PM Photographs

Absurdities of Market Construction

“We dwell in an upside-down age the place making a revenue distribution to firm homeowners is seen, extremely, as a failing by many S& P 500 Index firms and nothing lower than heresy by the overwhelming majority of latest economic system firms.” -Daniel Peris

We dwell in attention-grabbing instances. Nowhere is that extra evident than within the construction of the fairness markets. Earlier market environments noticed firms pay their traders a portion of their income, often called a dividend. This dividend tradition was a standard a part of investing in fairness markets. Company boards and administration noticed dividends as an integral a part of the capital return insurance policies they pursued and pushed dividends as much as entice traders to develop into homeowners of their inventory. This can be a factor of the previous, because the variety of shares that pay dividends has dwindled, and the general yield on the S&P 500 has fallen to a mere 1.58%.

Think about that dividends made up 75% of the full return for the S&P 500 index from 1871-1989. However from 1990-2023, dividends made up solely 30% of the full return. What explains this transformation?

One can clearly level to the 1982 laws that made inventory buybacks acceptable, even most popular by administration. It is very important observe that previous to 1982, buybacks had been unusual and seen as a type of market manipulation, how the instances have modified. One may additionally look to the daybreak of the expertise sector, and its interval of dominance over the market capitalization in the course of the 1990-present interval. However the true wrongdoer is the adoption by company boards and administration of ideas of theoretical finance that made the case that dividends didn’t matter. That it was merely a capital construction determination and dividend coverage was lower than meaningless, it was irrelevant.

This sentiment is reiterated at the moment by issue traders and people who imagine the arguments of theoretical finance made within the latter half of the twentieth century with out questioning these clearly doubtful theories. The 2008 monetary disaster definitely ought to have made us query these theories and their applicability to trendy markets, as almost each danger mannequin based mostly on these tutorial theories was confirmed nugatory.

The 20 yr underneath efficiency of worth to progress ought to have additionally made traders query the findings of lecturers who declare that traders ought to pay further charges to chase a tutorial definition of worth on a complete return foundation with out consideration of dividends. It ought to be famous that the unique Fama & French issue mannequin analysis executed the worth issue via an extended/brief technique, not by merely proudly owning worth shares lengthy solely. This simply proves that many of the practitioners on this space fail to even learn the analysis, and even fewer perceive its implications. A incontrovertible fact that turns into evident whenever you interact with issue traders who imagine within the components with spiritual like zeal.

As a substitute let me contend and show on this piece that traders have to take a distinct method to investing. I need to evaluation the literature that received us to this place the place market members truly imagine within the dividend irrelevance principle and show why that is misguided at greatest and dangerous at worst. I’ll additional make the case for renewing an outdated concept, of viewing investments in fairness securities as items of actual companies, companies that ought to be paying their homeowners a bit of the income earned. Primarily based on the proof one may even make the argument that dividends are the ONLY motive to spend money on shares.

Think about the return within the inventory market from 1871-2023. Shares returned 7.01% actual return together with dividends. This quantity drops to a mere 2.5% actual return when dividends are taken out. It’s dividends which have pushed the returns in fairness securities for this 152-year time interval. When seen throughout the span of market historical past, we see simply how anomalous the present low dividend atmosphere is.

Difficult Educational Finance

The elemental parameters of educational finance have formed the world we dwell in at the moment. They act as a kind of ordering system to carry order to chaos and make the world of finance make sense. However there may be another view to the concepts put forth by monetary principle. Daniel Peris, famous historian, and Portfolio Supervisor at Federated-Hermes, posits a few of these critiques in his earlier guide, “Getting Again to Enterprise”, an intensive refutation of recent portfolio principle. He furthers his evaluation to wanting on the tutorial literature round dividends in his new guide, The Possession Dividend.

In it he challenges the assumptions made by Markowitz in his landmark paper by making the purpose that there’s a huge quantity of subjectivity within the creation of those fashions. This makes them much less dependable, and unrealistic for software to the actual world.

We additionally see this within the space of diversification. The educational definition of diversification would require an investor to carry 1000’s of firms within the often-cited whole inventory market index. This, they argue, ensures you get the most effective returns by proudly owning the entire market. This argument comes immediately from tutorial finance, and a great deal of traders have piled on the prepare, bringing their self-fulfilling prophecy to fruition.

The index revolution might have began in 1976 with Jack Bogle and the creation of the primary index fund, however the theoretical underpinnings for the full market index fund began nicely earlier than that. In recent times we now have actually seen an acceleration within the adoption of index merchandise. That is very true in these looking for to retire early, the so-called “FIRE” communities. Buyers in these communities are piling into whole market index funds, with many utilizing it for ALL of their cash on the recommendation of a number of gurus within the motion. However what do these traders actually personal? In the event you ask them, they’ll say they personal the whole market. In the event you requested them additional in the event that they had been nicely diversified, they’d say “in fact! I personal over 3,000 firms!”

In actuality nonetheless, they’d be mistaken. The overall market index might actually have 3,000 firms in it, however it’s far much less diversified than most of its holders notice.

Greater than 1 / 4 of the fund’s belongings are present in its high 10 holdings. 50% of the portfolio’s belongings are in its high 50 holdings, representing a mere 1.6% of portfolio positions. The opposite 50% is scattered amongst 1000’s of firms having little if any impact on the general efficiency of the fund, it’s diversification for variations sake, or what Charlie Munger referred to as “diworsification.”

So, in actuality, the full inventory index is a momentum pushed, extremely concentrated portfolio representing a market recognition contest, and leaving those that put their hard-earned cash into it uncovered to essentially the most danger, on the highest costs, for the most well-liked shares that climb to its high 10. That is most danger for BELOW common return after charges and bills. This isn’t investing, so let’s name it what it’s, that is speculating.

“There’s just one clever type of investing: determining what one thing is value and seeing if you should buy it under that worth. It is all about worth. -Howard Marks

Each investor ought to learn the 2017 piece, “The Energetic Fairness Renaissance: The Rise and Fall of MPT” by C. Thomas Howard, on the CFA institute weblog, it offers a terrific abstract of the rise and fall of accepted dogma inside the monetary group and makes a name for proof and rationality in a world of emotional determination making. In my favourite part from the piece, the writer states:

A lot of finance pushes apart the mounting opposite proof and troopers on underneath the yoke of the MPT paradigm. This might sound stunning: Is not finance a self-discipline based mostly on empiricism, one which solely accepts ideas supported by proof? Sadly, as Thomas Kuhn argued years in the past in his traditional work, The Construction of Scientific Revolutions, scientific {and professional} organizations are human and are inclined to the identical cognitive errors that afflict particular person determination making.

This critique of educational finance naturally flows to the dividend puzzle and the notion that dividends are irrelevant. With the intention to dissect this viewpoint we should start with Markowitz and his foundational concept of recent portfolio principle and the notion of diversification.

As Daniel Peris states:

“Markowitz follows with one other assertion in 1952 that “diversification is each noticed and smart; a rule of habits which doesn’t suggest the prevalence of diversification should be rejected each as a speculation and as a maxim.” I don’t dispute this assertion, however I do need to observe that it’s no much less a subjective alternative than his different first ideas. And I might repeat my earlier remark that in follow, having 30-40 shares verses 3 or 4, as was frequent then, is certainly risk-reducing diversification, however that having many a whole bunch and even 1000’s of holdings in a single’s portfolio, as is frequent at the moment via index funds and ETF’s, is just not.

He continues:

Markowitz may by no means have imagined, nor may he have supposed such an absurd state of affairs. Worse, the intense diversification so common at present is a type of self-deception in that the overdiversified traders are actually selecting not to decide on, whereas on a regular basis pondering they’ve made very accountable choices.

Within the Dividend Puzzle, Black states the next:

“The selection between a standard inventory that pays a dividend and a inventory that pays no dividend is analogous, no less than if we ignore things like transaction prices and taxes. The worth of the dividend-paying inventory drops on the ex-dividend date by in regards to the quantity of the dividend. The dividend simply drops the entire vary of doable inventory costs by that quantity. The investor who will get a $2 dividend finds himself with shares value about $2 lower than they’d have been value if the dividend hadn’t been paid, in all doable circumstances.”

On this evaluation Black ignores two basic ideas.

1. The investor who will get the $2 dividend and reinvests it now owns extra shares than they did earlier than the corporate paid the dividend. Whereas their whole steadiness doesn’t change as Black accurately states, the worth of the inventory drops to mirror the fee of dividends, it’s accretive to the long-term investor who acts like an proprietor. It steadily will increase their shares over time offering them with a bigger and bigger declare on the corporate’s earnings.

2. The revenue investor doesn’t must deplete their possession stake to obtain revenue from the funding within the shares in the event that they obtain a dividend. Within the case of the revenue investor, the worth of the inventory drops by $2, and the investor will get $2 in dividend revenue. The investor who invests in non-dividend paying shares as a result of they imagine dividends don’t matter, must promote their shares to create an equal quantity of “revenue” by realizing capital good points.

That is yet one more instance of how tutorial finance fails to account for the real-world software of those theories. Dividends are most definitely not irrelevant for long run traders who search to compound their wealth over a long time. Think about that in Modigliani and Millers 1961 exposition of the dividend irrelevance principle they made a lot of assumptions corresponding to taxes don’t exist, there aren’t any flotation prices or transaction prices for issuing inventory, dividend coverage has no affect on capital budgeting choices, leverage has zero affect on the price of capital, and at last essentially the most absurd of all assumptions and the important perception of constructing the speculation work, corporations pay out 100% of Free Money Move (FCF).

In actuality none of those assumptions maintain true.

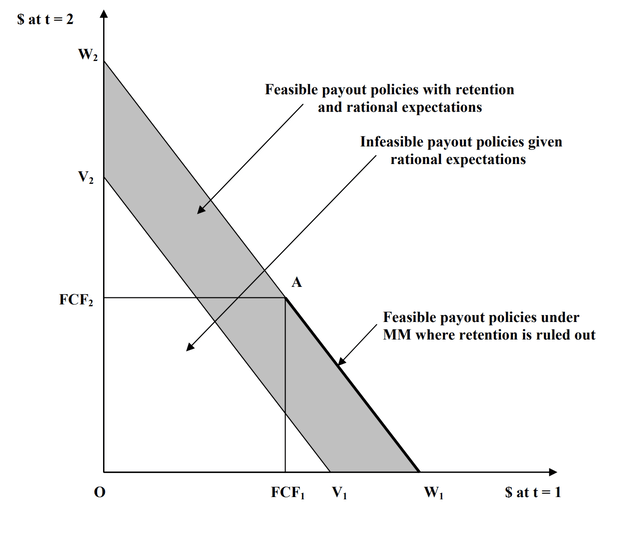

The perfect critique I’ve discovered of the dividend irrelevance principle, and the Dividend Puzzle of Fischer Black who depends on Modigliani and Miller’s dividend irrelevance, comes from Harry and Linda DeAngelo of the Marshall College of Enterprise at USC. Of their paper “The Irrelevance of the MM Dividend Irrelevance Theorem”, they critique Miller and Modigliani’s assumption of 100% FCF payout, an assumption that after we enable for retention of free money, fails.

The Irrelevance of the MM Dividend Irrelevance Theorem, Determine 2 (DeAngelo)

“As a result of their assumptions guarantee payout coverage optimality by forcing 100% FCF distribution to be an automated by-product of the funding alternative, MM (1961) confound funding and payout coverage and mistakenly attribute the worth affect of payout coverage optimization to funding coverage. Payout coverage issues when MM’s assumptions are relaxed to permit retention of FCF as a result of there isn’t a longer a one-to-one correspondence between possible and optimum insurance policies.”

One problem up to now is the concept even with retention allowed, the dividend irrelevance principle holds so long as the web current worth (NPV) of funding coverage is mounted. On this problem lies the very proof wanted to disprove dividend irrelevance. As a result of whenever you enable for retention, you give managers the power to make choices on payout coverage, simply as they’ve in the actual world. Subsequently, Miller and Modigliani’s principle of dividend irrelevance is making assumptions that don’t carry over to sensible software. Payout coverage could be very related to managers, and stockholders.

A closing critique of Fischer Black’s dividend puzzle, which depends on dividend irrelevance, demonstrates how the logic of the whole principle fails when utilized to actual world determination making by firms:

“Black argues that when taxes are added to the MM framework, corporations ought to largely get rid of payouts to stockholders,1 which they clearly don’t. However the logic Black makes use of to generate this prediction is flawed. In all instances, together with these through which payouts are taxed, optimum payout coverage requires distributions which might be giant in current worth phrases; if managers truly applied Black’s suggestion to get rid of nearly all payouts, they’d destroy untold quantities of stockholder wealth. (emphasis mine)

Conclusion

Citing the subject of dividends should not be controversial, however in private finance circles, this can be a slightly controversial subject. Some argue that dividend traders are “unsophisticated” and as a substitute traders ought to be centered on whole return. They cite the analysis of Fischer Black in his seminal work “The Dividend Puzzle,” as proof for his or her superiority. However within the course of, they ignore a plethora of proof on returns that categorically denies their view. The fact is that dividends make up almost the entire return that traders obtain from fairness securities. Investing in non-dividend paying shares proved to provide the bottom returns as I confirmed right here.

In conclusion, dividends stay an vital a part of funding within the capital markets as famous portfolio supervisor David Bahnsen lays out on this clip from his Dividend Cafe podcast through which he discusses the logic of dividends vs. speculative insanity.

I hope Daniel Peris is right, and we’re coming into a brand new paradigm shift, away from share buybacks and again in the direction of the resumption of dividend funds as the popular capital return coverage. I finish with a quote from The Possession Dividend discussing the significance of dividends and the non-equivalence of dividends and buybacks:

Whether or not in principle or in follow, these two actions—on one hand, clipping your coupons; alternatively, going out and promoting securities—are most definitely not the identical. Having capital good points depends upon market sentiment, on the views of individuals typically far faraway from the actions of an organization. In distinction dividends are a perform of an organization’s operations. A greenback could also be fungible; how it’s generated is just not. Drawing this distinction—between a capital markets exercise and a enterprise final result—could also be a very powerful assertion on this guide. The remainder of the argument follows naturally from it. -Daniel Peris, The Possession Dividend

:max_bytes(150000):strip_icc()/GettyImages-1472083948-775e9fc6b6234908b7263070412a55ee.jpg)

{kind=link}