Balazs Sebok

BNP Paribas (OTCQX:BNPQY) (OTCQX:BNPQF) purchase case recap was primarily based on the next:

M&A optionality after the Financial institution of the West disposal, we additionally observe up with a particular observe on the ABN AMRO rumors. A forecast of stable and strong outcomes over the interval. A restricted Russia publicity. An upside due to our evaluation of the Arval division.

Right this moment, we’re not shocked to see a optimistic inventory worth response after that the corporate launched its half-year numbers. BNP’s solely miss was on the CET1 ratio.

No extra information was reported on BNP’s Russian actions and the corporate doesn’t touch upon prospect M&A transactions, however we’re delighted to report just a few firm notes on our two factors above:

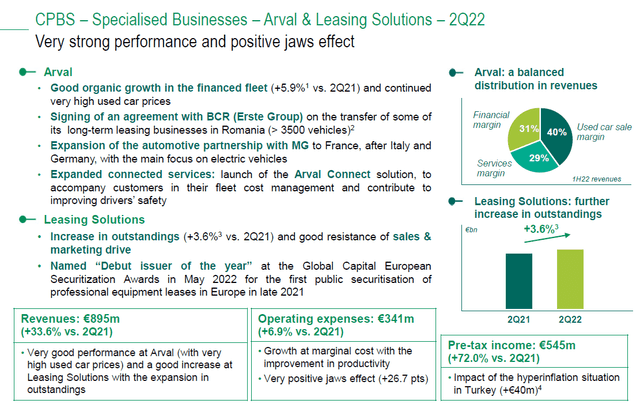

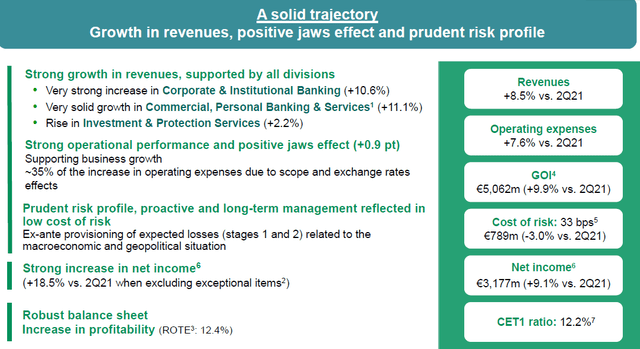

Regarding level 2) “Within the working divisions, revenues elevated by 9.7% in comparison with the second quarter 2021” Concerning Arval (level 4): “revenues rose strongly up by 33.6% in comparison with the second quarter 2021 due to used automotive costs and income development”. This was just about consistent with Mare Proof Lab’s expectations. We must also observe that there was a optimistic one-off for a complete consideration of €40 million because of the hyperinflation registered in Turkey.

Arval efficiency

Q2 Outcomes

Wanting on the three-month numbers, revenues elevated by 8.5% to €12.78 billion. The enterprise grew in all the corporate divisions due to a +11.1% in retail banking and +10.6% within the funding banking arm (regardless of one of many worst monetary markets in historical past). Prime-line gross sales have been additionally pushed by the mounted earnings division which delivered a plus 14.8% in Q2. A optimistic efficiency was registered in fairness buying and selling which grew by 16.1% because of the market volatility. It’s attention-grabbing to report the truth that income grows at a better price than working bills, 8.5% versus 7.6%.

BNP Q2 Outcomes snap

The most important financial institution in France reported a internet earnings up 9.1% to €3.1 billion effectively past analyst consensus expectations that have been forecasting €2.7 billion. As well as, the price of threat stood at €789 million, round €100 million under consensus expectations, whereas the financial institution remarked on its “prudent threat administration”.

As we already talked about, the CET1 capital ratio stood at 12.2%, -20 foundation factors from consensus and -20 foundation factors quarter on quarter. This was resulting from a rise in risk-weighted belongings. Nevertheless, we must also observe some help by enhanced profitability and a ROTE of over 12%.

The CEO defined that “BNP Paribas’ outcomes are stable and mirror its skill to mobilize greater than ever all its sources and enterprise strains to help people, corporates and establishments in all phases of the financial cycle”. He additionally added that the corporate “pursues its development trajectory, its technological developments, and helps its shoppers of their transition in direction of a extra sustainable economic system”

Conclusion & Valuation

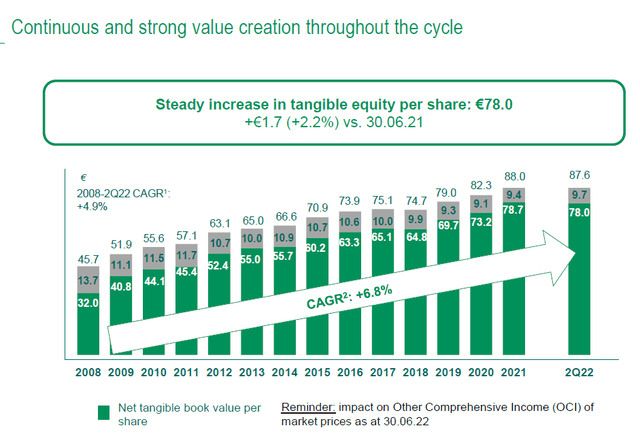

Yr to this point, BNP Paribas inventory has underperformed the European financial institution’s index with a decline of round 26.5% in comparison with the -22% inside the sector. We anticipate an improve of the consensus estimates. Cross-checking our inner estimates, our inner group has left all unchanged. BNP buyback is confirmed and the corporate is buying and selling at simply over 0.5x of its TBV. With a ROTE of 12% confirmed by the current outcomes, we see no justification to decrease our goal worth that’s derived from a median valuation between:

A sustainable ROTE at 9% A TBV of 0.9x

Is BNP Inventory A Purchase? Conclusion

Sure, we reiterate our Purchase ranking at 72€ per share.

BNP TBV evolution

Dangers to our goal worth are:

Asset high quality and future provision evolution. Capital pattern (since natural capital era was restricted within the first half of the 12 months). Sensitivity to macro developments (rates of interest, potential recession, and so forth.). Asset administration developments and return on capital.

/what-difference-between-magnum-cum-laude-and-summa-cum-laude_V2-3ae02babdc714ea9adaeec0f0a6bf1a5.png)

{kind=link}