izusek

After the bell on Wednesday, we acquired fiscal third quarter outcomes from BlackBerry (NYSE:BB) for the corporate’s November ending interval. Over the previous decade, shares have been one of many worst performers available in the market as a income turnaround has fully did not materialize, and now extra main modifications are within the works. The newest set of outcomes have been lower than spectacular but once more, clouding the general future right here a bit extra.

For fiscal Q3, BlackBerry reported revenues of $175 million. This quantity was up $6 million year-over-year and soared dramatically on a sequential foundation from the greater than a decade low of $132 million that was reported in Q2. Sadly, the full high line quantity missed avenue estimates by almost $6 million. For as soon as, the Cybersecurity section confirmed a pleasant quantity, with revenues rising by $8 million over the prior yr interval to $114 million. The IoT enterprise continued its long term progress development by including $4 million to $55 million. A few of these good points have been offset by the Licensing section, which might be very risky quarter to quarter, and this time confirmed a 50% year-over-year drop to $6 million in income.

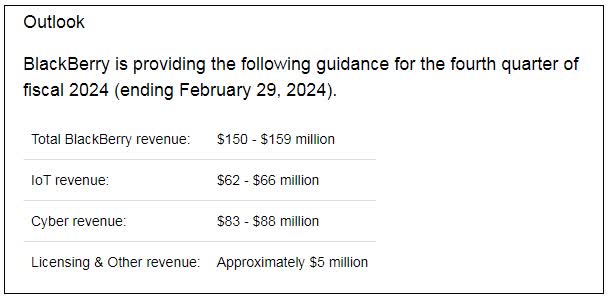

Within the press launch, BlackBerry administration talked concerning the Cybersecurity division securing massive strategic offers with main authorities businesses. Nevertheless, the corporate additionally reported that the annual recurring income (“ARR”) determine of this section dipped by one other $6 million sequentially to $273 million. The entire ARR right here is down $61 million up to now 18 months, and but once more administration is saying it ought to backside quickly, with progress not too far-off. The dollar-based internet retention charge right here at 82% stays effectively under what’s wanted for sustainable progress. Worse but was the corporate’s income steerage for the present interval, its fiscal This fall, which concludes on the finish of February 2024. Analysts have been on the lookout for almost $190 million, which might have been a pleasant sequential bounce to complete out the fiscal yr, however BlackBerry is now calling for a big sequential decline:

This fall Steerage (BlackBerry Q3 Earnings Launch)

On the margin aspect, the great improve in each Cybersecurity and IoT revenues helped gross margin {dollars} rise to their highest level in a few years (excluding the patent sale quarter). Nevertheless, it isn’t but sufficient to cowl the entire firm’s main working bills, so there are nonetheless GAAP losses being reported right here. The corporate’s adjusted revenue of a penny beat the road by 3 cents. Nevertheless, BlackBerry mainly by no means misses right here, because it all the time stories a lot of changes to make the underside line look significantly better – on this quarter these alterations have been a few nickel per share in whole.

A serious fear of traders is that the corporate does not have the monetary flexibility to execute a real turnaround plan. Complete money and investments have been $271 million on the finish of Q3, down from $519 million on the finish of Q2. Through the interval, the corporate’s convertible debentures hit their maturity date, however the inventory’s low value meant they could not be swapped for fairness. Administration ended up paying the $365 million again, however on the identical time issued new extension debentures within the quantity of $150 million. These will mature in February 2024, however could possibly be prolonged for a further three months. BlackBerry must get its money burn down, which in Q3 was considerably hampered by a surge in accounts receivable that put that stability sheet class determine at a price increased than the quarter’s income whole.

Since I final reported on the corporate in October, there have been two different main developments. First, John Chen retired from his CEO place after a really turbulent decade on the helm. Whereas Chen was employed to assist BlackBerry keep away from chapter, he did not get the long run income image again on observe. So whereas markets have soared to new all-time highs up to now ten years, BlackBerry shares misplaced a great chunk of their worth. Satirically, John Giamatteo, President of BlackBerry’s Cybersecurity division, was appointed as the brand new CEO, regardless of that section being the corporate’s worst income performer lately.

The second main information merchandise is that the plan to IPO the IoT section has been scrapped. On the convention name, administration defined its new plans, whereas it’s going to have two separate enterprise segments mainly below a holding firm. There might be some extra restructurings over the following calendar yr, which can minimize the working expense base down a bit. This could possibly be an honest catalyst if the corporate can get to GAAP profitability and constructive free money move, however everyone knows that BlackBerry has had loads of hassle assembly its objectives over the previous decade.

As of Wednesday’s shut, shares have been buying and selling at about 3.25 instances their anticipated income for the February 2025 fiscal yr. That is considerably under most comparable software program firms that go for top single digit or low double digits on a value to gross sales foundation. Nevertheless, a lot of these names have very sturdy income progress profiles, and a few even have sizable GAAP income and or important free money move technology. Whereas I am not thrilled about BlackBerry’s income state of affairs at present, that negativity is offset by the potential for profitability enchancment coming within the subsequent yr together with the depressed valuation. For that purpose, I am conserving a maintain ranking on the inventory, however I’ll study that extra in about three months as administration has mentioned to attend till the following earnings name for extra concrete numbers and plans for the separation and restructuring efforts.

Ultimately, it was one other disappointing quarterly report from BlackBerry. Whereas the corporate introduced its ordinary backside line beat for adjusted Q3 earnings, revenues once more missed estimates by an honest margin and This fall income steerage was effectively under avenue expectations. The corporate nonetheless has a gross sales downside, however a brand new CEO is in place so I will give him a while to get his close to time period plans finalized earlier than I can decide if this inventory ought to get a purchase or promote suggestion once more. One factor is for certain, and that’s that BlackBerry has been probably the most disappointing names lately, with shares very near multi-year lows at a time when the general market has been racing to new highs.

:max_bytes(150000):strip_icc()/GettyImages-1472083948-775e9fc6b6234908b7263070412a55ee.jpg)

{kind=link}