Chris Stein

Introduction

Whitecap Sources (TSX:WCP:CA)(OTCPK:SPGYF) simply launched its 1Q2024 outcomes. As anticipated, the outcomes had been glorious, plus the administration raised the manufacturing steerage with out growing the Capex, which was nice information for buyers.

On this article, I’m going to the touch on the quarterly earnings briefly. I’m then going to construct a future projection, valuation, and sensitivity evaluation.

A number of days in the past, well-respected investor Dr. Eric Nuttall recommended slowly promoting down the Canadian Pure Sources (CNQ:CA)(CNQ) and shifting all the way down to midcaps as they did not have the run-up in valuation as CNQ had.

That is precisely what I wrote a month in the past in my CNQ thesis, and it has been working effectively for me thus far.

Regardless of recommending the midcaps, Nuttall did not advocate shopping for Whitecap Sources. I’m additionally going to dive into the explanations behind it.

Whitecap Sources

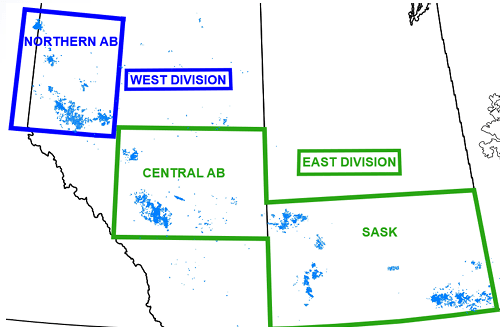

Whitecap Lands (Whitecap Presentation)

Whitecap is a midcap oil and gasoline producer with lands throughout Northern and Central Alberta and Saskatchewan with ~6k drilling areas & enormous 25+ years of reserves.

Its manufacturing combine consists of ~64% liquids. Regardless of ~36% gasoline within the 2024 manufacturing, it is very important remember that due to the low gasoline costs, it solely makes ~10% of the income. ~90% of income coming from oil makes the inventory efficiency way more correlated to grease costs than gasoline costs.

1Q2024 Replace

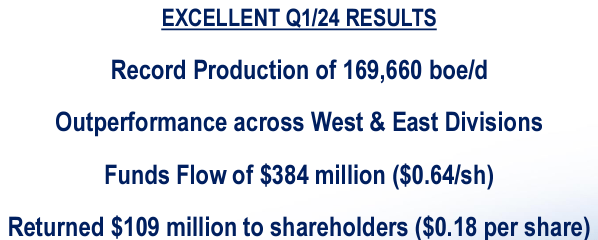

This slide from Whitecap’s presentation represents the highlights for the quarter.

1Q2024 Highlights (Whitecap’s Presentation)

To the numbers, I might simply add that the FCF was adverse for the quarter as the corporate spent ~40% of its deliberate full-year Capex, so there’s nothing unsuitable with that.

With a excessive anticipated FCF for the total yr, all above the bottom dividend needs to be directed to buybacks.

My greatest takeaway from this quarter is the elevated steerage by 2.000 boe/d with no change within the capital funds. It is a reflection of a lot better wells performances.

What’s sooner or later for Whitecap’s buyers?

I’m now going to construct up the projection mannequin, which I’ll use to worth the corporate.

Oil & gasoline costs – I’m assuming US$80 WTI, which is near the present strip and AECO, rising to C$3.5 in 2025 following the strip. TMX affect – Everyone knows that the approaching TMX pipeline has already considerably shrunk the heavy oil low cost. The TMX, in truth, not solely improves the heavy oil low cost but additionally improves the entire Canadian oil sector. As Whitecap CEO defined, the Canadian mild oil low cost to WTI is now additionally anticipated to shrink considerably, which might carry a further ~US$5/bbl income. I’m constructing the bottom case situation with this considerably decrease Canadian mild oil low cost. Understand that this upside is questionable, as no person is aware of how the differentials will behave. They is perhaps low for a yr or two however wider once more, as I anticipate the Canadian export capability is not going to sustain with the long run manufacturing output development, which could create a bottleneck in export, widening the reductions.

Benchmark Assumptions (Writer’s Projection Mannequin)

All of us have totally different opinions about the way forward for O&G costs. After we undergo the valuation, I’ll make a sensitivity evaluation with totally different worth assumptions.

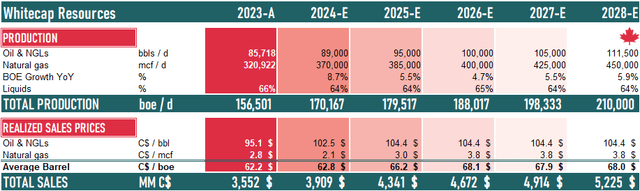

Manufacturing development – The purpose is to get the corporate to a manufacturing degree of ~210.000 boe/d. That represents a CAGR of ~6.1% from the 2023 manufacturing output of 156.500 boe/d. Realized costs – Primarily based on the shrunk reductions to WTI, I anticipate a lot better costs already in 2Q of this yr.

Manufacturing & Realized costs (Writer’s Projection Mannequin)

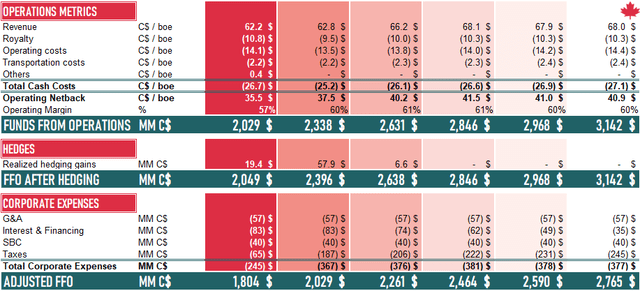

Netbacks – I anticipate almost flat prices however improved netbacks because of increased income per barrel brought on by these slim reductions.

Prices (Writer’s Projection Mannequin)

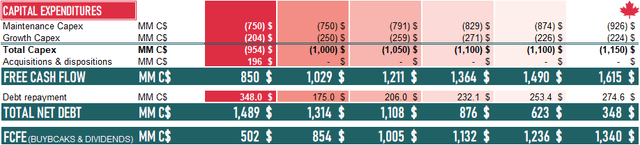

Capex – The output development must be supported by spending for development. The corporate plans for a Capex of C$0.9-1.1B. I’m going with the midpoint. C$750M is spent simply to offset the pure manufacturing declines. Because the output grows, the upkeep Capex will develop according to it.

Capex, FCF, FCFE (Writer’s Projection Mannequin)

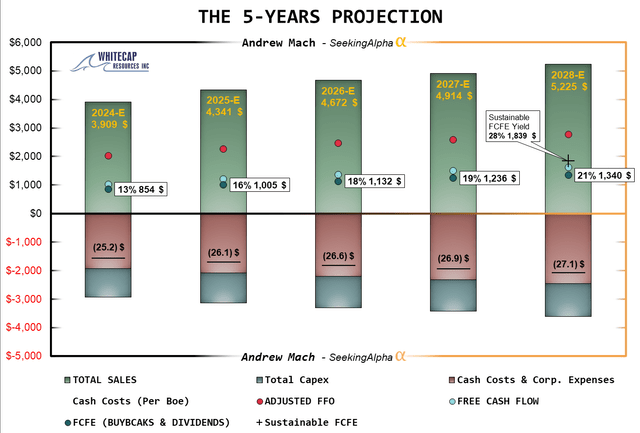

Here’s a abstract of all of the projections.

Whitecap Projection Abstract (Writer’s Projection Mannequin)

Because of these slim reductions, we might already attain very excessive yields this yr and develop quick. The bottom dividend of 6.7% prices the corporate ~C$435M, and the same quantity might go to buybacks this yr.

If the corporate switched to the no-growth mode in 2028 and simply spent to offset the declines, the yield might attain 28% with assumed oil costs.

Valuation

We will see the worth from these projected buybacks and dividends. Anyway, if I apply a 12.5% low cost charge, which I take advantage of throughout the Canadian oil sector, we arrive at a good worth of C$21, double the present worth.

DCF mannequin (Writer’s Calculation)

This doesn’t essentially imply that the value will double however somewhat that the market assumes a lot worse commodity costs or just requires a lot increased returns.

I’m not a fan of buying and selling round valuation multiples, however I imagine many skilled buyers are. In case you are one among them, listed below are the ensuing valuation multiples from my assumptions.

Valuation multiples (Writer’s Calculation)

Sensitivity

The primary danger for any commodity-producing firm comes from commodity costs.

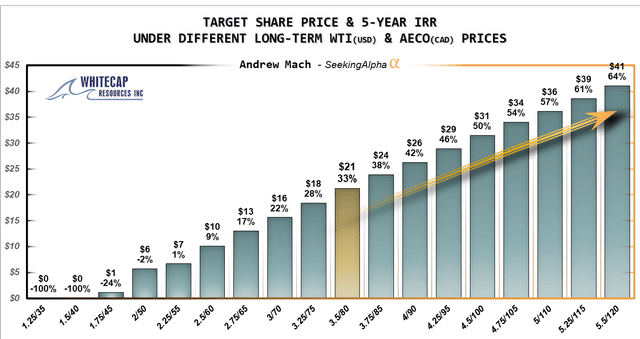

I’m working the identical PV12.5 valuation beneath totally different oil and gasoline costs to see the place the corporate’s breakeven is and the way a lot leverage towards the oil the corporate has.

Sensitivity evaluation with slim differentials (Writer’s Calculation)

The evaluation exhibits that the corporate makes sufficient FCF to offset the manufacturing declines even with a US$45 WTI and is pretty priced for oil at US$60-65 WTI.

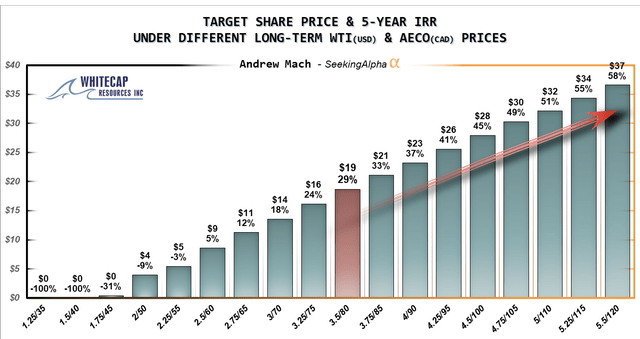

Nonetheless, we do not know the way the differentials will play out. I’m working the sensitivity evaluation yet another time, however now, with no advantages from the slim differentials. In that case, I might decrease the value goal to C$19 from C$21.

Sensitivity evaluation with broad differentials (Writer’s Calculation)

Why does Nuttall say no to Whitecap?

From the valuation, we are able to see clearly how low-cost, and I dare to say undervalued, Whitecap is. No matter low cost charge one makes use of, buyers ought to all the time examine the thesis to the opposite alternatives available in the market.

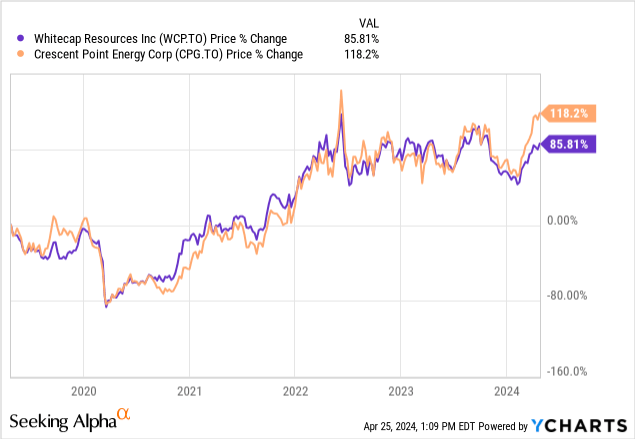

Whitecap Vs. Crescent

Crescent Level Vitality (CPG:CA)(CPG) is my largest oil holding. I not too long ago ready a five-year projection and could not assist however discover how comparable the corporate is to Whitecap.

I do not know who copies who, however the similarities make me suppose the managers are in contact each day.

Each Whitecap and Crescent personal lands in the identical geographical areas, with the same quantity of drilling areas. Each had been energetic within the acquisitions and now, after accounting for the expansion plans, have 20+ years of reserves. Each strongly deal with enhancements within the wells’ designs and are informing buyers that the brand new wells end in better-than-expected output performances.

They’ve almost similar manufacturing output, manufacturing combine, and value construction, which makes their sensitivities to grease and gasoline costs very comparable.

This may all be noticed from the very robust correlation of their inventory costs.

There are some things that differ.

Crescent has a quicker decline in manufacturing and a stronger development plan. Meaning Crescent must spend extra on sustainable Capex in addition to development Capex. Whereas Whitecap is planning to spend C$1B in 2024 Capex, Crescent plans C$1.5B.

This ends in stronger output development from Crescent, whereas Whitecap can instantly ship more cash into shareholders’ pockets through dividends and buybacks.

Total, Crescent is rising quicker, has a bigger tax pool, and realizes barely higher costs.

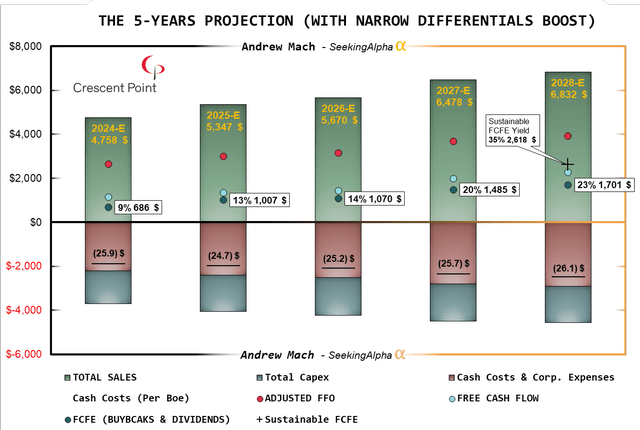

Right here is my Crescent projection in your comparability.

Crescent Projection Abstract (Writer’s Projection Mannequin)

When making use of the identical PV12.5 valuation, Crescent appears even cheaper with a worth goal of C$27 or ~125% upside.

Each names are priced very low, and one mustn’t determine based mostly on minor variations in DCF valuation outcomes. As I prefer to say: “Lengthy-term projection is like trying by a telescope; regulate the inputs a bit bit, and you’re looking at a special galaxy.

The primary cause why Nuttall and I choose Crescent is the promise from administration that they do not wish to be a part of any acquisitions for no less than the following two years, whereas Nuttall mentioned that Whitecap’s administration thinks about themself as having an edge in acquisitions and are prepared to take part in the event that they see a superb deal.

The problem with acquisitions is the paid premiums and infrequently issuance of latest shares, but additionally the easy indisputable fact that the market is prepared to pay a premium for prime shareholder payouts, which we are able to see with CNQ, for instance.

My Funding Determination

Practically all metrics are toe-to-toe, with a distinction within the timing of the payouts. Crescent comes with the next debt and extra spending for output development. Thus, I anticipate it’s going to take a bit longer earlier than the upper dividends land in my pockets.

Whitecap insiders exercise (SimplyWallstreet)

Insider buying and selling exercise additionally means that each names are low-cost as, in each instances, there’s robust shopping for exercise.

Regardless of the title change, I’m biased in direction of Crescent, and I actually don’t like the additional danger of potential acquisition.

Since each names seem undervalued, It is perhaps a fantastic thought to unfold the idiosyncratic danger and have them each in a portfolio. I see nothing unsuitable with that and don’t contemplate it “diworsification”.

I imagine that with the TMX tailwind and excessive dividends and buybacks, Whitecap is a robust purchase at these ranges.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

:max_bytes(150000):strip_icc()/GettyImages-1448623832-52fc53ba20034936aaabf25ee6cff828.jpg)

{kind=link}