chaofann

The true property funding belief, or REIT (VNQ), market is huge and versatile with over 1,000 Actual Property Funding Trusts worldwide investing in 30+ international locations and 20+ property sectors.

Subsequently, there may be really one thing for all the pieces.

There are REITs which might be well-suited for revenue traders. Others are higher for development traders. And a few might even entice the curiosity of deep worth activist traders.

Nonetheless, there’s a minority of REITs that I feel most traders ought to take into account for his or her portfolio. They stand out in that they’ve uniquely engaging enterprise fashions able to constantly producing superior returns.

Subsequently, they make very best “portfolio anchors” for many REIT traders. Listed here are two good examples of that:

Canadian Web REIT (NET.UN:CA)

I’ve beforehand described Canadian Web REIT as an early day model of Realty Revenue (O).

Immediately, Realty Revenue is a large firm, and its giant dimension will doubtless damage its future development prospects. Furthermore, the online lease market within the U.S. has additionally turn into very aggressive, decreasing the dimensions of its funding spreads.

However in its early days, Realty Revenue was very rewarding to its shareholders, incomes 15-20% annual whole returns to its shareholders.

It was in a position to provide such excessive returns as a result of:

It was quite a bit smaller It used extra leverage Its spreads had been bigger as a result of there was much less competitors.

Consequently, it grew at a a lot sooner tempo.

This brings us to Canadian Web REIT.

As mentioned, it’s an early day model of Realty Revenue that is working in Canada.

It’s tiny with a $100 million market cap. It makes use of a 50% LTV, which is above common, however its debt maturities are lengthy and well-staggered. It has traditionally been in a position to earn giant spreads as a result of Canada is much less aggressive, and this has allowed it to develop at a really quick tempo.

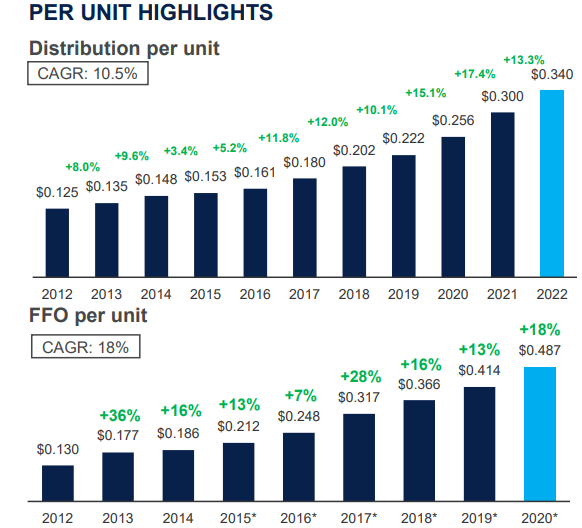

Canadian Web REIT

This fast development in funds from operations (“FFO”) per share mixed with its dividend has already resulted in big returns for shareholders.

Within the 10 years following the nice monetary disaster, Canadian Web REIT was one of the vital rewarding REITs that I do know. Buyers earned a 10x on their cash with out even counting the dividend!

And it’s nonetheless early days for Canadian Web REIT.

It’s nonetheless tiny, and I feel that it may well hold this going for a couple of extra a long time.

However in the present day, it’s supplied at an inexpensive valuation as a result of it’s going by a pace bump. The surge in rates of interest and the crash of the REIT market have made its price of capital too costly to pursue new acquisitions and briefly stopped its development. This pushed the REIT to promote a couple of properties as an alternative to repay some debt in 2023.

Even then, the REIT was nonetheless in a position to keep its FFO per share and hiked its dividend in 2023:

Canadian Web REIT

That is fairly phenomenal, all issues thought of, and the longer term seems shiny.

Rates of interest are anticipated to be minimize later this 12 months and with that, the administration expects a gradual restoration within the acquisition market, which might permit the REIT to return to development.

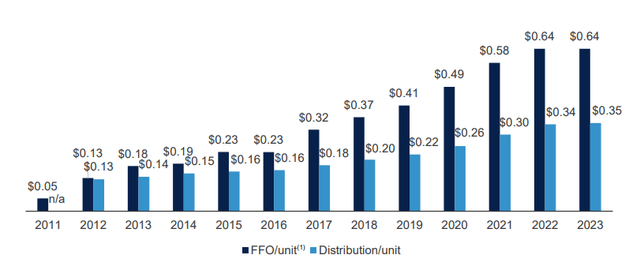

However even when that is not the case, Canadian Web REIT is not any rush. It has no main maturities till 2027, it retains almost 50% of its money stream for deleveraging, its leases get pleasure from CPI-based lease changes, and they’re comparatively brief at simply 6 years on common, and its releasing spreads are within the 5-10% vary.

This could present margin of security even when rates of interest stay greater for longer:

Canadian Web REIT

And priced at simply 8x FFO, a 20% low cost to NAV, and a close to 7% dividend yield, it actually doesn’t take a lot development to earn robust whole returns.

The administration is now additionally shopping for again shares to create additional worth for shareholders whereas their fairness remains to be discounted.

So how I see it’s that heads, I win; tails, I win massive.

If charges stay excessive and REITs stay depressed, Canadian Web will not be capable to develop a lot, if in any respect, however it should nonetheless earn vital money stream and regularly repay debt and purchase again shares to create worth for shareholders all whereas paying an enormous dividend.

And if charges are minimize and REITs get well, its fast development will resume, and its share worth will reprice quite a bit greater.

Canadian Web REIT

Beforehand, we defined that Canadian Web REIT is uniquely engaging on account of its differentiated technique, which permits it to develop externally by elevating capital and reinvesting it at a big constructive unfold, leading to robust development on a per-share foundation.

BSR REIT is extra easy than that.

Its technique is nothing distinctive. It owns house communities that generate rental revenue, and it’s not even in search of to develop externally. The cap charges in its sector are too low relative to its price of capital anyway.

However BSR is uniquely engaging due to its belongings and their long-term natural development prospects.

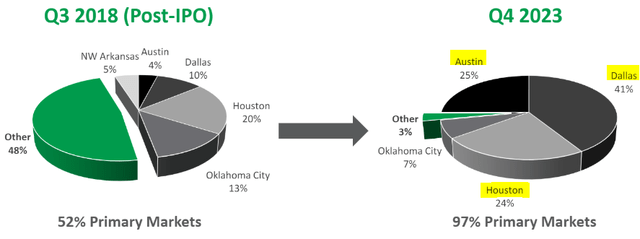

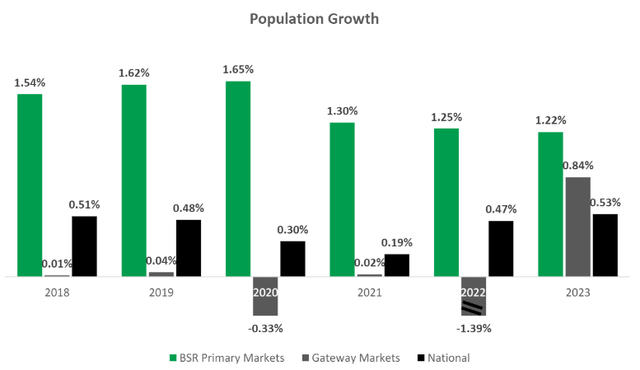

The REIT went by a multi-year portfolio repositioning main as much as the pandemic, and consequently, it’s in the present day virtually solely invested in inexpensive house communities of quickly rising Texan markets.

Most of its belongings are in Dallas, Austin, and Houston:

BSR REIT

BSR REIT

These markets are anticipated to get pleasure from among the quickest same-property NOI over the approaching decade as a result of:

They’re having fun with very quick inhabitants and job development as more and more many individuals and companies relocate there to profit from tax and value financial savings and a extra business-friendly atmosphere.The present rent-to-income ratios are in the present day nonetheless far beneath these of coastal markets. Usually, they’re in the present day as much as 2x decrease.BSR’s items, particularly, in the present day solely cost about $1,500 of month-to-month lease on common, which may be very low relative to the ~$80,000 annual revenue of its residents.On the similar time, housing affordability is at its lowest in a really very long time as a result of surging dwelling costs, excessive price of development, and elevated rates of interest.Texas has among the highest property taxes within the nation, however there may be vital political momentum towards decreasing these taxes, which may quickly enhance similar property NOI. This might be uniquely helpful to BSR.

BSR REIT

Because of this, BSR can continue to grow its similar property NOI even in the present day as its markets are severely oversupplied. It has guided for ~2% development in 2024 at the same time as most different house REITs expect a slight drop in rents.

This bodes very properly for 2025 and past as a result of new development begins have now dropped to the bottom degree for the reason that nice monetary disaster as a result of excessive rates of interest and inflation. Because the oversupply turns into undersupply, lease development will speed up, and I count on BSR to guide the pack once more.

However regardless of having fun with above-average long-term lease development prospects, BSR is in the present day priced at an exceptionally low valuation. It’s among the many least expensive in its property sector. It’s even cheaper than Mid-America Residence Communities (MAA) and Camden Property Belief (CPT):

BSR REIT P/FFO 11x P/NAV 0.6x Dividend Yield 5% Click on to enlarge

That is doubtless due to its small dimension and likewise as a result of it’s primarily listed in Canada. Canadian traders might not perceive simply how briskly its rents are more likely to develop over the long term.

BSR’s administration owns 40%+ of the corporate, and they’re in the present day busy shopping for again as many shares as they will whereas they’re closely discounted relative to their internet asset worth. Within the final quarter alone, they purchased again one other $30+ million value of shares, which is important for a corporation of this dimension.

It’s creating numerous worth and as rates of interest return to decrease ranges, and lease development accelerates within the coming years, I count on all of this hidden worth to be unlocked and BSR to richly reward its shareholders.

Simply two years in the past, it traded at a premium to its NAV, so I’ve little doubt that it may well get there once more because the market sentiment for REITs recovers.

Closing Notice

Most REITs are solely appropriate for particular kinds of traders.

However NET.UN and BSR are exceptions that would make sense for many traders, in my view.

There are ~20 such instances within the REIT sector, and people are the kinds of REITs that we’re concentrating on.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

:max_bytes(150000):strip_icc()/What-difference-between-standard-Error-means-and-standard-deviation_color-1c203133aca641aca0d03936d9558693.jpg)

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}