filadendron

Thesis

My thesis right here is absolutely easy. I’ll argue that Google (NASDAQ:GOOG) and Meta Platforms’ (NASDAQ:META) AI potential are mispriced. And I’ll make the argument in two steps. First, I’ll analyze META and GOOG’s substantial valuation low cost in comparison with different AI shares resembling Microsoft (MSFT). And the important thing level I need to make right here is that META and GOOG are priced as if they’ve already misplaced the AI race. And this results in the second a part of my argument. I’ll argue that the competitors amongst Google’s TensorFlow, Meta’s LLaMA, and Chat-GPT has solely begun. There is no such thing as a clear loser or winner for my part.

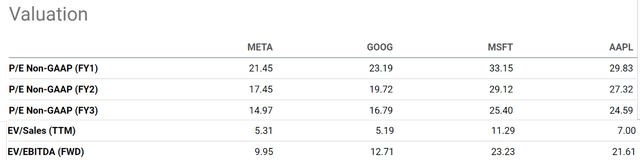

The primary a part of the argument is comparatively simple, and I’ll make it in a short time right here utilizing the desk proven under. As you possibly can see, when it comes to FY1 P/E ratios, META and Google are priced within the vary of 21x to 23x. In comparison with Microsoft’s 33x P/E, this can be a low cost of about 1/3. On the similar time, keep in mind that each Google and META maintain extra cash and fewer debt on their steadiness sheet. Because of this, the valuation low cost is much more dramatic when you think about leverage-adjusted valuation multiples resembling EV/gross sales and EV/EBITDA ratios. As seen, META and GOOG are discounted from MSFT and Apple (AAPL) by about ½ in these ratios. Word that the purpose right here is to not examine their steadiness sheet energy. All of them have very good steadiness sheet energy. My objective right here is to investigate valuation multiples solely.

Then I’ll transfer on to the second a part of my argument in regards to the AI race.

Supply: Looking for Alpha knowledge

TensorFlow, LLaMA, and Chat-GPT

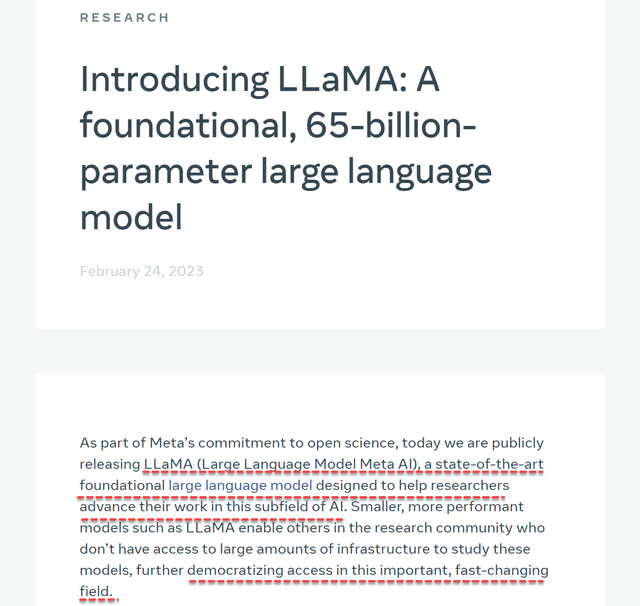

For readers new to those AI terminologies, the very best analogy that I can consider is to check their function within the AI world to the function working methods play within the PC world. All three platforms are primarily based on deep studying fashions and their objective was to facilitate the event and coaching of different studying fashions (much like the objective of working methods within the PC world). META reiterated this mission assertion of their most up-to-date analysis paper on LLaMA (see the highlighted sentences under). The entire paper is an fascinating learn for traders who’re inquisitive about giant AI fashions nowadays (and their mindboggling parameters and computation energy).

Supply: META analysis article

Most of us learn about Chat-GPT not too long ago due to its big reputation. Nevertheless, the opposite platforms are additionally extensively used and deeply entrenched within the AI trade. And every platform has its personal strengths and weaknesses. For instance, GOOG’s TensorFlow is a well-liked alternative for builders as a result of it’s open-source and straightforward to make use of. Nevertheless, it may be sluggish and inefficient for large-scale initiatives. LLaMA is a more moderen platform that’s designed to be quicker and extra environment friendly than TensorFlow. Nevertheless, it’s not as extensively adopted as TensorFlow, which signifies that there are fewer sources accessible for builders. And naturally, Chat-GPT is a platform that’s particularly designed for pure language processing duties. It is extremely correct and environment friendly, however it’s not as versatile as TensorFlow or LLaMA.

As such, my total conclusion is that there isn’t a clear winner or loser within the competitors between these three platforms at this level. And subsequent, I’ll argue that every platform is backed by a significant expertise firm with deep pockets. Which means every platform has the sources to proceed creating and bettering its expertise. The competitors between these three platforms is prone to proceed for a while. Ultimately, one might dominate or all three co-exist. It’s too early to say which platform will in the end emerge because the winner.

The AI race is simply starting

When it comes tech shares, our total philosophy is NOT to spend money on a given inventory primarily based on our confidence in a single product, whether or not it’s iPhone or AI. As a substitute, we deal with sustainable funding for R&D and the effectivity of the R&D course of.

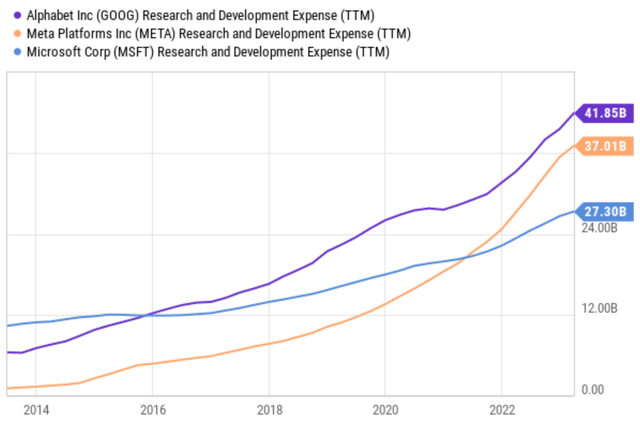

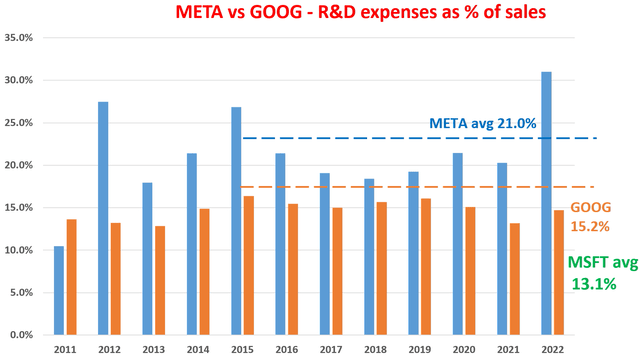

When it comes to R&D, all main gamers make investments closely in new R&D, they usually have well-established product traces to sustainably and aggressively function new instructions. As proven within the charts under, Google and Meta are literally spending extra on R&D than MSFT in recent times – each when it comes to absolute greenback quantity and as a proportion of whole gross sales. To wit, Google spent $41.9 billion on R&D TTM, Meta spent $37.0 billion, and Microsoft spent “solely” $27.3 billion. And AI has been a focus space the place all these main gamers are presently emphasizing. Estimating a quantity can be troublesome as a result of a lot of their analysis areas overlap (e.g., META digital actuality and AI, or MSFT’s clever workplace suites and AI). However primarily based on their public disclosures and the interviews with trade specialists, my estimate is about 20-30% of their R&D price range is devoted to AI analysis.

Supply: Looking for Alpha knowledge Supply: Creator primarily based on Looking for Alpha knowledge

And I foresee the AI race to be an extended drawn-out race. All gamers are well-positioned to maintain investing in these areas and keep within the race for a few years to come back. All of them have sturdy monetary positions, current merchandise that benefit from the cash-cow standing and very good profitability, and entry to an unlimited pool of expertise.

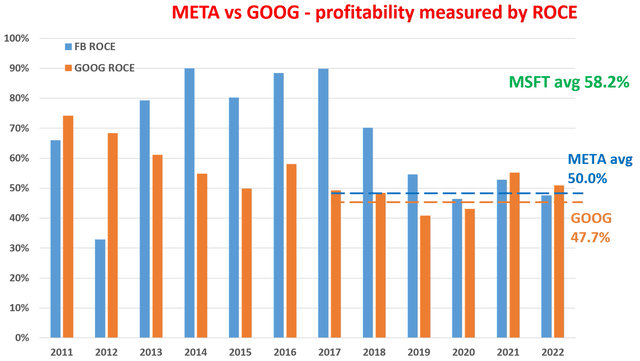

For instance, the next chart highlights their profitability when it comes to ROCE (return on capital employed). I’ve written articles purely devoted to the analyses of the ROCE for GOOG and META earlier than, and you’ll find the main points there if . Only a very transient recap right here after which I’ll simply straight quote and touch upon the outcomes. In these outcomes, I handled the next issues as their capital really employed: working capital consisting of payables, receivables, stock (however not money), web property, plant, and gear, and at last R&D bills. As seen, META’s ROCE averaged about 50% since 2017 (after its profitability normalized from the 90% stage in earlier years). And GOOG’s ROCE averaged round 48%. MSFT’s ROCE is comparatively greater at about 58.2% on common since 2017. And the important thing phrase right here is exactly “comparatively.” A ROCE on the order of fifty% could be very aggressive already and may help wholesome progress with minimal reinvestment, as detailed subsequent.

Supply: Creator primarily based on Looking for Alpha knowledge

Return projections, dangers, and ultimate ideas

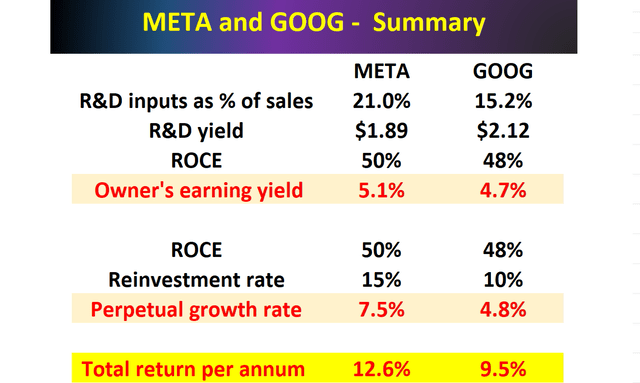

In the long run, how sustainably a enterprise can develop its earnings depends on two parameters: ROCE and reinvestment fee (RR, a.ok.a., the plow-back ratio). Extra particularly, Lengthy-Time period Development Fee equals the product of ROCE and RR.

Based mostly on this framework, the desk under summarizes my projected potential returns for META and GOOG. As seen, at their present RR (about 15% for META and 10% for GOOG), they may keep a 7.5% and 4.8% natural progress fee (that is actual progress with inflation excluded). At their present valuation multiples, additionally they supply an proprietor’s earnings yield (“OEY”) of round 5%. Because of this, each supply very favorable odds for whole annual return potential within the double digits, even earlier than including the inflation escalator.

Supply: Creator primarily based on Looking for Alpha knowledge

Dangers

Right here I’ll deal with the uncertainties surrounding their R&D, since that is the half that’s most related to the thesis. Each META and GOOG are underneath strain to cut back their R&D bills. Each META and GOOG are underneath strain to proceed investing in innovation to remain forward of the competitors. Nevertheless, each corporations should steadiness varied competing pressures together with macroeconomic circumstances, the pattern within the digital advert area, and in addition regulatory insurance policies. The worldwide financial slowdown might result in a lower in income for each META and GOOG. Promoting is particularly delicate to an financial slowdown, which might make it tougher to maintain their excessive R&D bills. The rise of advert blockers might additionally result in a lower in income for these corporations, which is a key space for each and contribute the majority of their present revenue. Regulatory challenges in some components of the world might additionally make it tougher for these corporations to maintain their excessive R&D bills.

Verdict

All instructed, my ultimate verdict is that these dangers are greater than correctly priced in already. And as such, I view each shares as considerably mispriced. In a nutshell, I view them as two sturdy AI contenders priced as losers at first stage of the AI race. As such, they provide return potentials which might be rather more favorable than different main AI shares can supply (say MSFT) for my part. As talked about above, each supply very favorable odds for whole annual return potentials near or exceeding 10% even earlier than contemplating inflation escalator or valuation enlargement. In distinction, my projection for MSFT’s whole return potential is within the upper-single digit resulting from its elevated valuation (thus decrease OEY), decrease RR, and in addition a really probably P/E contraction.

:max_bytes(150000):strip_icc()/INV_MoneyMarketDepositAccounts_GettyImages-530281091-bd867f3b87534609a7e36ede5d6beb1c.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1472083948-775e9fc6b6234908b7263070412a55ee.jpg)

{kind=link}