hafakot/iStock by way of Getty Photographs

That is my first article on Palantir Applied sciences (NYSE:PLTR), a sizzling IPO from 2020 that’s simply now turning the nook to working profitability. The corporate is a expertise concern, promoting software program to parse by means of tons of database info to seek out patterns and glean outcomes from specified queries. It is important goal is to assist the intelligence group in the US spy on folks, reworded to the politically-correct terminology as helping in counterterrorism investigations and operations. For positive, it is a very important trade in at this time’s courageous new on-line laptop world. However is it actually a development trade, and is Palantir actually a development inventory? These are points I’ve struggled to know because it started public buying and selling.

The 2023 declare to fame and future fortunes is the corporate’s remolding of its picture with buyers – as a high AI selection (synthetic intelligence) for database administration, analytics and determination making. I’ll say advertising and marketing the corporate as an AI winner is certainly sexier than saying we’re the world’s spy chief, plus the market alternative is materially bigger.

Palantir Web site – November 18th, 2023 Palantir Web site – November 18th, 2023

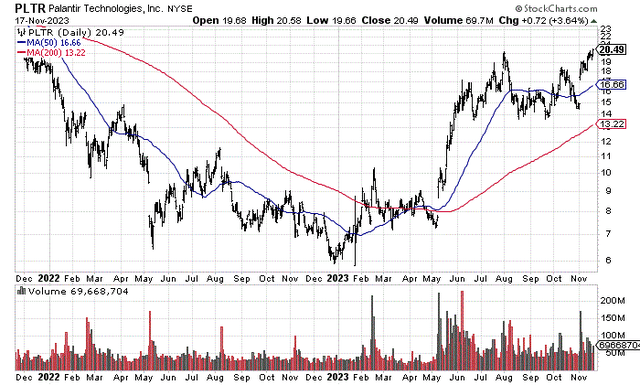

And, Palantir has change into a high funding gainer throughout 2023 on the AI pleasure visiting Wall Avenue (will it keep or will it go?), with a year-to-date bounce of +220%! The query for brand new buyers revolves round whether or not or not this dramatic change in enterprise price is sustainable. Do development charges in underlying metrics this yr and subsequent truly assist the share valuation?

My easy reply is I doubt it. The valuation at this time is amazingly stretched, whereas the share quote seems fairly prone to disappointment in 2024.

So, if a bear market in Massive Tech is approaching (like I’ve been explaining for the reason that summertime in different names), Palantir will nearly certainly take part on the draw back. My view is the speedy draw back danger of a -30% to -40% worth decline far outweighs potential upside of +10% to +25% by the top of 2024. My conclusion is hot-money merchants and novice, simply excitable buyers have piled into PLTR throughout 2023, and pushed the valuation manner forward of working outcomes. A 6-month to 12-month interval of cooling within the share quote is my expectation. As such, I charge the corporate a Promote and Keep away from in the interim.

StockCharts.com – Palantir, 24 Months of Day by day Value & Quantity Modifications

The Overvaluation Downside

As an investor you must not solely dream of what upside is coming, but additionally perceive what you’re paying for the privilege. A whole investment-process overview consists of weighing each potential rewards and dangers, if you’ll.

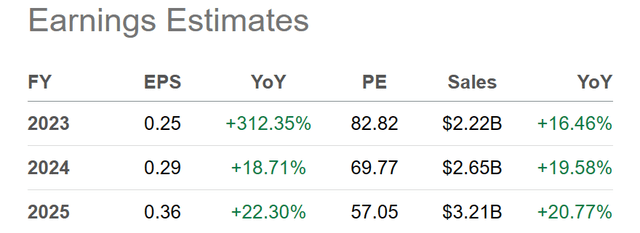

At $20+ a share, the full fairness capitalization of Palantir is $43 billion. The excellent news is the stability sheet could be very sturdy, with almost $3.3 billion held on the finish of September vs. $922 million in complete liabilities. Nonetheless, revenues for this yr are projected at simply $2.2 billion with $520 million in non-GAAP money earnings. In the meantime, analyst projected enterprise development charges round 20% yearly for 2024-25 can be properly above common vs. different U.S. corporations, though not unimaginable.

Searching for Alpha Desk – Palantir, Analyst Estimates for 2023-25, Made November seventeenth, 2023

Even worse information, $520 million in adjusted money earnings and $475 million in “free” money stream during the last 12 months have been mainly a perform of worker compensation by means of inventory choices and awards of $472 million. I’ll say that is how Silicon Valley and Massive Tech typically run companies at this time, with outsized funds in inventory for work, not the same old money funds for labor. For positive, once you strip out inventory compensation to staff, the entire sector seems much more overvalued than you’d guess utilizing GAAP accounting metrics.

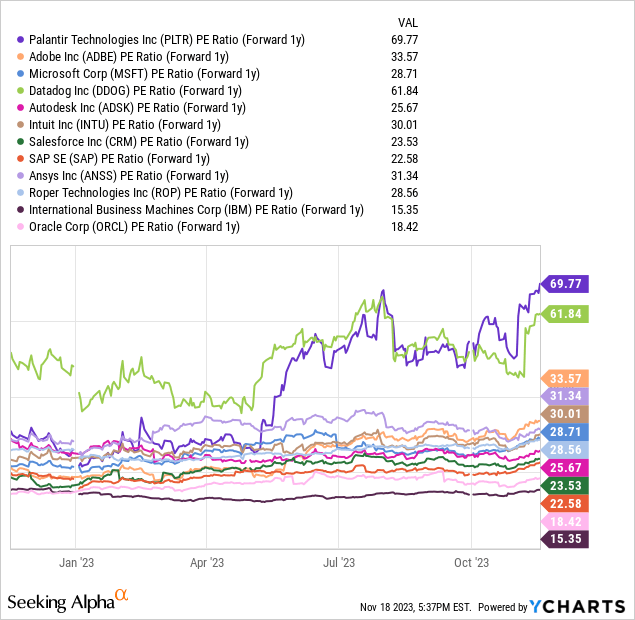

Anyway, utilizing $520 million in cash-adjusted earnings (as a substitute of GAAP accounting nearer breakeven for revenue), the share worth valuation nonetheless represents a sky-high ratio of 82x annual 2023 revenue estimates. The S&P 500 blue-chip index is within the low-20s for a comparable P/E a number of. When pricing 12 months of future anticipated development, Palantir has moved from a valuation choose in the identical space as friends a yr in the past to essentially the most overvalued place in big-data analytics and utility software program at present. The projected 1-year ahead P/E of just about 70x is exceptionally wealthy. As compared, most friends are buying and selling beneath 30x.

YCharts – Palantir vs. Massive-Information Software program Friends, Value to 1-Yr Ahead Earnings Projections, 12 Months

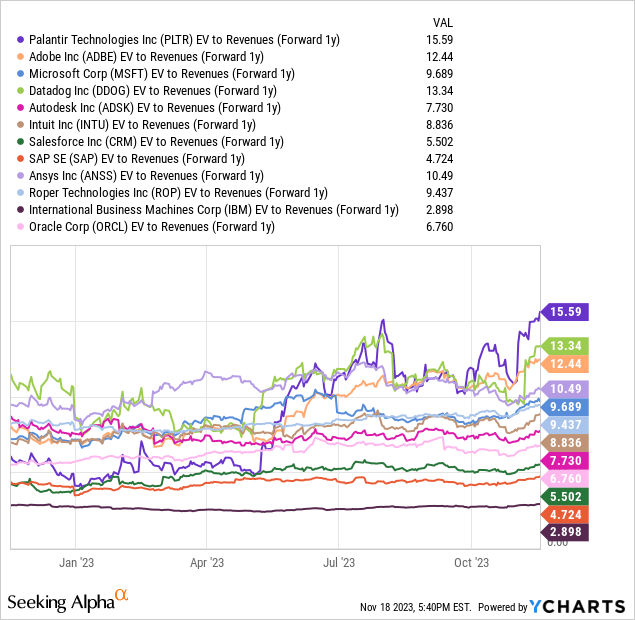

After adjusting firm values to money available and zeroed out debt, the enterprise worth calculation on 2024 gross sales can be fairly stretched. To make any sense, enterprise development has to take off quickly to catch as much as the rocketing share quote. The 15x EV a number of on future income expectations is a tough 70% premium to the trade common of 9x. If there is a silver lining, the sturdy stability sheet flush with money and strong enterprise development prospects do pull the common worth to “trailing” gross sales a number of of 20x, all the way down to an EV to gross sales ratio of 15x.

YCharts – Palantir vs. Massive-Information Software program Friends, EV to 1-Yr Ahead Income Projections, 12 Months

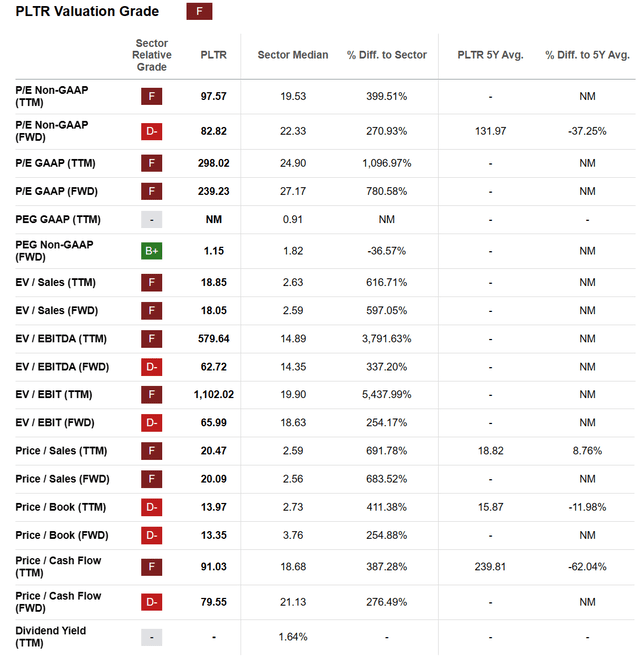

Searching for Alpha’s laptop rating system offers Palantir an “F” Valuation Grade general, in comparison with a listing of sector-average elementary ratios and several other 5-year seems at previous PLTR working outcomes.

Searching for Alpha Desk – Palantir, Valuation Grade on November 18th, 2023

Last Ideas

Traders considering including Palantir shares have to suppose lengthy and arduous if the premium valuation is price shopping for, particularly if development charges decelerate in a recession subsequent yr (as a substitute of accelerating on AI development).

My Promote ranking on Palantir is for a strict 12-month outlook. It is totally attainable the group’s AI push will result in thrilling development for the working enterprise and shareholders. But, in a bear market on Wall Avenue subsequent yr (which is my baseline projection outlined in earlier articles) a drop in PLTR’s worth again to $15 and even $12 can’t be dominated out. At that stage, we’d expertise an extremely good entry for a 5-year holding interval. My abstract view is the AI craze for buyers will subside, and higher valuations will seem ultimately for Palantir.

How might I be unsuitable? In fact, if working outcomes begin to spike past present analyst projections, a $25 or $30 worth stays an outlier chance in 2024. I might say a zigzag sample to $30 within the first half and correction again to $25 (not far above at this time’s quote) by the top of 2024 can be my most bullish outlook situation.

One other situation with a minor chance is Palantir turns into the goal of a takeover by a bigger fish wanting publicity to the AI story. The likes of Microsoft (MSFT), Oracle (ORCL), or Worldwide Enterprise Machines (IBM) is perhaps concerned about a hookup in some unspecified time in the future. My challenge is at this time’s excessive valuation could imply solely a slight share worth premium is obtainable within the low to mid-$20s. I do imagine the chances of a proposal might enhance by subsequent summer time, given a far decrease inventory quote beneath $15, and an acquisition worth round $20 with a transaction cut-off date in early 2025. Such would enable the enterprise to develop into the providing worth paid. Sadly, should you purchase your PLTR shares above $20 at this time, there would not be any upside captured in the long run.

In case you are within the AI way forward for Palantir, the inventory could possibly be one to look at carefully, with the battle plan of shopping for on weak spot. I might use a cost-average strategy over the following 3-6 months. You possibly can buy a small place beneath $18, add to it within the $15-16 vary, whereas getting extra aggressive beneath $14 (if this worth stage reappears in 2024).

Once more, underlying enterprise development charges of 20% don’t assist a trailing P/E effectively above 70x or a a number of on gross sales near 20x. I would favor half that valuation, all else being equal. Ready to buy Palantir nearer to 35x EPS and 10x gross sales would provide you with much better odds of making a living years down the highway. (I personally can not bear in mind many breakeven GAAP revenue performs with 20% development charges promoting for worth to income numbers effectively above 10x, over my 36+ years of buying and selling, excluding the late-Nineties Dotcom bubble period.)

So, both firm development has to select as much as a charge above 30%, or the inventory quote must fall again to rebalance with its average projected path of earnings and gross sales enlargement. No feelings or overoptimism, simply the maths.

With out the exaggerated AI hype for the reason that spring, I determine Palantir would nonetheless be buying and selling round $11-$12 per share. For example the hype fades subsequent yr, whereas base firm metrics rise one other 20%. That will give us a “truthful worth” goal in 12 months of $14.50 to $15 a share, down roughly -25% from at this time.

That is my tackle Palantir in November 2023. Hopefully, this text will add worth to your analysis and determination course of.

Thanks for studying. Please contemplate this text a primary step in your due diligence course of. Consulting with a registered and skilled funding advisor is really helpful earlier than making any commerce.

:max_bytes(150000):strip_icc()/GettyImages-1472083948-775e9fc6b6234908b7263070412a55ee.jpg)

{kind=link}