Pekic

Funding Thesis

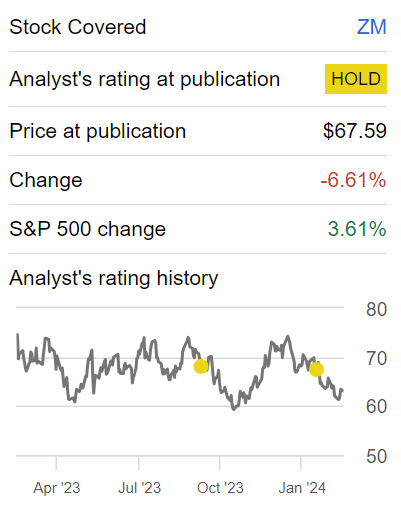

Zoom Video Communications, Inc. (NASDAQ:ZM) delivered fiscal This autumn 2024 outcomes and financial 2025 steerage that noticed its shares sizzle increased by greater than 10% premarket. Nevertheless, I declare that this rally is little greater than a reduction rally that Zoom’s outlook shouldn’t be worse.

Although the enterprise continues to ship very sturdy free money flows, whereas carrying a large amount of money on its steadiness sheet, I declare that its inventory is not worthwhile chasing, whilst there are just a few alluring nuggets to attract traders to this identify.

Fast Recap

Final month, I mentioned in a impartial evaluation, I mentioned:

[…] For traders, what actually issues is whether or not the inventory affords traders a compelling risk-reward. No investor will get all inventory picks proper. However our job is to deploy capital, and to take action selectively, solely once we imagine that the inventory affords traders a really compelling risk-reward.

Given Zoom’s present prospects, I don’t imagine this inventory affords traders a compelling risk-reward. Subsequently, I stay impartial on this identify, as I have been for some time.

Writer’s work on ZM

Zoom had been sliding because it headed into this earnings report with the inventory underperforming the S&P 500 (SP500) in a really sturdy market atmosphere. Nevertheless, whilst I’m able to comment on some optimistic parts on this report, there’s not sufficient right here to get me to claim a bullish ranking on this identify.

Why Zoom? Why Now?

Within the close to time period, Zoom stays centered on the enlargement of product choices. The introduction of the Zoom AI Companion has not solely demonstrated the corporate’s dedication to innovation however has additionally supplied clients with a instrument to boost their productiveness.

Notably, Zoom Crew Chat has skilled a outstanding 130% progress in utilization throughout paid accounts over the previous yr, showcasing its widespread adoption. As clients migrate from different chat platforms to Zoom, the corporate is positioned as a complete office resolution, driving buyer loyalty.

Regardless of the difficult macroeconomic backdrop, Zoom has demonstrated monetary resilience in fiscal 2024, with a 24% y/y improve in free money circulate (extra on Zoom’s free money circulate under).

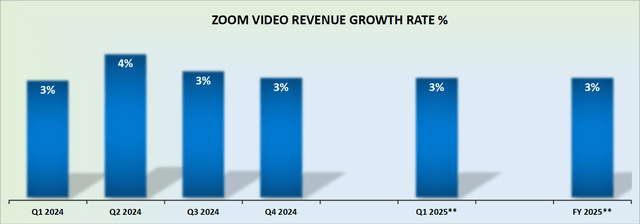

Nevertheless, Zoom additionally faces challenges associated to its progress charges. Zoom’s fiscal This autumn 2024 whole income progress of threepercenty/y signifies an absence of reacceleration is on the playing cards for fiscal 2025.

Furthermore, the corporate’s acknowledgment of a trough in year-over-year progress in fiscal Q2 2025 suggests a necessity for methods to reinvigorate its trajectory. The challenges are additional underscored by the comparatively flat efficiency within the EMEA area and a decline in APAC, indicating potential saturation in these markets.

Given this background, let’s now talk about its outlook for fiscal 2025.

Income Progress Charges Anticipated to Attain 3% to five% CAGR

ZOOM income progress charges

Zoom’s outlook for fiscal 2025 factors to roughly 3% to five% top-line progress. To substantiate this rivalry, take note the next desk.

SA Premium

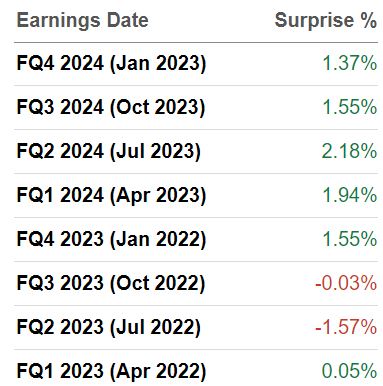

Zoom, for essentially the most half, beats income estimates by roughly 1% to 2%. The times when Zoom might be counted on to massively beat income estimates at the moment are a distant reminiscence.

Regardless of evaluating with a decrease income progress price hurdle with the prior yr, Zoom is not a quickly rising tech enterprise. Subsequently, its seemingly shareholder base is extra seemingly than not going to return from the worth camp.

Consequently, for Zoom to draw worth traders to its identify, it would convincingly display that it has what it takes to develop its underlying free money flows, past simply one-off cost-cutting measures. Given this context, we’ll now flip to debate its valuation.

ZM Inventory Valuation — 12x Ahead Free Money Flows

On the one hand, there’s so much to love about Zoom. In spite of everything, Zoom has no debt on its steadiness sheet and a whopping amount of money. Extra particularly, together with the premarket soar, 35% of Zoom’s market cap is made up of money and equivalents.

For sure that it is a great amount of money for a enterprise that’s clearly extremely free money circulate generative. Nevertheless, the issue right here I assert has to do with tackling these two issues:

What Zoom plans to do with this extra money? How lengthy will it take for this money to return to shareholders?

Even when Zoom mindlessly repurchases its shares, the time it takes for traders to pay money for these repurchases issues to traders’ return.

In spite of everything, Zoom’s share buyback presently stands at $1.5 billion, which is a paltry determine in contrast with $7 billion of money on its steadiness sheet. And on prime of that, the share repurchase program is open-ended, with no due date.

After which, additional confounding issues, the outlook for fiscal 2025 factors to roughly $1.5 billion of free money circulate, which is virtually equivalent to fiscal 2024. Consequently, it reveals traders that many of the cost-cutting that was potential to happen has already taken place in fiscal 2024 (the yr simply reported).

The Backside Line

In abstract, Zoom Video’s fiscal This autumn 2024 outcomes led to a premarket surge, but this appears extra like a reduction rally than a robust endorsement.

Regardless of strong free money flows and a major money reserve, the inventory lacks an attractive proposition for traders.

The forecast for fiscal 2025 signifies modest income progress charges of three% to five%, pointing to a extra mature progress stage. Valuation-wise, Zoom’s inventory trades at roughly 12 occasions ahead free money flows, however questions come up in regards to the firm’s plans for extra money utilization and the timeline for returning it to shareholders.

Total, I stay impartial on Zoom Video Communications, Inc. inventory.

:max_bytes(150000):strip_icc()/GettyImages-1472083948-775e9fc6b6234908b7263070412a55ee.jpg)

{kind=link}