established with hiring departments, they can supply for extra “provide” of jobs for candidates as nicely.

1Q24 outcomes replace

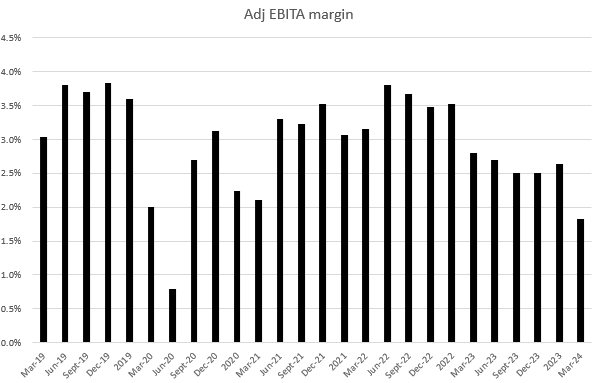

Launched on April 18, 2024, 1Q24 income fell 7.3% to ~$4.4 billion, lacking consensus expectations for a 6.7% decline. Adjusting for FX, income fell 5.5% y/y, accelerating the decline of 5.2% from 4Q23. Geography-wise, on a continuing forex foundation, Southern Europe fell 4.9% y/y, Northern Europe fell 12.1%, the Americas fell 1.1% y/y, and APME fell 4.8%. Of all of the areas, solely the Americas noticed sequential enchancment in y/y decline (1.1% in 1Q24 vs. 4.5% in 4Q23), suggesting little to no proof of restoration progress. On the revenue line, EBITA margins fell 100 bps to 1.8%, reflecting destructive working leverage. EPS got here in at $0.94, beating consensus of $0.91, however that is primarily as a result of decrease tax fee (27.9% in 1Q24 vs. 32.7% in 4Q23 and 28.9% in 1Q23).

Working situations are nonetheless weak

I believe the present working situations make the outlook for MAN’s restoration unsure and gloomy, though there are early indicators of enchancment, such because the stabilization of demand for temp staffing in key markets just like the US, UK, France, and Italy, and constructive staffing developments in LatAm and APME (word that LatAm noticed double-digit y/y income progress). This one-quarter of stability doesn’t, in my view, represent a development.

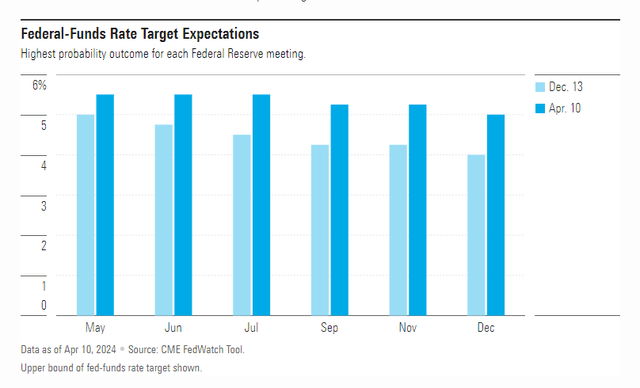

MorningStar

Only a few months in the past, the market was assured that the Fed would minimize charges by 75bps (3 cuts) by December; nonetheless, due to the sticky inflation and sizzling labor market, this has more and more turn out to be unlikely. The Fed has additionally made a press release recognizing this truth, and this has launched one other spherical of uncertainty to companies as to when they need to ramp up hiring to organize for the financial restoration. As such, I count on MAN to proceed dealing with progress headwinds as companies (in its key areas: Europe and North America) stay cautious of their hiring as they await indicators that the financial setting is on a sustainable path of enchancment.

The information from 1Q24 backs up my destructive narrative. The speed of decline in fixed forex income progress elevated from 5.2% y/y in 4Q23 to five.5% in 1Q24. Administration has talked about that they haven’t seen a constructive inflection level in temp staffing demand but, which makes it tough to foretell when income will get better. Enterprise know-how has gradual demand for short-term employees, and the manufacturing sector exterior of cars in Europe can be doing poorly, each of that are impacting MAN’s income efficiency.

In order that’s how I’d say it at this level, form of according to what Jonas stated. No inflection level at this level, however we’re seeing stability. 1Q24 earnings

Redfox Capital Concepts

Traders must also word that destructive working leverage may choose up tempo from right here, as fastened prices appear to characterize a bigger portion of income right now. As income continued to say no over the previous few quarters, adj. EBITA margins continued to fall accordingly. Given the macro uncertainty forward, I don’t see a powerful inflection in income progress anytime quickly; in distinction, it’s possible that companies will proceed to remain conservative, which may trigger income to say no additional. We now have seen within the Jun-20 quarter that margins fall quite a bit sooner when income drops under the $4 billion market (Jun-20 income = $3.7 billion).

Inside initiatives nicely place the enterprise for progress restoration

One encouraging factor is that MAN is working to enhance the effectivity and productiveness of its know-how and finance departments within the medium to long run. For instance, the institution of a worldwide enterprise companies middle in Portugal to cater to the monetary necessities of its European enterprise and the rollout of PowerSuite, a cloud-based platform for the back and front places of work, are good examples. The timing of MAN’s sturdy restoration progress is only a matter of time, in my view. The corporate seems to be well-prepared for this, because it has not incurred a restructuring cost in years. This means that the corporate has adjusted its headcount and prices appropriately to mirror the present, stabilized ranges of staffing exercise.

Steadiness sheet sturdy sufficient to tide by means of this cycle

Moreover, MAN should not have any points ready for the economic system to get better, because it has a reasonably sturdy stability sheet to tide by means of the near-term volatility. As of 1Q24, it has money and money equivalents of ~$604 million and complete debt (excluding leases) of $984 million, netting off to ~$380 million of web debt, which is simply 0.4x LTM EBITDA. With the present money stability, it could not have any points with paying out consensus anticipated dividends (c. $2.96 per share) as nicely (amounting to a complete of ~$143 million), so there isn’t a threat of a dividend minimize.

Valuation

Redfox Capital Concepts

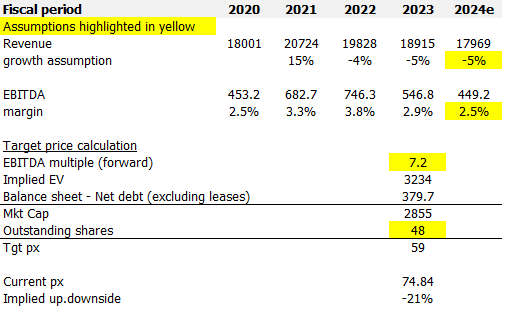

I mannequin MAN utilizing a ahead EBITDA strategy, and utilizing my assumptions, I imagine MAN is value $59. I count on MAN to proceed seeing income decline in FY24 as a result of unsure macroeconomic situations that trigger companies to stay conservative of their hiring selections. Administration’s up to date steerage for 2Q24 (they guided for fixed forex decline of two to six%, however based mostly on my changes for FX given the sturdy USD motion because the begin of April, I assumed one other 300bps of headwinds, resulting in an adjusted reported income information of -5 to -9%) is a transparent signal that 2Q24 has not seen any enhancements. I’m assuming that FY24 income will are available in on the high-end of the information (anticipating some type of financial restoration because the Fed minimize charges within the coming months). As income decline, MAN ought to see EBITDA margins decline as nicely because of destructive working leverage. Valuation ought to proceed to development at ~7.2x ahead EBITDA, much like the place friends (Randstad, Korn Ferry, and PageGroup) are buying and selling at, a mean of ~7.2x ahead EBITDA, given they’ve an identical progress outlook.

Threat

The upside threat to my promote score is that central banks in MAN’s key areas minimize charges sooner than anticipated, driving a powerful financial restoration within the coming months. This can drive extra demand for MAN’s companies, resulting in sturdy EBITDA progress (from top-line restoration and working leverage). The market can even possible drive up valuation multiples as they count on sturdy restoration progress in FY25.

Conclusion

My view for MAN is a promote score. The unsure financial outlook is inflicting companies to be cautious of their hiring, resulting in declining income for MAN, and I count on this to proceed for the close to future because the Federal Reserve is unlikely to chop charges as aggressively as beforehand anticipated. This can lead to destructive working leverage, additional pressuring profitability. Whereas MAN is taking steps to enhance effectivity and has a powerful stability sheet, these elements should not sufficient to offset the headwinds from the macro setting within the near-term.

{kind=link}