-Oxford-

We’re buy-rated on finance software program firm Intuit Inc. (NASDAQ:INTU). Regardless of inflationary pressures and rising rates of interest, Intuit’s monetary tech platform has been resistant relative to the bigger tech group, and we suggest shopping for the inventory at present ranges.

Intuit operates within the monetary software program business, estimated to develop at a CAGR of 9.2% between 2021-2031. We imagine Intuit’s place inside the monetary software program business has made its companies more-or-less indispensable, even throughout market downturns. Intuit’s fiscal This fall 2022 report in August confirmed income progress of 32% Y/Y and outpaced EPS expectations by round 12% – underlying that Intuit’s buyer base is extra resilient than anticipated for a fintech firm underneath present circumstances.

We anticipate Intuit to proceed outperforming expectations by 2023 for 2 causes. First, we anticipate the corporate to see demand tailwinds for its two foremost merchandise: QuickBooks and TurboTax. These two merchandise have confirmed resilient to Fed rate of interest hikes and macroeconomic headwinds for probably the most half. Second, the shift of monetary companies from software-based options to cloud-based ones. The enterprise world is quickly shifting to the cloud, and we anticipate specializing in the cloud will likely be a progress catalyst for Intuit in the long term. Intuit continues to be not low-cost, however the inventory is down 36% YTD. We imagine the inventory pullback offers a beautiful entry level into the center of the monetary software program business.

Bullish on the monetary software program business and shift to the cloud inside it

Intuit develops and sells monetary, accounting, and tax preparation software program inside the broader monetary software program business. We like Intuit’s place inside the business as a result of we anticipate it the profit from the fast shift from conventional strategies of managing monetary data to finance and accounting data software program companies. We imagine Intuit will trip the rising demand for computerized accounting.

Whereas we’re bullish on the ripe-for-picking nature of the monetary software program business, we’re particularly buy-rated on Intuit due to the corporate’s shift from promoting software-based options to cloud-based options. Cloud is on the middle stage of the tech area, and we imagine Intuit will acquire extra momentum going ahead with cloud-based options. With cloud-based options, Intuit will have the ability to supply clients the pliability of accessing their data from wherever. The shift falls inside the Software program as a Service ((SaaS)) market, forecasted to develop at a CAGR of 25.9% between 2021-2028.

Resilient buyer base underneath present monetary stressors

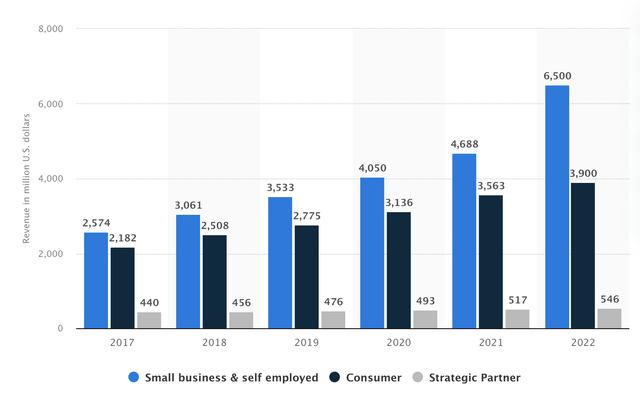

Whereas Intuit has 4 segments, the corporate derives most of its income from two segments which have confirmed comparatively resilient to the present market downturn: Small Companies and Self-Employed Teams and Shoppers. The previous makes up round 51% in FY2022, whereas the latter accounts for about 31% throughout the identical interval.

The next graph outlines Intuit’s complete revenues by section worldwide between 2017-2022.

Statista

Every section encapsulates certainly one of Intuit’s two foremost merchandise: QuickBooks underneath the Small Companies and Self-Employed Group and TurboTax underneath the Client one. If in case you have a small enterprise, you have most likely interacted with QuickBooks, and should you file your individual taxes, chances are high you have reverted to TurboTax. We imagine Intuit’s QuickBooks and TurboTax exist in a protected haven, even throughout a market downturn. The corporate’s FY2022 reported 38% Y/Y progress for Small Enterprise and Self-Employed teams. Client Group income additionally elevated by 10% Y/Y. We imagine the key to Intuit’s customer-base resilience is that its enterprise mannequin saves corporations time and cash.

Dangers to the purchase thesis

Intuit is just not with out dangers. There nonetheless stays plenty of uncertainty concerning the finances spending of small companies and self-employed people. Small Companies and Self-Employed segments make up most of Intuit’s income. Therefore, the corporate’s weak to smaller companies reducing budgets because of near-term world macroeconomic headwinds. The corporate’s concurrently weak to the cyclicality of buyer demand. Intuit sees the very best demand within the second and third quarters, the U.S tax seasons. The corporate is reliant on heavy cyclical demand, and we anticipate that if Intuit doesn’t benefit from the anticipated demand within the U.S tax season, its profitability will likely be damage.

Inventory efficiency

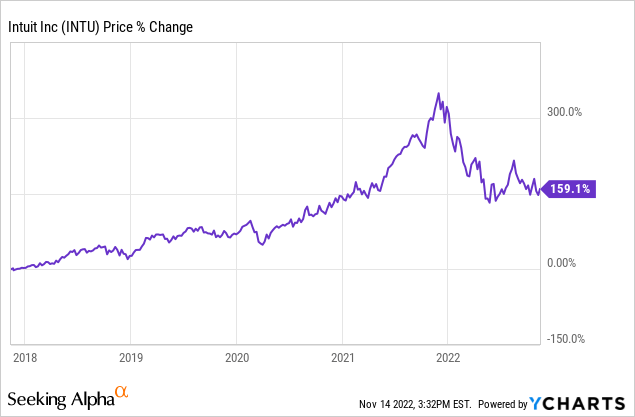

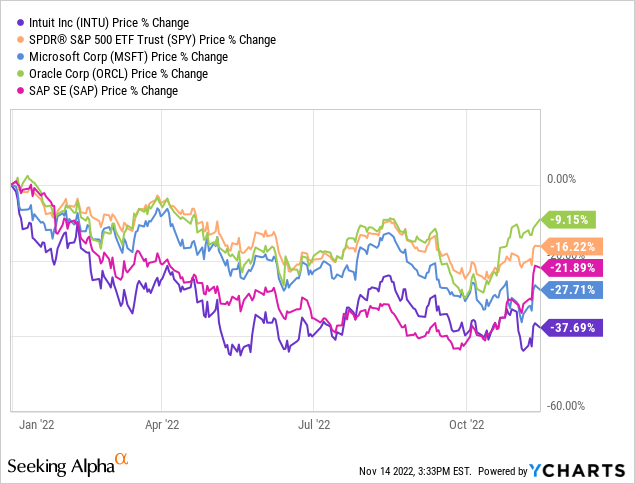

Intuit’s grown a powerful 156% over the previous 5 years. YTD, the inventory is down 36% alongside a lot of the tech peer group. Intuit has underperformed the S&P Index (SPY), which has solely dropped about 17% YTD. Relative to the competitors, Intuit underperforms YTD of SAP SE (SAP), which fell round 15%; Oracle (ORCL) decreased by about 10%, and Microsoft (MSFT) by about 27%. We like Intuit’s underperformance YTD, because it creates a beautiful entry level to put money into the corporate. We suggest traders purchase the inventory at present ranges, as we anticipate Intuit to develop meaningfully in 2023.

TechStockPros

TechStockPros

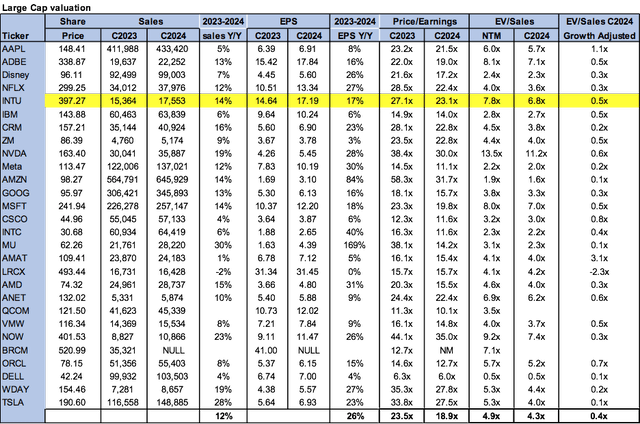

Valuation

Intuit is just not low-cost. The inventory is buying and selling at 23.1x C2024 EPS $17.19 on a P/E foundation in comparison with the peer group common of 18.9x. On the EV/Gross sales foundation, the inventory is buying and selling at 6.8x C2024 versus the peer group common of 4.3x. Intuit is richly valued; nonetheless, we imagine the inventory is a progress inventory and suggest traders purchase at present ranges.

The next graph outlines Intuit’s valuation relative to the peer group.

TechStockPros

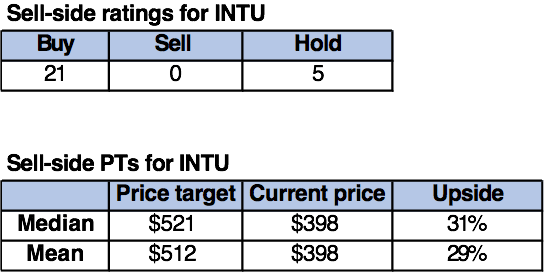

Phrase on Wall Avenue

Wall Avenue is bullish on the inventory, and so are we. Of the 26 analysts overlaying the inventory, 21 are buy-rated, and 5 are hold-rated. The inventory is at the moment buying and selling at $398. The median worth goal is $521, and the imply worth goal is $512, with a possible upside of 29-31%.

The next are Intuit’s sell-side scores and worth targets.

TechStockPros

What to do with the inventory

Whereas a lot of the fintech peer group does not look fondly at 2022, Intuit stands out. The corporate had an incredible FY2022 – buying MailChimp, and growing income by 32% Y/Y. Intuit’s not solely worthwhile, but it surely’s additionally rising. We like Intuit’s place inside the monetary software program business and anticipate the corporate to see elevated demand tailwinds as macroeconomic headwinds ease. We additionally imagine the corporate is a “protected haven” throughout the present market downturn due to its comparatively resilient buyer base and indispensable companies. We suggest traders purchase Intuit Inc. on the pullback.

:max_bytes(150000):strip_icc()/GettyImages-1472083948-775e9fc6b6234908b7263070412a55ee.jpg)

{kind=link}